Assessing GE Vernova (GEV) Valuation After Strong Earnings And AI Data Center Demand Surge

GE Vernova Inc. GEV | 0.00 |

GE Vernova (GEV) is back in focus after reporting quarterly results that beat expectations, highlighting strong demand for its gas turbines from AI data centers and new reservation deals that are filling its gas power backlog.

The strong quarterly update and a run of new turbine and grid agreements, from Maxim Power to Xcel Energy, have coincided with sharp momentum. The 30 day share price return is 28.74% and the 1 year total shareholder return is 123.35% from a latest share price of $823.67, suggesting investors are reassessing both growth potential and risk around GE Vernova’s role in supplying power for AI heavy data centers.

If this surge in interest around energy and AI infrastructure has you looking wider, it could be a good time to check out 34 AI infrastructure stocks as another way to spot power related data center plays.

With the stock up sharply and trading only about 1% below the average analyst target, the key question now is simple: Is GE Vernova still mispriced, or are markets already baking in years of future growth?

Most Popular Narrative: 10% Undervalued

GE Vernova’s last close of $823.67 sits just above a widely followed fair value narrative of $714.58. This frames the debate around how much growth is already priced in.

Revenue Growth: GE Vernova is expected to grow its revenue by 13%, contributing to a total revenue of US$77 billion.

Earnings Forecast: Estimated earnings for 2030 are US$4.2 billion, translating into a market capitalization of US$270.06 billion, based on a 64.68x price-to-earnings ratio.

Read the complete narrative. Read the complete narrative.

According to lexdrew1, this fair value hinges on a step change in revenue scale, fatter margins, and a premium earnings multiple that would usually sit with pure tech names. If you are curious which assumptions connect today’s share price to that kind of 2030 profile, and how sensitive the valuation is to even small changes in those inputs, the full narrative lays out the entire roadmap behind that $714.58 figure.

Result: Fair Value of $714.58 (ABOUT RIGHT)

However, that story could unravel quickly if AI driven data center demand softens, or if execution slips across its Power, Wind, or Electrification segments.

Another View: Our DCF Model Flags Downside

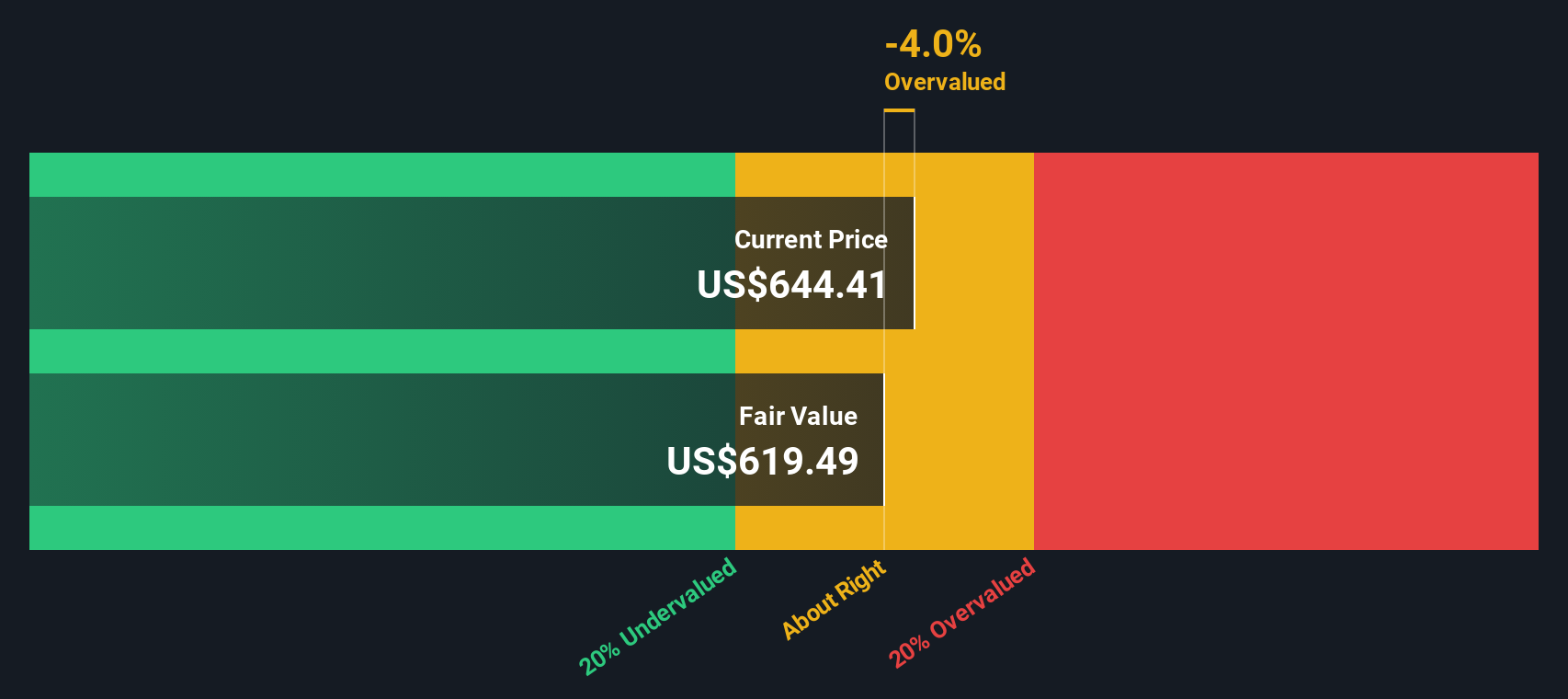

That 10% undervalued narrative sits awkwardly next to our DCF model, which points to a fair value of $653.48 per share. With GEV at $823.67, the stock screens as overvalued on future cash flows. This raises a simple question: which story are you more comfortable relying on?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out GE Vernova for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own GE Vernova Narrative

If you see the numbers differently, or prefer to weigh the assumptions yourself, you can build a complete view in just a few minutes: Do it your way

A great starting point for your GE Vernova research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If GE Vernova has sharpened your focus on quality, do not stop here. Use the screener to surface a fresh batch of ideas that fit your style.

- Target quality at a sensible entry point by scanning our list of 51 high quality undervalued stocks that pair stronger fundamentals with more modest pricing.

- Prioritise resilience and sleep easier at night by checking companies in the 85 resilient stocks with low risk scores that score well across our risk checks.

- Spot lesser known names before the crowd by reviewing the screener containing 24 high quality undiscovered gems that still fly under most investors' radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.