Assessing Genesis Energy (GEL) Valuation After Soda Ash Exit And Pipeline Spending Completion

Genesis Energy, L.P. GEL | 17.60 | +0.57% |

What Is Driving Fresh Attention on Genesis Energy?

Genesis Energy (GEL) is back on investors’ radar after selling its soda ash business, wrapping up a heavy pipeline spending cycle, and drawing renewed support from analysts covering the midstream space.

After a sharp reset over recent years, Genesis Energy’s recent 7 day share price return of 4.88% and 30 day gain of 8.11% sit alongside a 1 year total shareholder return of 64.27%. This hints that momentum has been building as investors react to the soda ash sale, pipeline spend winding down, and fresh optimism around its core midstream operations.

If this renewed interest in midstream infrastructure has caught your eye, it could be a good moment to broaden your search with our 24 power grid technology and infrastructure stocks for more grid focused opportunities.

With the soda ash sale complete, heavy pipeline spending behind it, a unit price of US$17.19, and what appears to be a wide gap to certain valuation estimates, the question is simple: is Genesis Energy still mispriced, or is the market already factoring in future growth?

Preferred Multiple of 0.7x P/S: Is It Justified?

On simple sales based metrics, Genesis Energy’s current unit price of $17.19 lines up with a P/S of 0.7x that screens as cheap against several benchmarks.

P/S compares the company’s market value to its revenue and is often used for businesses that are not yet profitable. For Genesis Energy, a 0.7x P/S is flagged as good value relative to both the US Oil and Gas industry average of 1.6x and a peer average of 2.4x. This suggests the market is assigning a lower value to each dollar of current revenue than it does to many comparable companies.

However, the SWS fair ratio work points in a different direction. Against an estimated fair P/S of 0.3x, Genesis Energy’s 0.7x is described as expensive. This implies a level that the market could move closer to if that fair multiple proves to be a better guide over time. Taken together, investors are weighing a discount to sector and peer averages against a premium to this fair ratio marker.

Result: Price-to-Sales of 0.7x (ABOUT RIGHT)

However, you also need to factor in the annual revenue contraction of 37.65% and the recent net loss of US$160.474m as potential pressure points on the story.

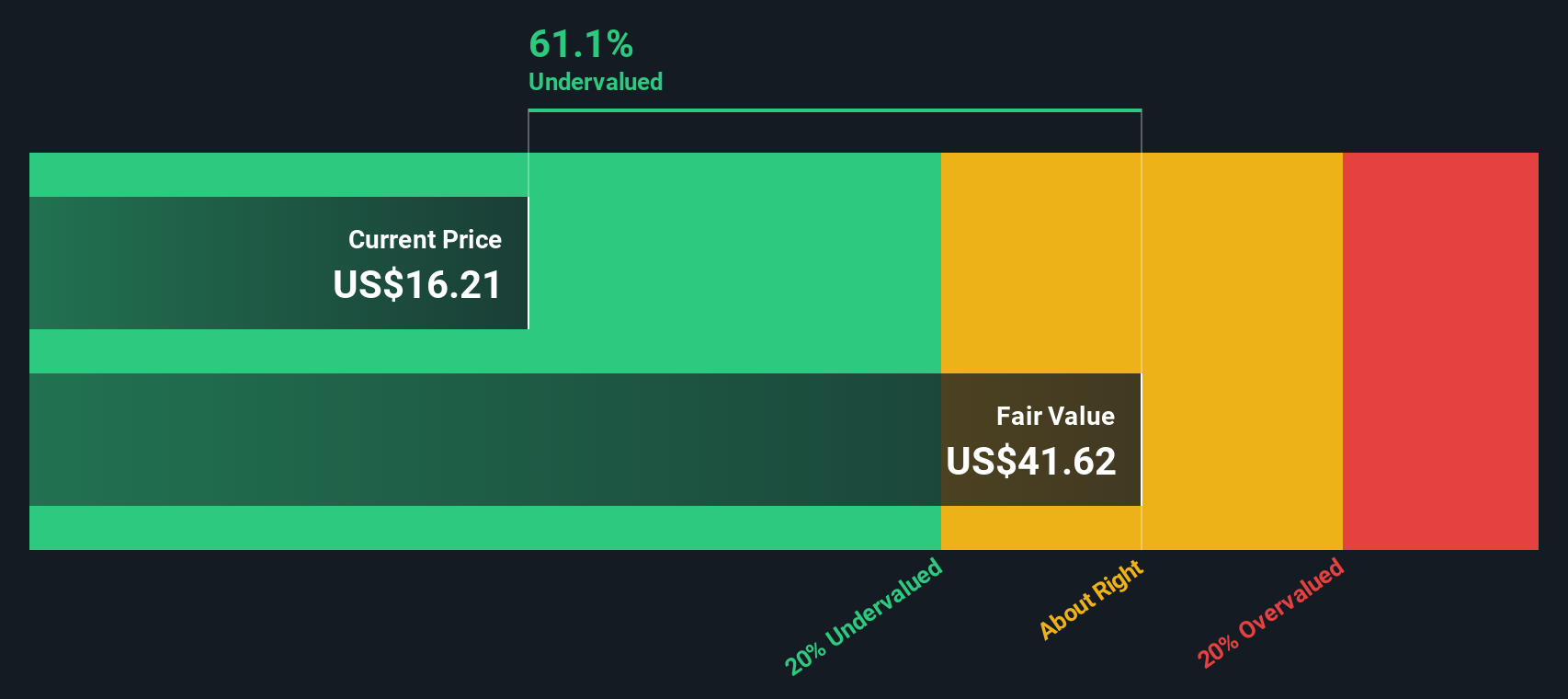

Another View: DCF Paints a Very Different Picture

If you put the P/S ratio to one side and look at our DCF model, the story flips. At $17.19, Genesis Energy is assessed as trading 66.6% below an estimated future cash flow value of $51.40, which points to a very different sense of what the units might be worth.

This gap between a low P/S and a large DCF discount leaves you with a puzzle to solve: is the market rightly cautious about revenue contraction and ongoing losses, or is the cash flow outlook being priced too harshly?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Genesis Energy Narrative

If this framework does not quite line up with your view, or you would rather test your own assumptions against the numbers, you can build a personalised Genesis Energy narrative in just a few minutes, starting with Do it your way.

A great starting point for your Genesis Energy research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If you are serious about building a stronger portfolio, do not stop with just one stock. Use these focused idea lists to widen your opportunity set.

- Target potential value candidates by reviewing our 52 high quality undervalued stocks, built to surface companies that may be trading at attractive prices relative to their fundamentals.

- Prioritise resilience with the 84 resilient stocks with low risk scores, which highlights businesses carrying lower risk scores so you can concentrate on steadier profiles.

- Spot earlier stage opportunities through the 24 elite penny stocks with strong financials, a curated list that can help you find smaller names with stronger financial underpinnings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.