Assessing Global Partners (GLP) Valuation After Recent Unit Price Strength And Conflicting Fair Value Signals

Global Partners LP GLP | 0.00 |

Global Partners (GLP) is back on investors’ radar after recent trading, with the units last closing at $47.23. The move comes alongside a one-month return of 6.4% and a year-to-date gain of 11.8%.

The recent 2.4% 1 day share price return and 6.5% 30 day share price return suggest improving momentum in the short term, even though the 1 year total shareholder return is slightly negative and the 5 year total shareholder return is much stronger.

If this move in Global Partners has you thinking about where else to put fresh capital to work, it could be worth scanning 33 power grid technology and infrastructure stocks

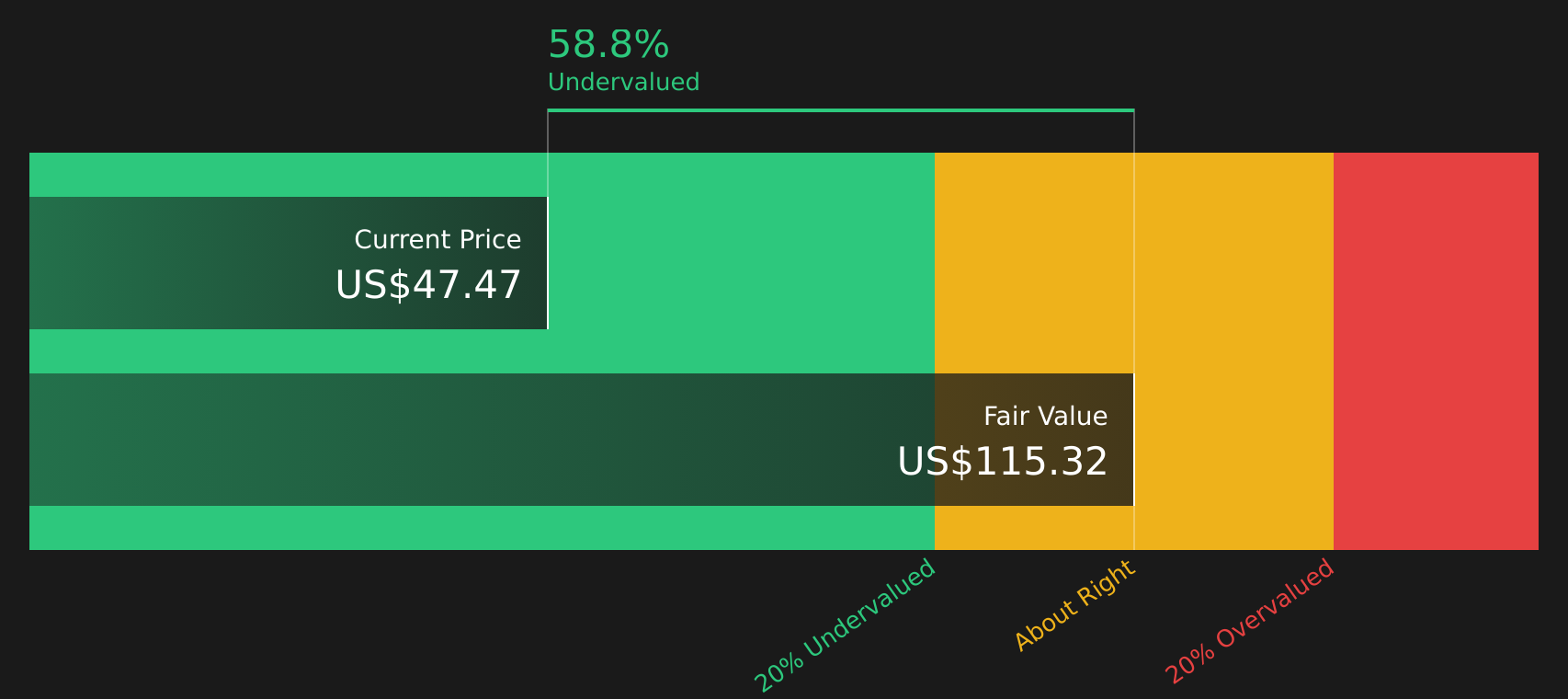

With Global Partners trading at $47.23, slightly above a US$45.50 analyst target but with an estimated 35% intrinsic discount and mixed recent returns, is the market offering a mispriced entry, or already pricing in future growth?

Most Popular Narrative: 4% Overvalued

At $47.23, Global Partners sits slightly above the most followed fair value estimate of $45.50 per unit, which is built on detailed long term growth and margin assumptions.

Acquisitions, divestments, and demographic trends are expected to support revenue stability, margin improvement, and stronger market positioning across core segments.

Refinancing efforts enhance financial flexibility, allowing for continued investment, expansion, and resilience amid changing energy and retail landscapes.

Want to see what keeps that fair value anchored near today’s price? The key ingredients are aggressive top line growth, steady margins, and a lower future earnings multiple. Curious which assumptions really move the needle in this narrative?

Result: Fair Value of $45.50 (OVERVALUED)

However, this story can change quickly if fuel volumes weaken or tighter carbon regulations lift costs, putting pressure on margins and long term returns on assets.

Another View: Cash Flows Tell a Different Story

Analysts see Global Partners as slightly overvalued at $47.23 versus a $45.50 fair value, but the SWS DCF model points the other way, with an estimated future cash flow value of $73.15. One framework leans cautious; the other suggests a wide upside gap. Which one do you trust more right now?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Global Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment, the key question is how it all lines up for you and your risk appetite. Move quickly, test the assumptions, and weigh both sides using the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Global Partners caught your attention, do not stop here; broaden your watchlist now so you are not late to the next opportunity.

- Spot potential bargains early by scanning 53 high quality undervalued stocks, which pairs solid fundamentals with prices that may not fully reflect their underlying strength.

- Strengthen your income stream by checking out 14 dividend fortresses, built around higher yielding companies that focus on consistent payouts.

- Prioritize resilience by reviewing 72 resilient stocks with low risk scores, where companies score well on financial stability and overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.