Assessing GlobalFoundries (GFS) Valuation After Buyback, Earnings Update And New 2026 Guidance

GlobalFoundries Inc. GFS | 48.31 | -0.21% |

Why GlobalFoundries stock is back in focus

GlobalFoundries (GFS) has jumped onto investors’ radar after announcing a US$500 million share repurchase program, together with fresh quarterly and full year 2025 results, new 2026 guidance, and leadership changes.

The latest earnings release, buyback announcement and leadership updates come after a strong run in the share price, with a 7 day share price return of 16.92% and a 90 day share price return of 48.73%. However, the 3 year total shareholder return of a 22.37% decline shows longer term holders have had a very different experience.

If this news has you looking across the semiconductor and chip ecosystem, it could be a useful time to scan 34 AI infrastructure stocks as another way to source ideas connected to next generation computing demand.

With GlobalFoundries posting US$885 million in net income for 2025, outlining fresh 2026 guidance, and authorizing a US$500 million buyback while trading near its analyst price target, is there still a potential entry point here, or is future growth already priced in?

Most Popular Narrative: 3.2% Undervalued

With GlobalFoundries last closing at $48.99 and the most followed narrative pointing to a fair value of $50.62, the gap is small but worth unpacking.

The company's focus on differentiated technologies (such as FD-SOI, RF, and power management platforms) and recent MIPS acquisition strengthens its value proposition in edge AI, automotive, and data center markets, deepening customer partnerships and enabling premium pricing, which is likely to drive sustained improvements in revenue visibility and margin stability.

Curious how that premium pricing and product mix translate into the $50.62 fair value? The narrative leans heavily on expectations for revenue growth, margin uplift and the earnings multiple that ties it all together.

Result: Fair Value of $50.62 (UNDERVALUED)

However, there are still clear pressure points, including pricing strain in smart mobile contracts and heavy capital spending needs that could challenge the margin and free cash flow story.

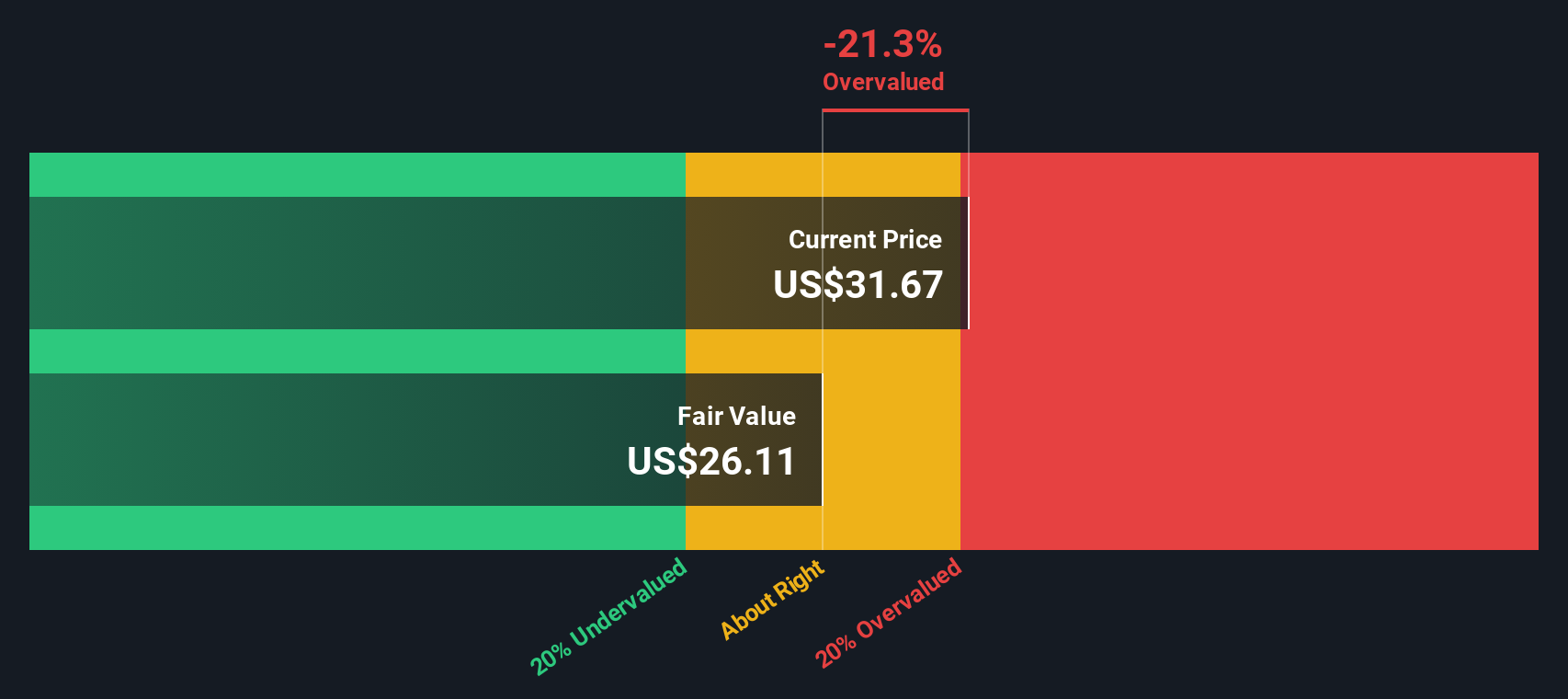

Another View: DCF Points to Overvaluation

While the most followed narrative suggests GlobalFoundries is about 3.2% undervalued at $48.99 versus a $50.62 fair value, the SWS DCF model comes to a very different conclusion. In that framework, the shares sit above an estimated future cash flow value of $37.05, so are framed as overvalued. Which story do you think fits the cash flow profile better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out GlobalFoundries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals here leave you split, that is the point. Use the data, move quickly, and weigh 3 key rewards alongside everything else.

Looking for more investment ideas?

If GlobalFoundries has you thinking about what else might be out there, do not stop at one ticker. Broaden your watchlist with targeted screens built around clear fundamentals.

- Spot potential mispricings by reviewing 55 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their underlying business strength.

- Prioritise resilience with 82 resilient stocks with low risk scores, focusing on companies that score well on stability to help you keep volatility in check.

- Hunt for tomorrow’s potential leaders using our screener containing 24 high quality undiscovered gems, where smaller names with strong metrics might not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.