Assessing Globus Medical (GMED) Valuation After Hammer Pattern Signal And Upgraded Earnings Outlook

Globus Medical Inc Class A GMED | 0.00 |

Technical signal and earnings expectations shift focus to Globus Medical

A recent hammer chart pattern in Globus Medical (GMED) has coincided with higher earnings estimates and a top Zacks Rank, prompting investors to reassess the spine and orthopedics specialist’s current share performance.

At a share price of US$87.17, Globus Medical has seen short term share price weakness with a 7 day return of 3.64% and a 90 day return of 1.92% decline, while its 1 year total shareholder return of 22.26% and 3 year total shareholder return of 66.01% point to momentum that has been building over a longer horizon.

If this technical shift has you looking beyond a single name, it could be a good moment to see what else is setting up on our screener of 34 healthcare AI stocks.

With shares at US$87.17, a value score of 4, and an intrinsic value estimate that is roughly 4% above the market price, is Globus Medical quietly offering upside, or is the market already pricing in its future growth?

Most Popular Narrative: 20.4% Undervalued

Globus Medical’s most followed narrative pegs fair value at about $109.54, well above the recent $87.17 close. This sets up a clear valuation gap for investors to assess.

Successful integration and synergy capture from the NuVasive and Nevro acquisitions are providing opportunities for increased cross-selling, cost efficiencies, and realization of deferred tax assets, which are expected to drive margin expansion, boost earnings, and enhance recurring cash flows in upcoming years.

Curious what earnings profile and margin path support that higher fair value, and how growth, profitability and the chosen discount rate all fit together? The full narrative lays out those assumptions in detail, including how future earnings power and valuation multiples are being framed against current performance.

Result: Fair Value of $109.54 (UNDERVALUED)

However, this depends on acquisitions such as NuVasive and Nevro meeting margin goals, as well as capital spending for robotics avoiding prolonged slow patches.

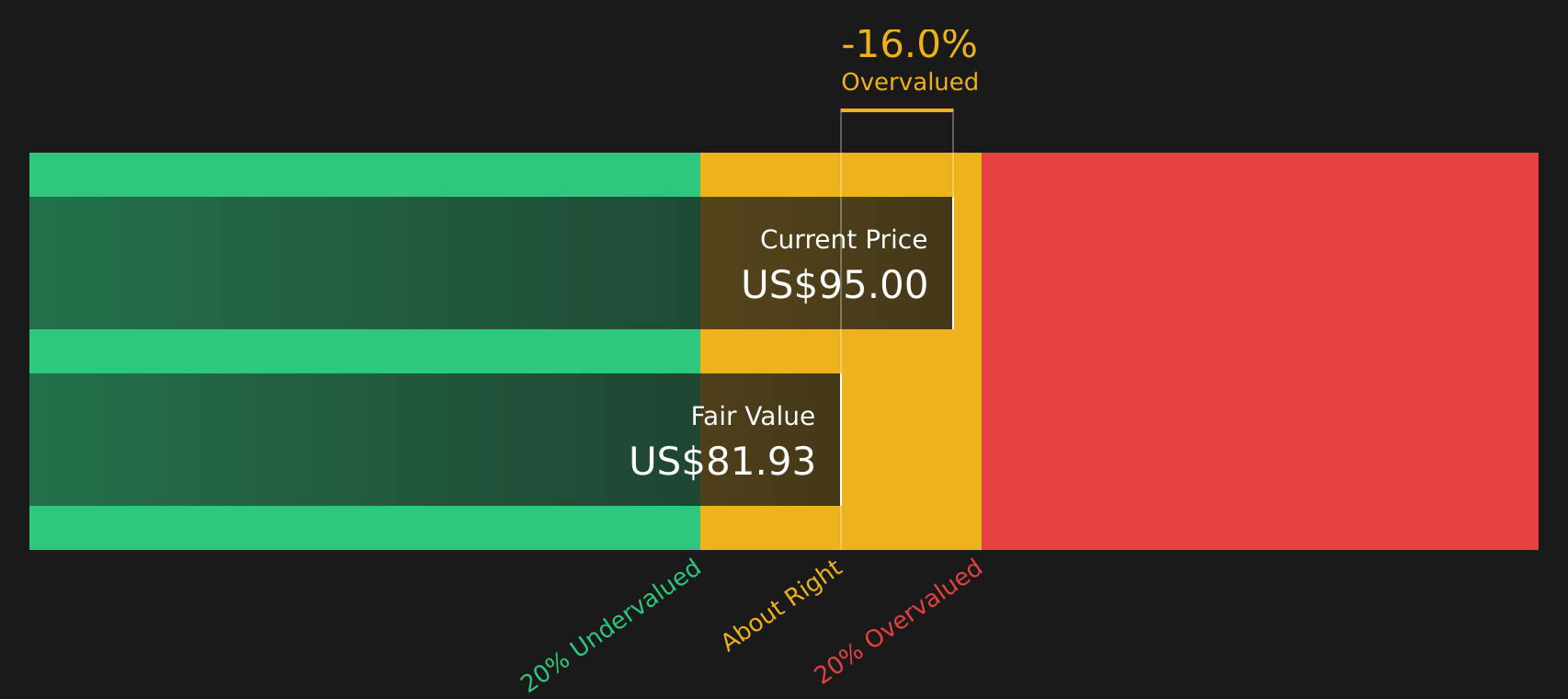

Another View: SWS DCF Points To A Tighter Margin Of Safety

While the narrative fair value sits at about $109.54, our DCF model comes out closer to $83.84, with the current $87.17 price sitting above that mark. In plain terms, that approach views Globus Medical as slightly overvalued right now. Which lens do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Globus Medical for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of signals leaves you undecided, it is a good time to look through the numbers yourself and move quickly to shape your own view. To understand what the market is currently optimistic about, take a closer look at 5 key rewards.

Looking for more investment ideas?

If Globus Medical has sharpened your focus, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Target potential value upside by scanning our list of 50 high quality undervalued stocks that combine price appeal with solid fundamentals.

- Strengthen your income stream by reviewing 14 dividend fortresses that offer higher yields with a focus on resilience.

- Protect your downside by checking out 67 resilient stocks with low risk scores that score well on financial stability and risk controls.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.