Assessing GRAIL (GRAL) Valuation After Analyst Upgrades And Strong Recent Shareholder Returns

Grail GRAL | 54.99 | +2.59% |

GRAIL (GRAL) is back on investors’ radar after several analysts recently raised their ratings, pointing to growing interest in the company’s multi cancer early detection platform and its long term potential.

The recent analyst upgrades come against a backdrop of sharp share price moves, with a 14.93% 1 month share price return and a 10.81% 3 month share price return. The 1 year total shareholder return of 278.77% suggests momentum has been strong despite short term swings.

If GRAIL’s story has caught your attention, this could be a useful moment to scan the wider healthcare space and see how other healthcare stocks compare on growth, risk, and price.

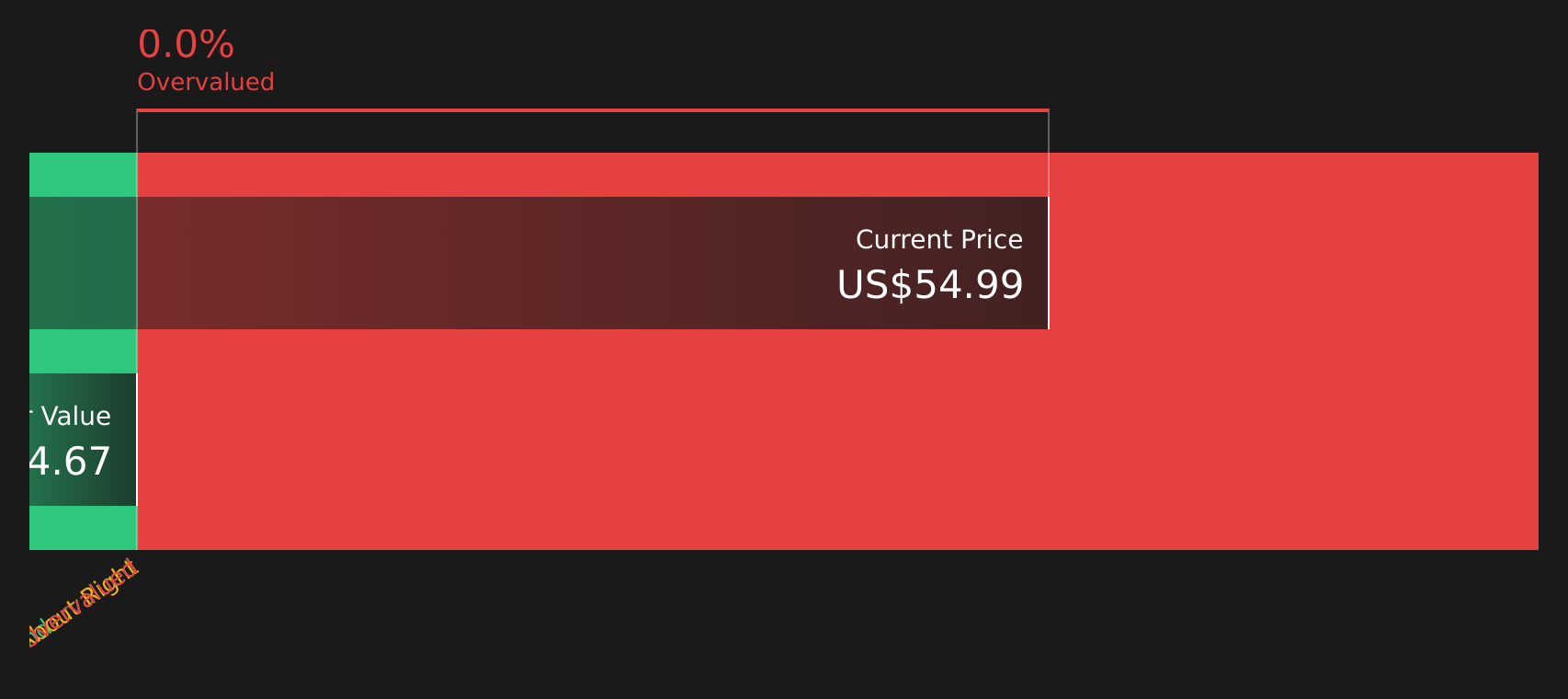

With GRAIL shares around $101 and an average analyst target of $111.25, plus a very large 1-year return, it is reasonable to ask whether there is still a buying opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 3.8% Undervalued

With GRAIL last closing at $101 against a narrative fair value of $105, the most followed view sees modest upside as long term assumptions play out.

Near-term readouts from the 140,000-participant NHS Galleri study and further regulatory milestones position GRAIL for international expansion and partnership opportunities with public health systems globally, potentially driving future earnings and revenue diversification.

Curious what kind of revenue ramp, margin shift, and future earnings multiple are baked into that $105 figure? The story blends rapid growth with punchy profitability assumptions and a premium valuation hurdle. The full breakdown shows exactly how those pieces fit together.

Result: Fair Value of $105 (UNDERVALUED)

However, this story can change quickly if key clinical readouts, such as the NHS Galleri trial, disappoint or if continued high losses and cash burn weigh more heavily on sentiment.

Another Angle on Valuation

The narrative model sees GRAIL as 3.8% undervalued at $105, yet our DCF model points in a very different direction, with an estimate of $27.47, which suggests the shares are expensive on that basis. Which story you lean toward depends on how confident you are in the long term assumptions behind each.

Build Your Own GRAIL Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a full narrative in just a few minutes with Do it your way.

A great starting point for your GRAIL research is our analysis highlighting 1 key reward and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If GRAIL is on your watchlist, do not stop there; use the Simply Wall St Screener to quickly surface fresh ideas that fit your style and goals.

- Spot potential turnaround names by checking out these 3523 penny stocks with strong financials that already show stronger financials than many expect from this corner of the market.

- Ride the AI wave more deliberately by scanning these 24 AI penny stocks that focus on artificial intelligence while still meeting your own quality filters.

- Zero in on value ideas by reviewing these 875 undervalued stocks based on cash flows that currently screen as priced below what their cash flows suggest.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.