Assessing Green Brick Partners (GRBK) Valuation After Renewed Attention And Awards For Its Communities

Green Brick Partners GRBK | 65.35 | -0.03% |

Green Brick Partners (GRBK) is back on investors’ radar after fresh coverage linked the homebuilder to a high-conviction position in David Einhorn’s portfolio and highlighted new awards for its master-planned communities in North Texas.

The latest recognition for its communities comes alongside strong price momentum, with a 30.03% 3 month share price return and a 34.09% 1 year total shareholder return suggesting sentiment has strengthened over both shorter and longer horizons.

If this homebuilder’s run has caught your attention, it could be a good moment to scan the rest of the sector and see which 23 top founder-led companies might deserve a spot on your watchlist.

With shares at $80.59, annual revenue of $2.1b and net income of $335.8m, plus analyst targets sitting below the current price, you have to ask: is Green Brick now fully valued, or could the market still be underestimating future growth?

Most Popular Narrative: 30% Overvalued

At $80.59 per share versus a narrative fair value of $62, Green Brick Partners is framed as richly priced, with the debate centering on how long its current earnings strength and homebuyer demand can hold up.

The company's industry-leading gross margins (over 30% for nine consecutive quarters) and flexible cost structure, including achieved reductions in labor/materials costs and construction cycle times, suggest strong resilience in net margins and potential for earnings stability, even when market incentives and price concessions are required.

Want to see what sits behind that confidence in margins and earnings? The narrative leans heavily on how future revenue, profit margins and the implied P/E multiple all fit together. If you want to understand which assumptions need to hold for $62 to make sense, the full narrative lays out the numbers in detail.

Result: Fair Value of $62 (OVERVALUED)

However, record home closings in key markets and a low net debt position could support earnings and challenge the idea that Green Brick is priced too high.

Another Angle: Earnings-Based Multiple Sends a Softer Signal

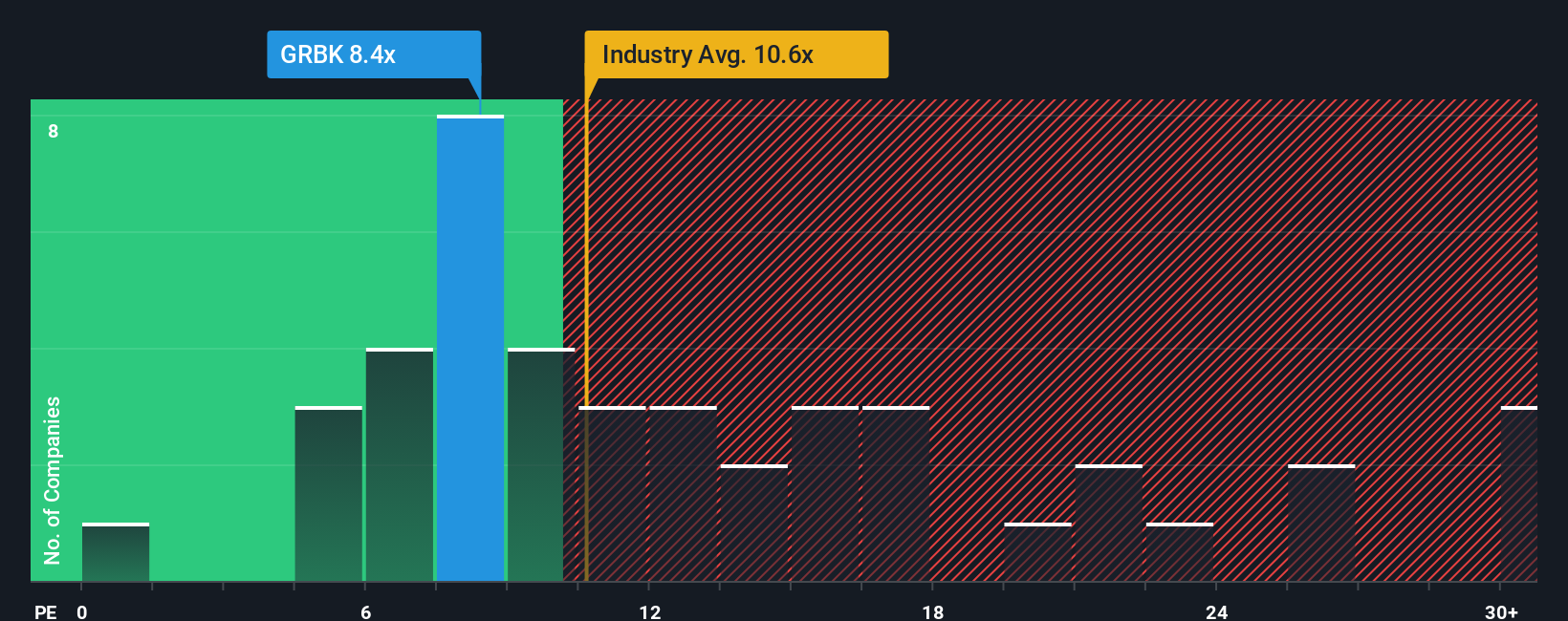

While the narrative fair value of $62 suggests Green Brick Partners looks about 30% overvalued, the current P/E of 10.5x paints a different picture. It sits below both the peer average of 14.3x and the fair ratio of 12.5x, which implies the market could eventually move closer to that higher level.

In practical terms, that gap means the share price already reflects some caution about slower forecast revenue growth of 3.7% a year and a 2% yearly earnings decline, even after a 34.09% 1 year total return. The key question is whether you view that discount as sufficient compensation for the risks that analysts highlight.

Next Steps

With sentiment clearly split, this is a good time to look at the full picture yourself and move quickly from headline to hard data, including 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If this story has you thinking more carefully about where you put your money, now is the moment to widen your search using focused screeners on Simply Wall St.

- Target stability first by checking companies that pass our 81 resilient stocks with low risk scores and see which names might help anchor your portfolio.

- Hunt for value in quality names using the screener containing 24 high quality undiscovered gems and see which underfollowed businesses stand out on fundamentals.

- Prioritise financial strength by reviewing companies highlighted in the solid balance sheet and fundamentals stocks screener (44 results) so you are not missing sturdier alternatives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.