Assessing Group 1 Automotive (GPI) Valuation As Fresh Analyst Buy Ratings Highlight Earnings Potential

Group 1 Automotive, Inc. GPI | 329.45 | -0.41% |

Recent analyst actions, including a new buy initiation from Evercore and positive earnings expectations, have brought Group 1 Automotive (GPI) into focus for investors monitoring sentiment shifts ahead of the next results.

At a share price of US$391.91, Group 1 Automotive has seen a 90 day share price return of 7.56% decline and a 1 year total shareholder return of 12.42% decline, although the 5 year total shareholder return of 194.50% points to stronger longer term momentum than recent trading suggests.

If the recent analyst attention has you reassessing the auto space, it could be a good moment to scan other auto manufacturers that might fit your watchlist next.

With analysts highlighting potential upside to their price targets and the share price recovering from recent declines, the key question now is whether Group 1 Automotive is still trading at a discount or if the market has already priced in future growth.

Most Popular Narrative: 15% Undervalued

Against a fair value narrative of $460.88, Group 1 Automotive's last close at $391.91 reflects a valuation gap that this widely followed view seeks to explain.

The sustained growth in the high margin parts & service (aftersales) segment, driven by an aging vehicle fleet and rising average vehicle age in both the U.S. and U.K., positions Group 1 to capitalize on increasing repair and maintenance needs, which should continue to expand recurring revenue and bolster margins.

Ongoing expansion of technician headcount, investments in service capacity, and focus on customer outreach to owners of older vehicles are set to further increase aftersales throughput, providing earnings stability and margin growth that are less correlated to vehicle sales cycles.

Want to understand why this narrative sees more value than the current price suggests? It is based on steady revenue assumptions, firmer margins, and a lower earnings multiple than many dealers enjoy. Curious which specific earnings and revenue paths have been included in that fair value? The full narrative lays out the playbook in plain numbers.

Result: Fair Value of $460.88 (UNDERVALUED)

However, this depends on Group 1 keeping acquisition risks in check and avoiding margin pressure if online retailers and direct to consumer models gain more ground.

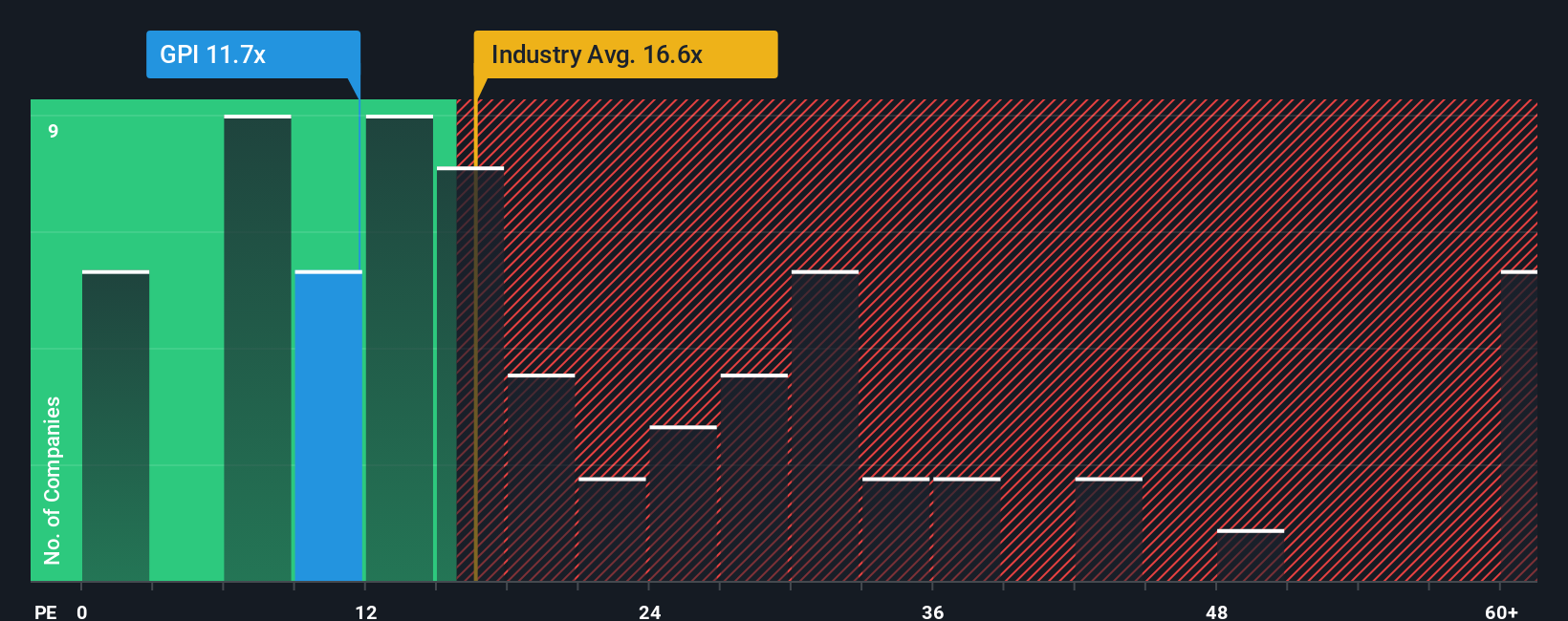

Another View: Market Ratios Paint A Different Picture

While the fair value narrative points to Group 1 Automotive trading at a discount, the market is sending a mixed signal. The current P/E of 13.1x is slightly higher than the peer average of 12.7x, yet sits well below both the US Specialty Retail industry at 20.5x and the fair ratio of 17.5x, which suggests the multiple could shift if sentiment changes.

That gap cuts both ways, as it hints at some valuation risk relative to close peers but also leaves room if the market edges closer to the fair ratio. Which reference point do you think matters more for your own thesis on GPI?

Build Your Own Group 1 Automotive Narrative

If you look at the same numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom view of GPI in just a few minutes with Do it your way.

A great starting point for your Group 1 Automotive research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If GPI has sparked your curiosity, do not stop here. Broaden your watchlist with fresh ideas that line up with your goals before other investors get there first.

- Target long term compounding potential by hunting for companies that our screener flags as these 864 undervalued stocks based on cash flows based on their cash flow profiles.

- Capture the next wave of digital infrastructure by scanning these 18 cryptocurrency and blockchain stocks that are building tools and services around blockchain and digital assets.

- Strengthen your income stream by reviewing these 13 dividend stocks with yields > 3% that currently offer yields above 3% and may complement a core equity portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.