Assessing Hagerty (HGTY) Valuation After Earnings Beat And Extended Markel And Essentia Agreements

Hagerty Inc Class A HGTY | 10.97 | +2.91% |

Why Hagerty Is Back on Investor Radar After Earnings and Partnership Updates

Hagerty (HGTY) is in focus after reporting third quarter 2025 results that topped analyst expectations and after extending key agreements with Markel Group and Essentia Insurance through the end of 2028.

After a strong third quarter, Hagerty’s recent 30 day share price return of an 8.97% decline contrasts with a 12.52% gain over 90 days. Its 1 year total shareholder return of 28.37% and 3 year total shareholder return of 25.80% suggest longer term holders have seen more resilient outcomes. Recent moves likely reflect investors weighing the earnings beat, extended Markel and Essentia agreements, and the impact of insider selling alongside the current US$12.58 share price.

If Hagerty’s latest moves have your attention, it could be a good moment to broaden your search and check out auto manufacturers as another way to spot potential opportunities linked to vehicle demand and enthusiasm.

With Hagerty shares recently at US$12.58 and sitting about 8.6% below the average analyst price target, recent earnings strength and extended partnerships raise a key question: is there real upside left or is future growth already priced in?

Most Popular Narrative: 9.2% Undervalued

Hagerty’s most followed narrative pegs fair value at about $13.86, compared with the recent $12.58 close, setting up an earnings and partnership focused story.

The ramping State Farm partnership is expected to significantly accelerate new business growth, providing access to over 500,000 current program vehicles and thousands of motivated agents, materially expanding Hagerty's customer acquisition funnel and recurring commission revenues at attractive margins over the next several years.

Curious how that kind of distribution reach, margin ambition, and long term earnings build up comes together into one fair value number? The narrative leans on compounded revenue expansion, a sharp profitability shift and a richer earnings multiple to justify that outcome. If you want to see exactly how those moving parts are stitched together, the full story breaks down each step.

Result: Fair Value of $13.86 (UNDERVALUED)

However, this hinges on collector demand and underwriting risk, so softer classic car valuations or higher loss ratios under the Markel risk retention shift could quickly challenge that underpriced story.

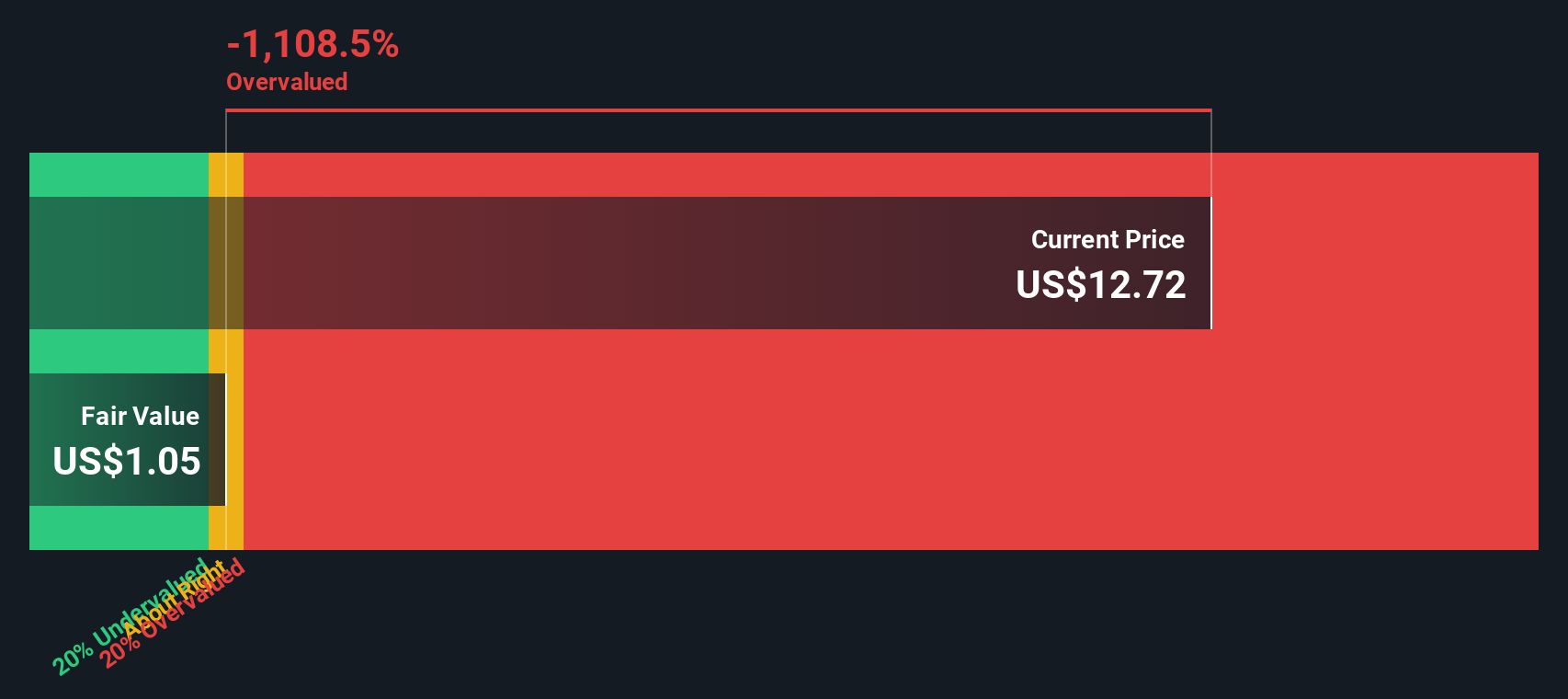

Another Way to Look at Hagerty’s Valuation

That 9.2% undervalued narrative sits awkwardly next to our DCF work, which points to a future cash flow value of about $4.28 per share versus the recent $12.58 price. This implies Hagerty screens as expensive on this method. The real question is which set of assumptions you trust more.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hagerty for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 871 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hagerty Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a complete Hagerty view in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Hagerty.

Looking for more investment ideas?

Do not stop at Hagerty. Widen your watchlist with focused stock groups that line up with how you like to invest and the themes you care about most.

- Target potential growth stories at the smaller end of the market by scanning these 3523 penny stocks with strong financials for businesses that match your risk and return preferences.

- Position yourself in front of accelerating tech trends by reviewing these 23 AI penny stocks and seeing which companies align with your view on artificial intelligence.

- Hunt for possible mispriced opportunities by filtering these 871 undervalued stocks based on cash flows and comparing their fundamentals with the expectations already reflected in current market prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.