Assessing Harley-Davidson (HOG) Valuation After Prolonged Share Price Weakness

Harley-Davidson, Inc. HOG | 20.86 | +2.61% |

Recent share performance and business snapshot

Harley-Davidson (HOG) stock has been under pressure recently, with a decline of about 4% over the past week and about 4% over the past month, extending to roughly 20% over the past 3 months.

Over the past year, the shares show a total return of about a 25% decline, while the 3-year and 5-year total returns are roughly 56% and 41% declines, respectively, against a last close of US$19.46.

The company reports annual revenue of US$4,473.18m and net income of US$338.74m, with annual revenue down about 4% and net income down about 2%, indicating a business that has recently faced some pressure.

Harley-Davidson operates through three segments: Harley-Davidson Motor Company, LiveWire, and Harley-Davidson Financial Services, covering motorcycles, parts, accessories, apparel, electric bikes, and financing products across the United States and international markets.

Harley-Davidson’s recent 1-day share price return of about 0.5% sits against weaker momentum, with a 90-day share price return of roughly 20% decline and a 1-year total shareholder return of about 25% decline. This points to sentiment that has softened rather than strengthened.

If this kind of pressure on a classic brand has you looking at other parts of the market, it could be a good time to check out 22 top founder-led companies as potential long-term compounders beyond the usual names.

With the share price under pressure and the stock trading below the average analyst price target, the key question now is whether Harley-Davidson is undervalued or if the market is already accounting for its future growth.

Most Popular Narrative: 17.2% Undervalued

At a last close of $19.46 versus a narrative fair value of $23.50, the most followed view sees Harley-Davidson trading at a discount, with that gap tied to specific expectations on margins, demand, and cash returns to shareholders.

The new partnership in HDFS unlocks significant cash ($1.25B) and reduces leverage, enabling accelerated share buybacks and freeing up $300M for growth investments, which can directly support EPS and future revenue streams through both financial engineering and new business initiatives.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue path, margin rebuild, and earnings multiple are baked into that fair value? The narrative leans on specific forecasts for shrinking sales, higher profitability, and fewer shares outstanding. If you want to see exactly how those moving parts combine into $23.50, the full story sits behind that link.

Result: Fair Value of $23.50 (UNDERVALUED)

However, if weak motorcycle demand persists or tariffs land toward the higher end of the US$50m to US$85m range, the margin story behind that fair value could quickly look fragile.

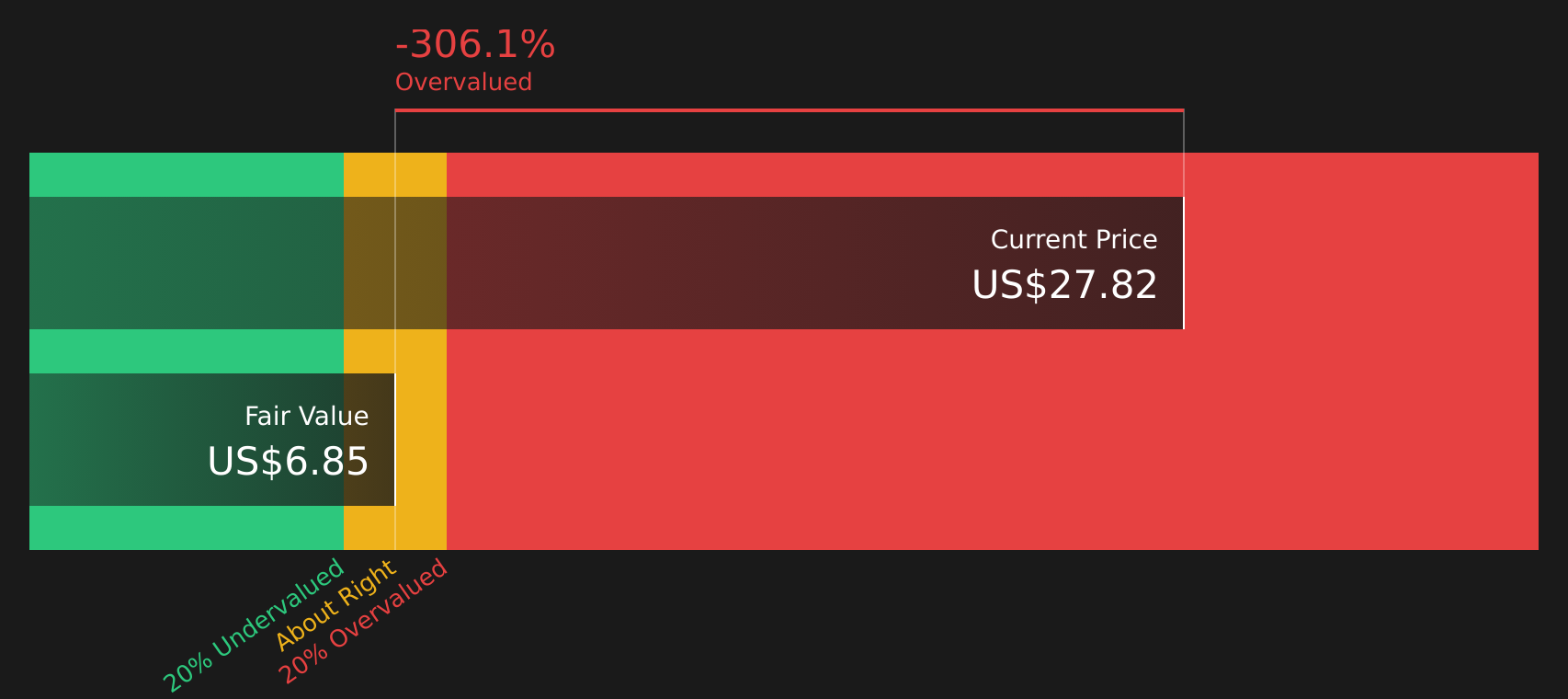

Another Angle: Cash Flows Paint A Tougher Picture

While the narrative fair value of $23.50 suggests Harley-Davidson might be undervalued, our DCF model comes to a different conclusion. On this view, the shares at $19.46 sit above an estimated future cash flow value of $14.84, which points to a stock that could be pricing in more optimism than its cash generation supports. Which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Harley-Davidson for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After all this, do you feel the story leans more positive or cautious? Take a close look at the full picture and move quickly to form your own view, starting with 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Harley-Davidson has sharpened your focus, do not stop here. Broaden your watchlist with other ideas that match your style and risk comfort.

- Target value opportunities by scanning our list of 51 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial profile.

- Strengthen your income stream by reviewing 16 dividend fortresses, highlighting companies that offer higher-yield payouts backed by more resilient cash flows.

- Protect the downside by checking 78 resilient stocks with low risk scores, featuring businesses that score better on balance sheet strength and overall risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.