Assessing Hilltop Holdings (HTH) Valuation As Recent Returns Send Mixed Signals

Hilltop Holdings Inc. HTH | 0.00 |

What Hilltop Holdings (HTH) offers investors right now

Hilltop Holdings (HTH) is drawing attention after a period of mixed share performance, with a roughly 5.8% gain over the past month alongside a 4.3% decline over the past 3 months.

For investors watching regional banks, the stock sits around $38.12 at the last close, supported by a business that spans banking, broker dealer activities, and mortgage origination across the United States.

Looking beyond the recent 5.8% 1 month share price return, Hilltop Holdings has a 12.45% year to date share price return and a 29.97% 1 year total shareholder return. This points to improving momentum supported by dividends over the longer period.

If you are comparing Hilltop with other financials and yield oriented ideas, it can help to broaden your watchlist using tools like the 20 top founder-led companies

With Hilltop trading near US$38.12 and sitting only about 4% below the average analyst price target of roughly US$39.67, you may want to consider whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 4% Undervalued

Hilltop Holdings' most followed narrative pegs fair value around $39.67, slightly above the recent $38.12 close. That puts a tight focus on the assumptions behind that gap.

Continuing growth and strong demand for loans in Texas and across the Sun Belt, fueled by population gains and robust economic conditions, are expected to drive increases in lending volume and recurring revenue streams as Hilltop's loan pipeline remains healthy and pipelines in commercial lending continue to expand.

Read the complete narrative. Read the complete narrative.

Interested in why a regional bank story supports this valuation? The narrative leans on measured revenue expansion, thinner profit margins, and a richer future earnings multiple than the sector. The precise mix of those inputs is what really drives that $39.67 fair value marker.

Result: Fair Value of $39.67 (UNDERVALUED)

However, you still need to keep an eye on Hilltop's reliance on mortgage origination and Texas exposure, as these factors could amplify housing or regional downturn pressure.

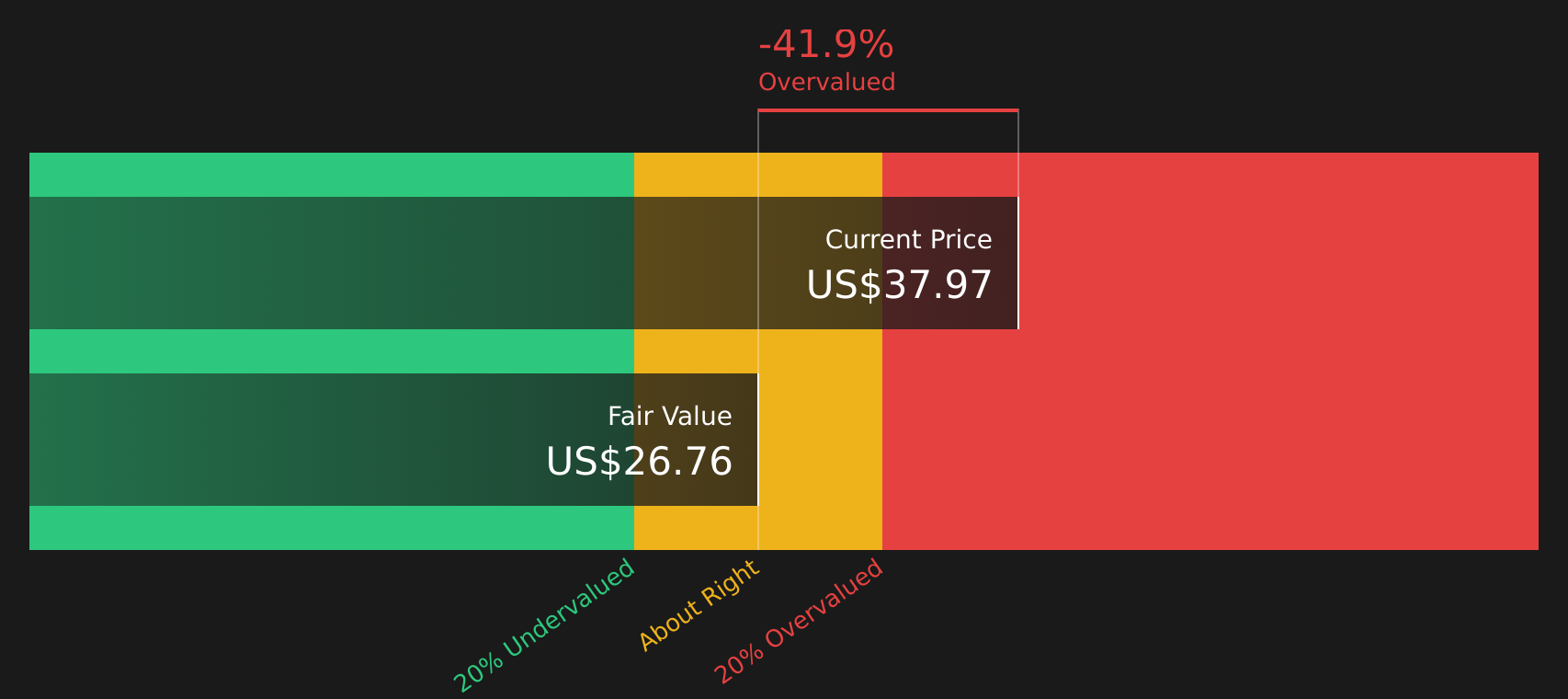

Another way to look at HTH’s value

Analysts see Hilltop as about 4% undervalued based on their fair value estimate, but the SWS DCF model paints a different picture. On that view, the current $38.12 price sits above an estimated future cash flow value of $26.60, which points to an overvalued stock instead.

This kind of gap between an earnings based target and a cash flow driven model often comes down to how optimistic you are about future margins and loan growth. Which do you trust more for a regional bank with mixed growth forecasts: headline multiples or long range cash flow assumptions?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hilltop Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages on value and future prospects can be confusing. It helps to review the numbers yourself, weigh both sides, and focus on the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Hilltop has your attention, do not stop your research here. Your next strong opportunity could be sitting in plain sight among similar stocks.

- Target potential bargains by scanning companies that combine quality fundamentals with attractive prices using the 47 high quality undervalued stocks.

- Strengthen your income focus by reviewing stocks built around reliable payouts with the 12 dividend fortresses.

- Prioritise resilience by checking companies that score well on financial stability through the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.