Assessing Hims & Hers Health (HIMS) Valuation As Estimate Cuts And Big Game Ad Campaign Shape Sentiment

Hims & Hers Health, Inc. Class A HIMS | 19.14 | -3.53% |

Recent earnings estimate cuts, insider selling and rising implied volatility have put Hims & Hers Health (HIMS) under pressure, while a high profile “Big Game” ad campaign is drawing fresh attention to its telehealth model.

The recent 1 month share price return of 15.92% decline and 3 month share price return of 34.93% decline suggest momentum has cooled, even though the 3 year total shareholder return of about 2.6x still reflects a strong longer term outcome. Recent estimate cuts, insider selling disclosures and increased options activity are feeding a more cautious tone around risk, while the “Rich People Live Longer” Big Game campaign points to management focusing on brand building as telehealth competition and regulation remain in focus.

If this kind of telehealth volatility has your attention, it could be a good time to scan other healthcare stocks that might offer different growth and risk profiles.

With Hims & Hers now trading at a discount of about 45% to the average analyst price target and an estimated intrinsic discount of roughly 55%, the key question is whether this signals mispricing or whether markets are already incorporating potential future growth risks.

Most Popular Narrative: 83.4% Undervalued

Compared with the last close at $28.67, the most followed narrative pegs Hims & Hers Health at a fair value of $173.02, a wide gap that frames a very optimistic upside story.

Over the long term, Hims & Hers has an unusually large addressable market ahead of it. The company’s growth is driven by three reinforcing dimensions:

• Expanding market size, as digital healthcare adoption continues to grow globally

• Category expansion, with new offerings such as hormonal health, longevity, and sleep

• International scaling, with multiple geographies already in the pipeline (e.g. Brazil, Australia). Together, these form a multi-dimensional growth model that is described as providing durable tailwinds for many years. With several countries and categories still to be launched, sustaining ~40% annual revenue growth is presented as achievable without relying on what the narrative views as aggressive assumptions.

According to Deep_Insights, this fair value leans heavily on assumptions of strong revenue expansion, higher profitability and a premium future earnings multiple. The details focus on which specific growth drivers and margin targets contribute most, and how weight loss scenarios are incorporated into that narrative.

Result: Fair Value of $173.02 (UNDERVALUED)

However, this upbeat view still runs into real pressure points, including ongoing GLP 1 and weight loss uncertainty, as well as the risk that heavy investment fails to translate into sustained profitability.

Another View: Earnings Multiple Paints A Tougher Picture

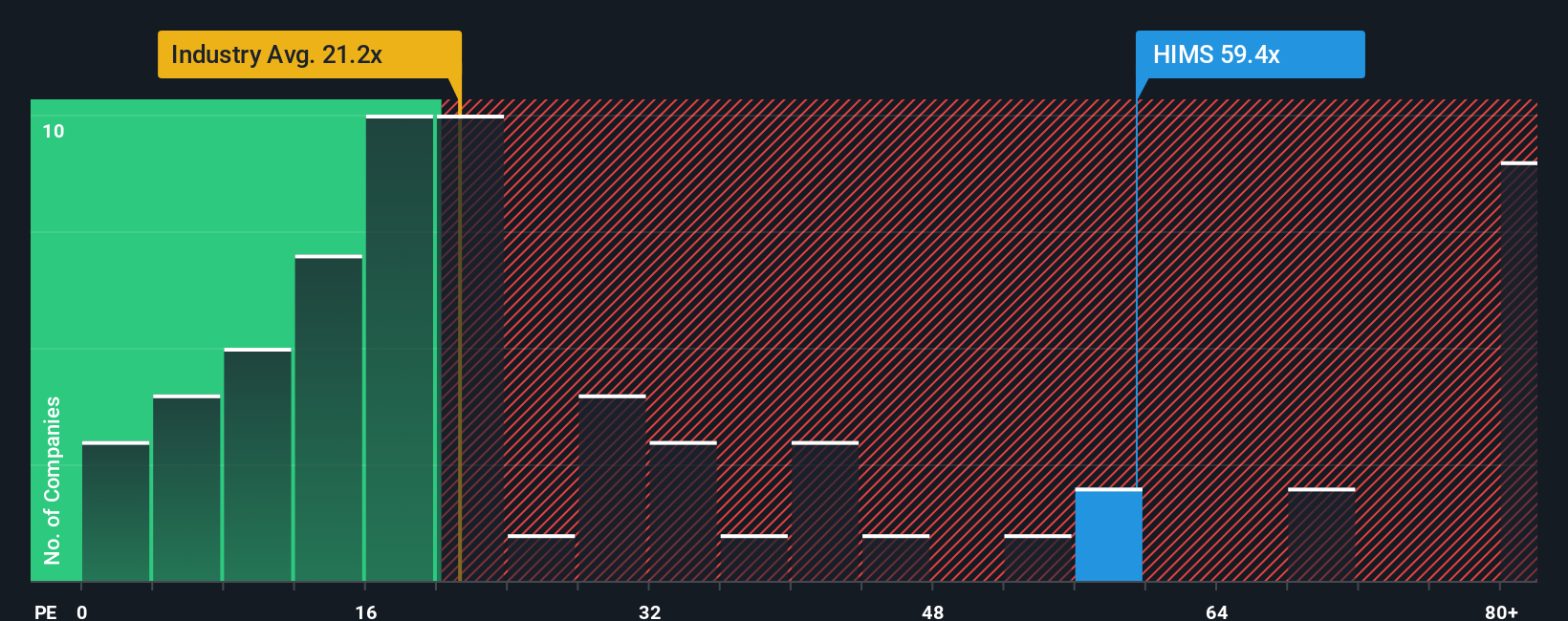

The SWS DCF model suggests Hims & Hers is undervalued, but the earnings multiple tells a different story. At a P/E of 48.8x versus a fair ratio of 27.1x, the gap is wide. The US Healthcare average is 22x and peers sit around 33x, which raises the question of how much optimism is already baked into the price.

Build Your Own Hims & Hers Health Narrative

If you see the numbers differently or want to stress test your own assumptions against this data, you can build a custom view in minutes: Do it your way.

A great starting point for your Hims & Hers Health research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Hims & Hers got you thinking, do not stop here. A few minutes with the right screeners can surface ideas you will not want to miss.

- Zero in on potential value opportunities by scanning these 868 undervalued stocks based on cash flows that some investors might be overlooking right now.

- Ride the wave of artificial intelligence by checking out these 23 AI penny stocks that are building real businesses around this theme.

- Tap into long term income potential by reviewing these 14 dividend stocks with yields > 3% that offer yields above 3% with different risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.