Assessing Honest Company (HNST) Valuation After Mixed Earnings And Business Exit Plans

Honest Company, Inc. HNST | 2.82 | +1.44% |

Honest Company (HNST) is back in focus after reporting mixed earnings, with profits ahead of expectations but sales lagging, and announcing plans to exit the Canadian market and its baby apparel business.

The latest announcements appear to be weighing on sentiment, with Honest Company’s 90 day share price return of a 28.45% decline and 1 year total shareholder return of a 63.58% loss pointing to fading momentum even as management refocuses the business.

If this kind of business reset has you thinking more broadly about your portfolio, it could be a good moment to look at fast growing stocks with high insider ownership as a fresh source of ideas.

With Honest Company posting annual revenue of US$383.1m and net income of US$7.1m, yet carrying a 1 year total shareholder return loss of 63.58%, investors may ask whether this weakness is overdone or whether the market is already discounting future growth.

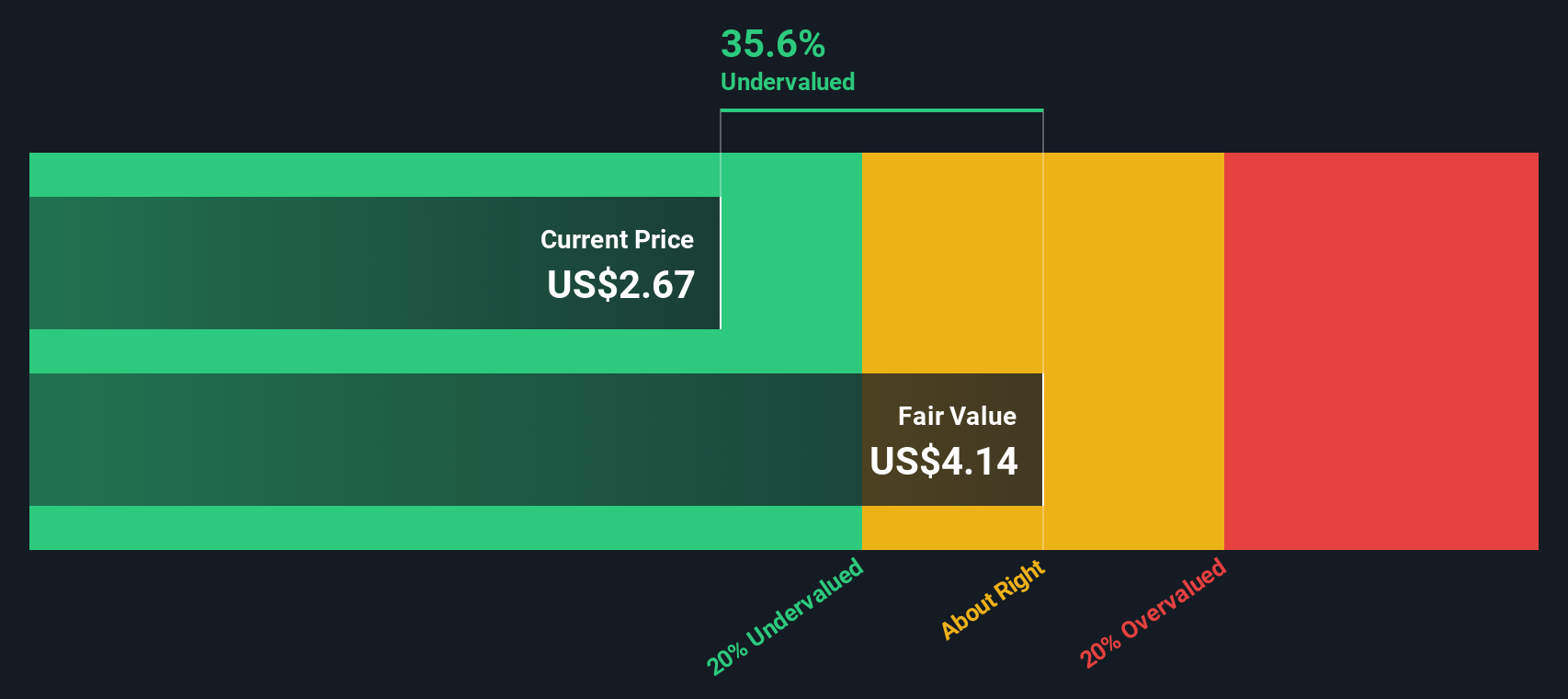

Most Popular Narrative: 36.3% Undervalued

With Honest Company last closing at $2.44 against a narrative fair value of $3.83, the widely followed view implies a meaningful valuation gap that hinges on how its reset plays out.

Disciplined focus on operational improvements, margin enhancement, and tariff mitigation (evidenced by record gross margin, positive net income, and improved cost structure) is expected to further improve net margins and earnings resilience over the long term, especially as marketing and supply chain investments drive increased efficiency.

Curious what is behind that higher fair value? The narrative leans heavily on steady earnings growth, firmer margins, and a richer future earnings multiple. The exact mix of those ingredients might surprise you.

Result: Fair Value of $3.83 (UNDERVALUED)

However, this depends on tariff exposure and softer diaper demand not undercutting margins or revenue more than expected, which could quickly challenge that higher fair value.

Another Angle on Valuation

That $3.83 fair value hinges on earnings forecasts and a premium P/E in future. Our take using the SWS DCF model is different, with an estimate of $1.38 per share. This suggests Honest Company is trading above that cash flow based value and raises the question of which story you trust more.

Build Your Own Honest Company Narrative

If the numbers or assumptions here do not quite match your view, you can dig into the data yourself and build a fresh narrative in minutes, starting with Do it your way.

A great starting point for your Honest Company research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more stock ideas?

If Honest Company has you rethinking your next move, do not stop here. Let Simply Wall St's screeners help you spot opportunities you might otherwise miss.

- Target potential turnaround stories by checking out these 3526 penny stocks with strong financials that already back their share price with stronger financials.

- Position yourself for the next wave of automation by looking at these 23 AI penny stocks that link artificial intelligence themes with early stage pricing.

- Zero in on value led opportunities using these 865 undervalued stocks based on cash flows where current prices sit below cash flow based estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.