Assessing HubSpot (HUBS) Valuation After A Steep One Year Share Price Pullback

HubSpot, Inc. HUBS | 244.67 | +0.77% |

Why HubSpot is on investors’ radar now

HubSpot (HUBS) has been under pressure, with the share price showing negative returns over the past day, week, month and past 3 months, which is prompting some investors to reassess the stock.

At a last close of US$304.79, HubSpot sits against a backdrop of mixed fundamental signals, including positive annual revenue and net income growth, alongside a reported net loss in absolute dollar terms.

The recent 1 day share price return of 2.27% decline and 7 day share price return of 15.07% decline sit within a much steeper 1 year total shareholder return of 58.02% decline. This suggests momentum has been fading as investors reassess both growth potential and risk around HubSpot’s CRM-focused model.

If HubSpot’s pullback has you rethinking your tech exposure, it could be a good moment to scan other high growth tech and AI stocks that are catching attention in the software and AI space.

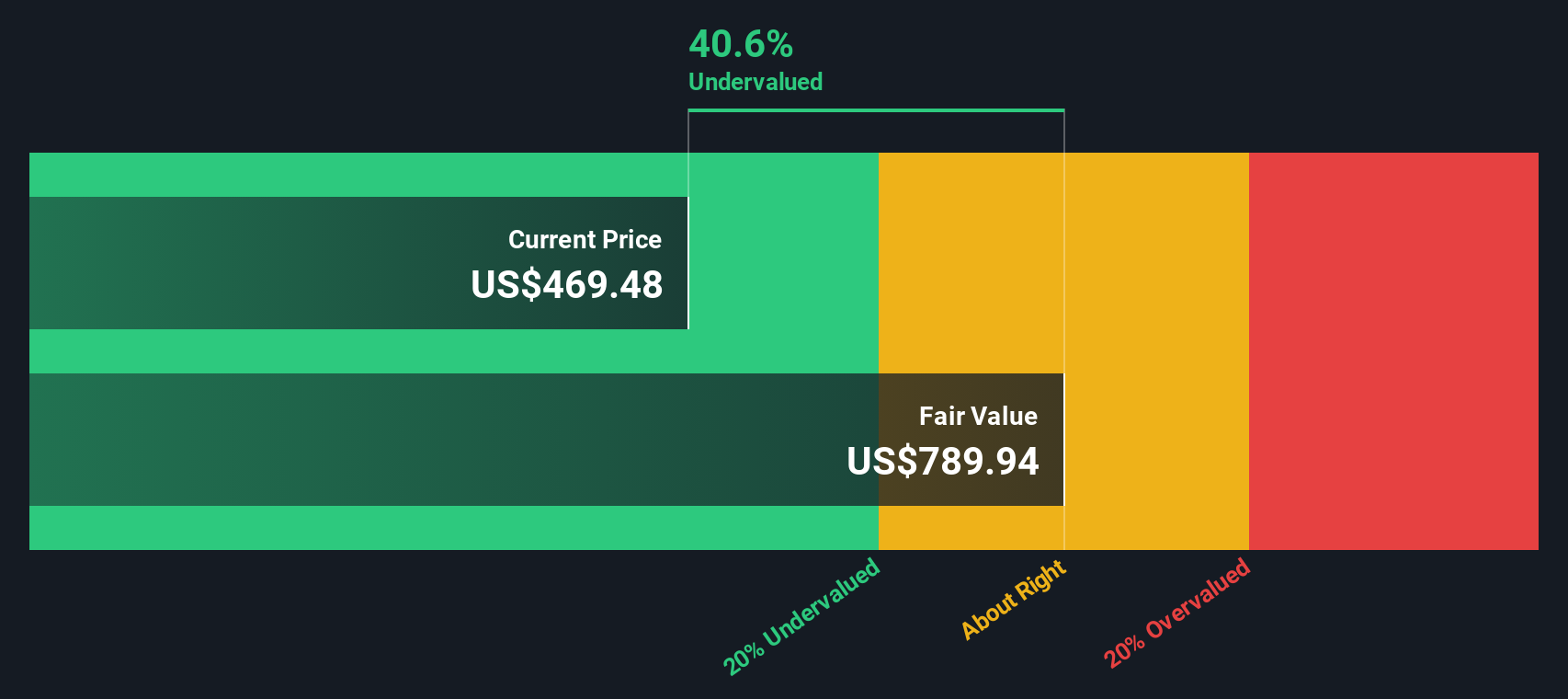

With HubSpot shares down 58.02% over the past year despite annual revenue and net income growth, and trading at a reported intrinsic discount, the key question is simple: is this a reset that creates opportunity, or is the market already pricing in future growth?

Price-to-Sales of 5.3x: Is it justified?

On a P/S of 5.3x at a last close of US$304.79, HubSpot screens as good value versus some peers and fair value models, even though the share price has been under pressure.

P/S compares the company’s market value to its revenue, which is often used for software and CRM names where profits are still developing or currently negative.

For HubSpot, the SWS checks flag that a 5.3x P/S is below the peer average of 7.1x and below an estimated fair P/S of 9.3x. The shares also trade 39.1% below an internal fair value estimate of US$500.76 and 87.1% below the average analyst price target of US$570.36.

Against the wider US software industry, however, HubSpot’s 5.3x P/S sits above the sector average of 4.7x. This suggests the market is still assigning a premium multiple even as some models point to room for the ratio to move closer to the higher fair level.

Result: Preferred multiple of 5.3x Price-to-Sales (UNDERVALUED)

However, there are clear risks, including HubSpot’s net loss of US$3.532m and the potential for investor sentiment to remain weak after a 58.02% 1 year decline.

Another angle on value: our DCF model

The SWS DCF model paints a similar picture to the P/S work. With HubSpot at US$304.79 compared with our DCF fair value estimate of US$500.76, the shares screen as undervalued on cash flow assumptions as well as on sales multiples.

For you, the real question is whether those cash flow assumptions and revenue forecasts feel reasonable, or if they build in more optimism than you are comfortable with.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out HubSpot for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own HubSpot Narrative

If you see the numbers differently or prefer to weigh the data yourself, you can shape a full HubSpot story in a few minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding HubSpot.

Looking for more investment ideas?

If HubSpot is on your watchlist, do not stop there; lining up a few contrasting ideas can sharpen your judgement and reveal what really stands out.

- Spot potential value movers by scanning these 872 undervalued stocks based on cash flows that the model flags as trading below their estimated cash flow based valuations.

- Ride the AI trend with focus by checking these 24 AI penny stocks that tie real revenue to artificial intelligence rather than just hype.

- Strengthen your income watchlist by reviewing these 13 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.