Assessing Huntington Bancshares (HBAN) Valuation After Category III Shift And Cadence Integration Moves

Huntington Bancshares Incorporated HBAN | 15.79 | -0.57% |

Huntington Bancshares (HBAN) is drawing fresh attention after its merger with Cadence Bank pushed the lender into Category III status, accompanied by the appointment of a new Chief Risk Officer and the addition of former Cadence directors to the board.

Those board changes, executive moves and the upcoming UBS conference presentation come during a solid run in the stock, with a 20.1% 3 month share price return and a 64.13% 5 year total shareholder return suggesting momentum has been building rather than fading.

If this kind of bank reshaping has your attention, it could be a good moment to widen your search and check out 22 top founder-led companies as potential next ideas to research.

With HBAN trading at $19.00, sitting below an analyst price target of $20.50 and an indicated intrinsic value gap, the real question is whether there is still mispricing here or whether the market already reflects the future growth story.

Most Popular Narrative: 87.9% Overvalued

Compared with the last close at $19.00, the most followed narrative assigns Huntington Bancshares a fair value of $10.11, which implies a steep premium in the current price.

Huntington Bancshares (HBAN) is currently trading around $14.56, with analysts offering a consensus 12-month price target of $15.59, suggesting a potential upside of around 7%. The stock has been rated as a "Moderate Buy" by most analysts, with 12 out of 19 giving it a "Buy" or "Strong Buy" recommendation.

Curious what justifies a fair value well below today’s price? According to mschoen25, it hinges on profit margins, future earnings power and the valuation multiple the bank is assumed to hold onto over time. The full narrative spells out how those ingredients combine into that overvaluation call.

Result: Fair Value of $10.11 (OVERVALUED)

However, this overvaluation call could be challenged if HBAN’s 19.8% revenue growth and 17.5% net income growth support a higher sustained profit margin or different P/E assumptions.

Another Take: Cash Flows Point the Other Way

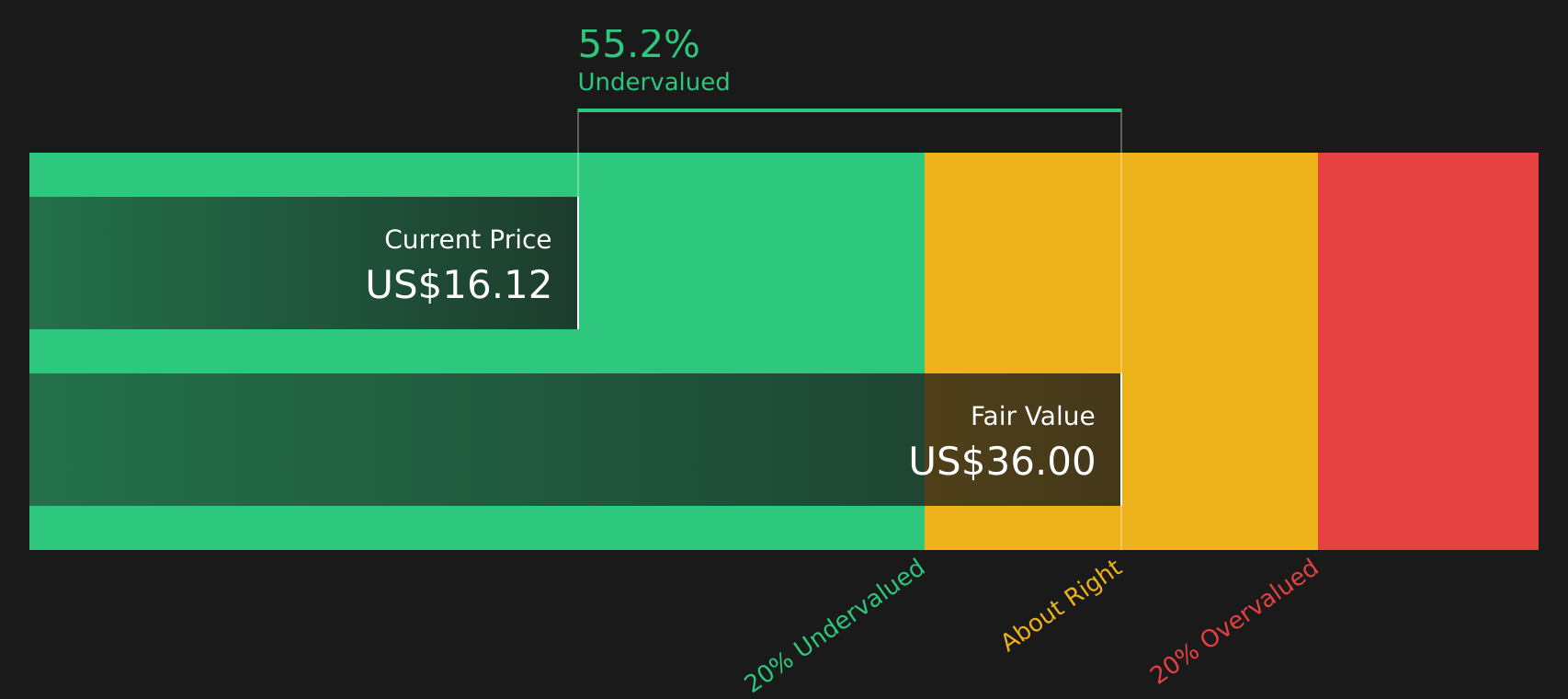

The user narrative flags Huntington Bancshares as 87.9% overvalued at a fair value of $10.11, yet our DCF model points in the opposite direction. With our future cash flow value estimate at $35.70 versus a $19.00 share price, the DCF view suggests the shares are trading at a sizeable discount. When one framework says expensive and another says cheap, which set of assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Huntington Bancshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Huntington Bancshares Narrative

If you are not convinced by any of these views or prefer to lean on your own research, you can pull the numbers together and build your own take in just a few minutes, starting with Do it your way.

A great starting point for your Huntington Bancshares research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Huntington has you thinking about what else might be out there, do not stop here. Broaden your watchlist with other well screened opportunities worth your attention.

- Target consistency and peace of mind by checking companies in our 82 resilient stocks with low risk scores that may suit a more cautious approach.

- Spot potential value opportunities early by reviewing screener containing 24 high quality undiscovered gems before they land on everyone else's radar.

- Focus on financial strength first by scanning the solid balance sheet and fundamentals stocks screener (45 results) for businesses with sturdier foundations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.