Assessing ICL Group (NYSE:ICL) Valuation After Strong Q1 2026 Results And Higher Dividend Guidance

ICL Group Ltd. ICL | 0.00 |

ICL Group (NYSE:ICL) is back in focus after first quarter 2026 results showed sales of US$2,023 million and net income of US$126 million, along with a higher dividend and raised EBITDA guidance.

ICL Group's recent first quarter update and higher dividend come after a 22.33% 1 month share price return and 10.71% year to date share price return, while the 1 year total shareholder return is slightly negative, suggesting momentum has picked up recently after a softer longer term experience.

If ICL's recent move has you thinking about other materials related opportunities, this is a good moment to scan 30 best rare earth metal stocks

With revenue at US$2,023 million, net income at US$126 million, a higher dividend, and raised EBITDA guidance all now in the open, you have to ask whether ICL is still undervalued or if the market is already pricing in future growth.

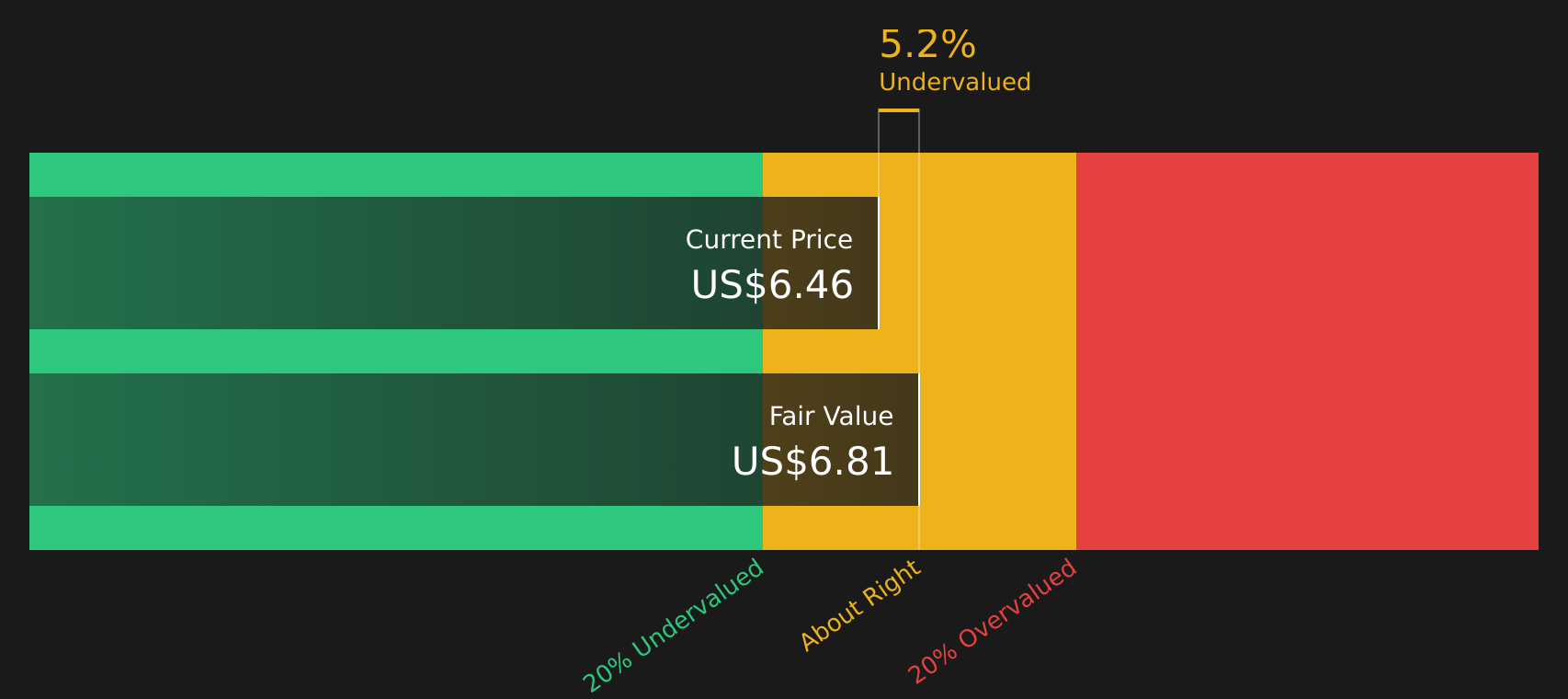

Most Popular Narrative: 4.9% Undervalued

ICL Group's most followed narrative pegs fair value at $6.74, a touch above the last close of $6.41. This keeps the focus firmly on the assumptions behind that gap.

The company's strategy to expand its product pipeline and innovate across business segments implies significant investment. If these projects, such as those in battery materials, do not meet expected returns, net margins and earnings could suffer.

Curious what justifies a higher fair value with slower revenue growth and a steeper discount rate baked in? The narrative leans on changing margins, future earnings power, and how the business mix evolves over time. The numbers behind that story are anything but simple.

Result: Fair Value of $6.74 (UNDERVALUED)

However, there are still clear watchpoints, including geopolitical tensions that could raise costs and the heavy spending on new projects that may not deliver the expected returns.

Another View: DCF Points The Other Way

The popular narrative sees ICL Group as 4.9% undervalued with a fair value of $6.74, slightly above the last close of $6.41. However, the Simply Wall St DCF model estimates fair value at $4.69, which would imply the stock is trading above its future cash flow value and could be overvalued instead. That is a very different message for anyone relying on growth and margin assumptions.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ICL Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mixed signals on value and risks make this a moment to look closely at the numbers yourself and decide what really matters for you, including 5 important warning signs.

Looking for more investment ideas?

If ICL has your attention, do not stop here. Use this momentum to broaden your watchlist and pressure test your thesis against other opportunities.

- Spot potential long-term value by scanning 51 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their financial strength.

- Target consistency and income potential by reviewing 14 dividend fortresses that focus on higher yields supported by resilient business profiles.

- Prioritise capital preservation by checking 66 resilient stocks with low risk scores designed to highlight companies with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.