Assessing IDT (IDT) Valuation After Retail Strength And BOSS Money Tax Tailwind

IDT Corporation Class B IDT | 51.16 | +3.02% |

IDT (IDT) is back on investor radars after fresh data on its National Retail Solutions segment and new U.S. remittance tax rules highlighted potential implications for both its retail and BOSS Money businesses.

Despite the strong same store sales data from NRS and the potential boost to BOSS Money from the new remittance tax, IDT’s recent share price momentum has been soft, with a 30 day share price return of 6.43% decline and a year to date share price return of 5.56% decline, while the 5 year total shareholder return of 157.49% still points to a much stronger long term outcome.

If this has you thinking about other ways to position your portfolio around payments and infrastructure themes, it could be worth scanning 23 top founder-led companies as a starting list of founder led companies with distinct business models.

With the shares soft in the short term, a value score of 3, an intrinsic value estimate above the current US$47.76 price and an US$80 analyst target on the table, is there a genuine opportunity here or is future growth already priced in?

Most Popular Narrative: 40.3% Undervalued

Compared with the $47.76 last close, the most followed narrative pegs IDT’s fair value at $80, which implies a sizable valuation gap in that framework.

The company's intention to continue repurchasing shares and increasing dividends, backed by strong cash generation, suggests improved earnings per share (EPS) growth potential.

With ongoing subscription revenue growth and strategic investments in AI and digital channels, net2phone's future performance is expected to boost revenue and improve adjusted EBITDA margins.

Curious what kind of revenue profile and margin path support that $80 figure, and why the implied future P/E needs to step up from today’s level? The full narrative lays out a detailed earnings bridge, the assumed share count path and the required valuation re rating that ties those pieces together.

Result: Fair Value of $80 (UNDERVALUED)

However, this depends on BOSS Money’s working capital needs remaining under control and foreign exchange movements not eroding reported growth or margins.

Another Angle On Valuation

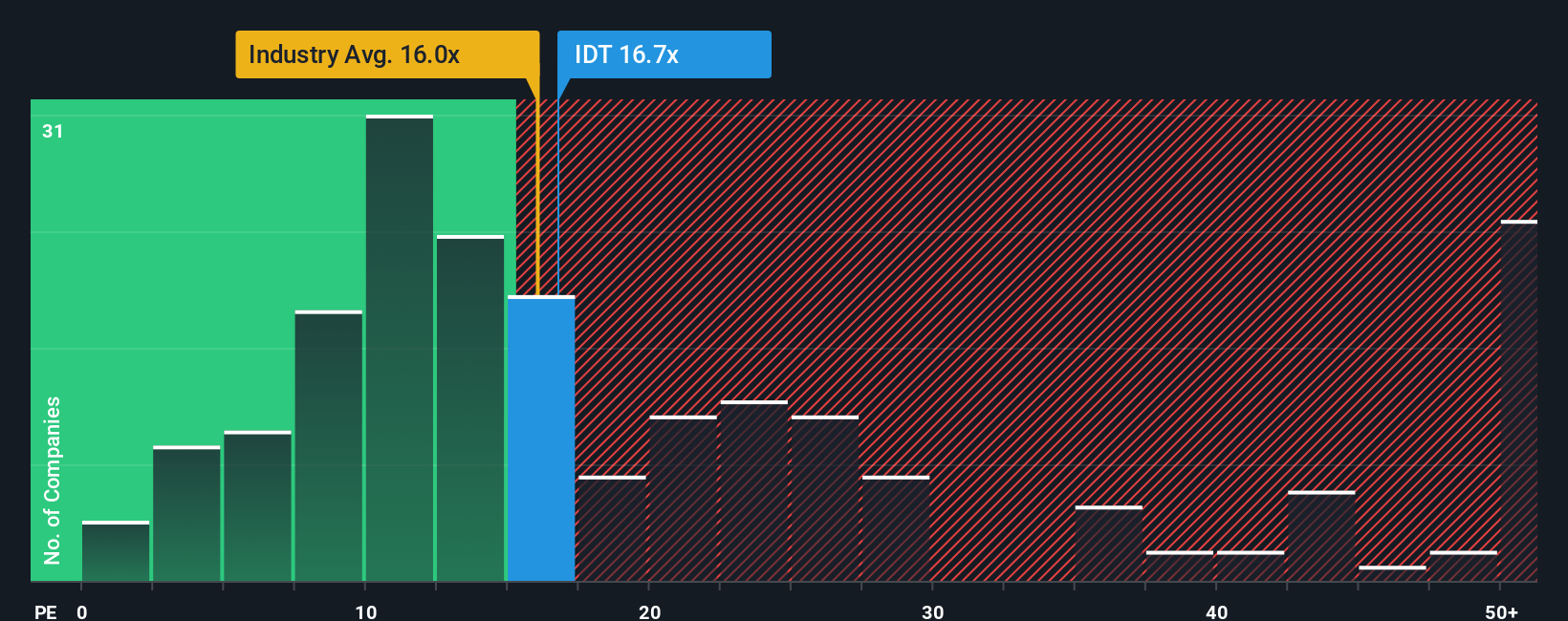

On earnings, the picture is less clear cut. IDT trades on a 14.7x P/E, which is cheaper than the global Telecom average of 16.4x, but above its own fair ratio of 12.6x and well ahead of the 6x peer average. That mix of discounts and premiums raises a simple question: is this really a bargain or just fairly priced quality?

Build Your Own IDT Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a custom IDT view in minutes by starting with Do it your way.

A great starting point for your IDT research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop your research with IDT, you could miss other compelling setups that fit your style, so keep casting the net wider with a focused stock search.

- Target potential mispricings by scanning our list of 55 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their business quality.

- Strengthen your income stream by reviewing 16 dividend fortresses that aim to pair higher yields with resilient business models.

- Prioritise resilience by checking out 85 resilient stocks with low risk scores designed to highlight companies with more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.