Assessing Intuitive Machines (LUNR) Valuation After New Lunar Contracts And Backlog-Driven Revenue Growth

Intuitive Machines LUNR | 0.00 |

Why Intuitive Machines stock is back in focus

Intuitive Machines (LUNR) has drawn fresh attention after being named prime contractor for key lunar imaging instruments and reporting first quarter results that combined higher revenue with a wider net loss and record backlog.

Those new lunar imaging contracts and the revenue jump have arrived alongside powerful momentum in the stock, with a 30 day share price return of 49.86% and a year to date share price return of 113.98%. The 1 year total shareholder return of 237.39% and 3 year total shareholder return of about 4.7x suggest recent enthusiasm has been building for some time.

If you are watching space related and automation themes more broadly, this is a good moment to scan the market and check out 35 robotics and automation stocks

With Intuitive Machines stock up sharply, trading near its analyst price target of $38 and still showing a large implied intrinsic discount, it is worth asking whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 66.3% Overvalued

Compared with the last close at $38.26, the most followed narrative pegs Intuitive Machines' fair value at $23.00, which points to a sizable valuation gap.

While LUNR’s 63.72% growth profile is fundamentally sound, the market is currently pricing in a flawless execution of every lunar mission. Considering the $15M in recent insider selling within the $23 to $25 range and the high 1.4 beta volatility, we view $23.21 as the objective "Going Concern" value. This provides a necessary buffer for investors against the inherent execution risks of the lunar economy.

Want to see what sits behind that going concern value and dilution callout? The narrative leans heavily on projected revenue expansion, margin shifts and a future earnings inflection. The key is how those moving parts stack up against a much larger share count and rising data services contribution.

Result: Fair Value of $23.00 (OVERVALUED)

However, recent insider selling and the need to execute multiple complex lunar missions cleanly could both challenge the assumption that the current premium is justified.

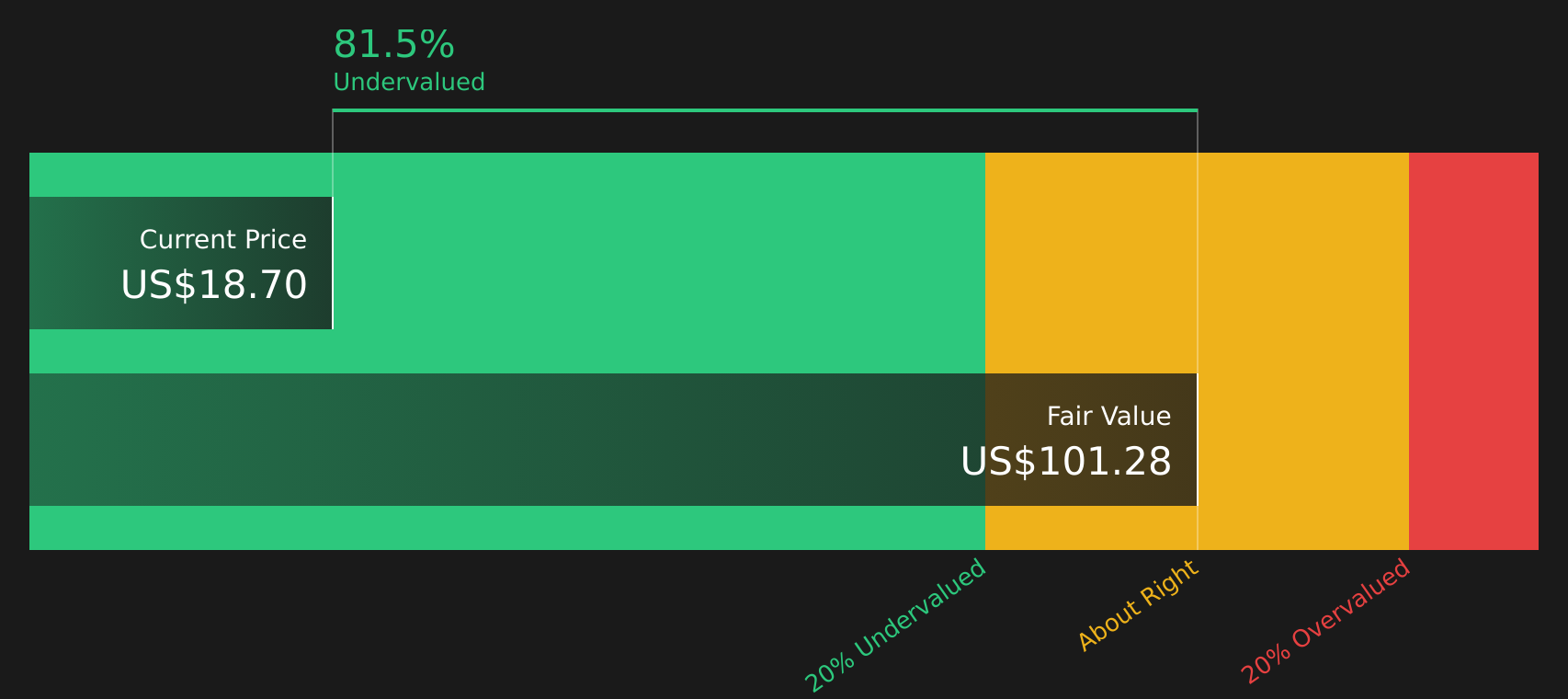

Another View: DCF Paints a Very Different Picture

The first narrative leans on revenue multiples and concludes that Intuitive Machines looks overvalued around $38, but our DCF model points the other way. In that approach, the stock trades at roughly a 64% discount to an estimated future cash flow value of $105.29. For you as an investor, that raises a simple question: which story feels more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Intuitive Machines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between rich valuation and potential upside, this is the moment to move quickly, review the numbers, and weigh both the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If this story has you thinking more broadly about your portfolio, now is the time to hunt for fresh ideas instead of waiting on the sidelines.

- Spot potential bargains early by checking out screener containing 21 high quality undiscovered gems before other investors start paying attention.

- Strengthen your core holdings with the solid balance sheet and fundamentals stocks screener (46 results) and focus on companies with financial foundations that may better handle tough conditions.

- Cut down on unnecessary volatility by reviewing the 69 resilient stocks with low risk scores and see which stocks line up with a steadier approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.