Assessing Intuitive Surgical (ISRG) Valuation After 2026 da Vinci Growth Outlook And AI Recurring Revenue Update

Intuitive Surgical, Inc. ISRG | 452.07 | -2.67% |

Intuitive Surgical (ISRG) has updated investors on its 2026 outlook, guiding for 13% to 15% global da Vinci procedure growth, supported by U.S. general surgery, broader international adoption, and the commercial rollout of the da Vinci 5 system.

That 13% to 15% procedure growth outlook comes after a choppy stretch for the share price, with a 30 day share price return of 11.14% and a year to date share price decline of 13.55%, while the 3 year total shareholder return of 103.36% signals strong long run compounding despite the recent pullback.

If Intuitive Surgical’s update has you rethinking where robotics and AI might fit in your portfolio, this could be a time to scan 25 healthcare AI stocks for potential next ideas to research.

With shares down 18.42% over the past year but still trading at levels that reflect strong expectations, investors are left with a key question: Is Intuitive Surgical a rare chance to buy quality on sale, or is the market already pricing in years of future growth?

Most Popular Narrative: 18.5% Undervalued

The most followed narrative puts Intuitive Surgical’s fair value at $596.36, above the last close of $485.84. That frames the current pullback in a very different light.

Ongoing product innovation (including full launch of da Vinci 5, integrated force feedback, and digital/AI case insights), coupled with R&D to expand into adjacent specialties, enhances clinical outcomes and surgeon efficiency supporting future procedure growth, higher system ASPs, and increased recurring instrument and accessory revenues.

Curious what earnings, margins, and future valuation multiple have to look like to back that price? The narrative leans on ambitious growth and a premium P/E to get there. The full breakdown shows exactly how those assumptions line up year by year.

The fair value estimate uses a 7.68% discount rate and incorporates double digit revenue expansion, gradually improving profitability, and a forward earnings multiple above many large Medical Equipment peers. If you want to pressure test your own expectations against that framework, the narrative lays out every key assumption so you can decide how much of it you agree with.

Result: Fair Value of $596.36 (UNDERVALUED)

However, there are still pressure points to watch, including tighter hospital budgets in markets like Japan and Europe and rising competition in robotic instruments that could challenge high margin consumables.

Another View: Rich Multiple Sends a Different Signal

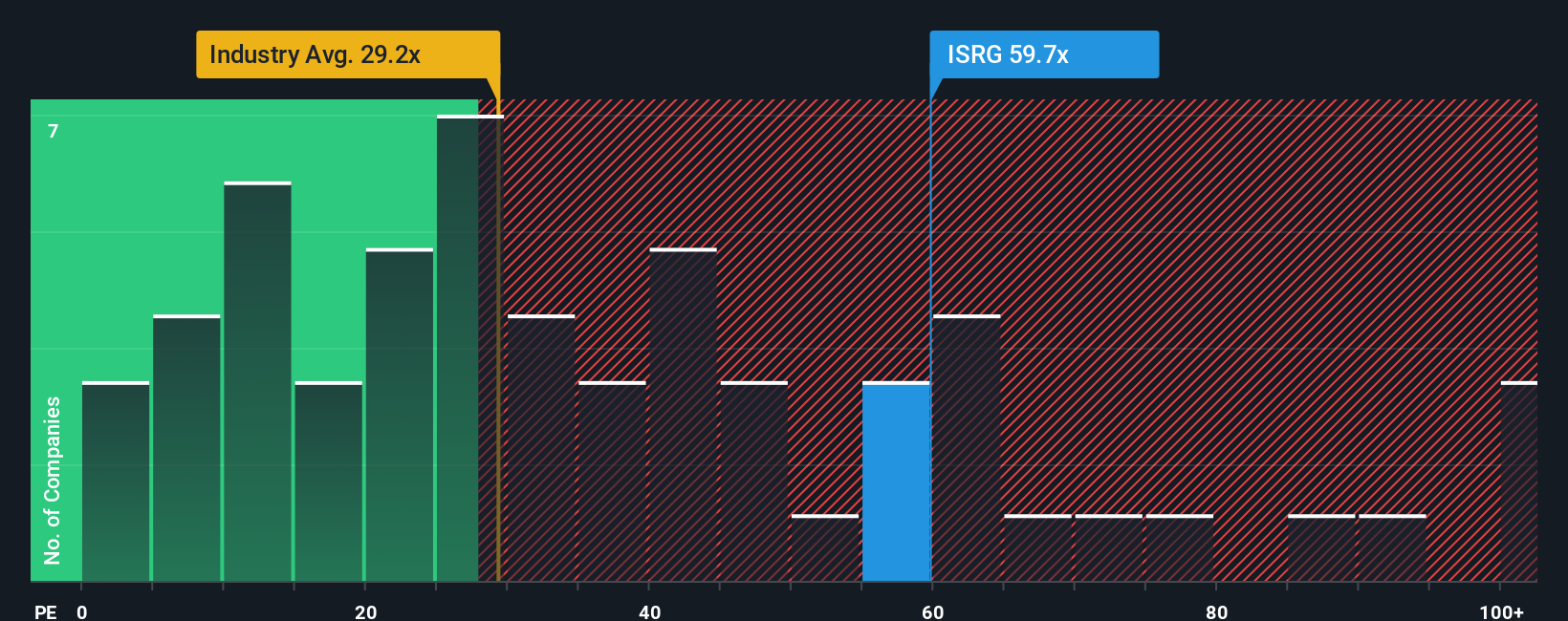

While the popular narrative points to an 18.5% upside to fair value, the current P/E of 60.4x tells a tougher story. It sits well above the US Medical Equipment industry at 30.4x and above Intuitive Surgical’s own fair ratio of 37.6x. This points to valuation risk if sentiment cools.

Build Your Own Intuitive Surgical Narrative

If you are not fully aligned with these views or prefer to weigh the data yourself, you can build a custom Intuitive Surgical story in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Intuitive Surgical.

Looking for more investment ideas?

If Intuitive Surgical is already on your radar, it makes sense to widen your search now so you do not miss other strong candidates worth researching.

- Target dependable income by reviewing 13 dividend fortresses that may appeal if you want yields backed by solid fundamentals.

- Hunt for potential value opportunities through 53 high quality undervalued stocks that line up with quality metrics and financial strength filters.

- Zero in on financial resilience with our solid balance sheet and fundamentals stocks screener (44 results) to focus on companies with balance sheets that can support their long term plans.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.