Assessing IRADIMED (IRMD) Valuation After Strong Multi Year Returns And High P/E Premium

IRadimed Corp. IRMD | 93.56 | +0.02% |

IRADIMED stock snapshot

IRADIMED (IRMD) has drawn attention after a long stretch of strong multi year total returns. The stock recently closed at US$99.81 and has shown mixed performance over the past month and past 3 months.

For context, the company reports annual revenue of US$83.814 million and net income of US$22.48 million. Its business is focused on MRI compatible medical devices for hospitals and imaging centers.

IRADIMED’s recent share price moves have been choppy, with a 15.82% 90 day share price return and an 83.59% 1 year total shareholder return. This points to momentum that has been strong over a longer stretch than in the latest month.

If IRADIMED’s run has you curious about where else capital is moving in healthcare technology, take a look at our screener of 25 healthcare AI stocks as a starting point for further research.

With IRADIMED posting strong multi year total returns while trading around US$99.81 against a US$120.00 analyst target, the key question is simple: are you looking at an undervalued growth story, or is the market already pricing in what comes next?

Most Popular Narrative: 1% Overvalued

IRADIMED’s most followed narrative sets a fair value of about $99 per share, sitting just below the recent $99.81 close, which keeps expectations tightly aligned.

The introduction and FDA approval of the new 3870 MRI-compatible IV pump, with significantly enhanced usability and technology over the legacy product, is expected to catalyze a major replacement cycle among hospitals and imaging centers, unlocking large-scale, recurring device and consumable revenues. This supports a step-change in revenue growth as existing customers upgrade and potential new customers previously deterred by usability issues are attracted.

Curious what kind of revenue path and margin profile need to sit behind that story to justify today’s price and beyond It all comes down to how quickly hospitals adopt the new pump, what happens to profitability as volumes build, and the future earnings multiple this narrative assumes will hold. The full narrative lays out those financial building blocks in detail.

Result: Fair Value of $99 (OVERVALUED)

However, this story can change quickly if hospitals slow pump upgrades due to budget pressure, or if supply chain hiccups stretch that 5 to 6 month backlog.

Another Take: High P/E Raises The Bar

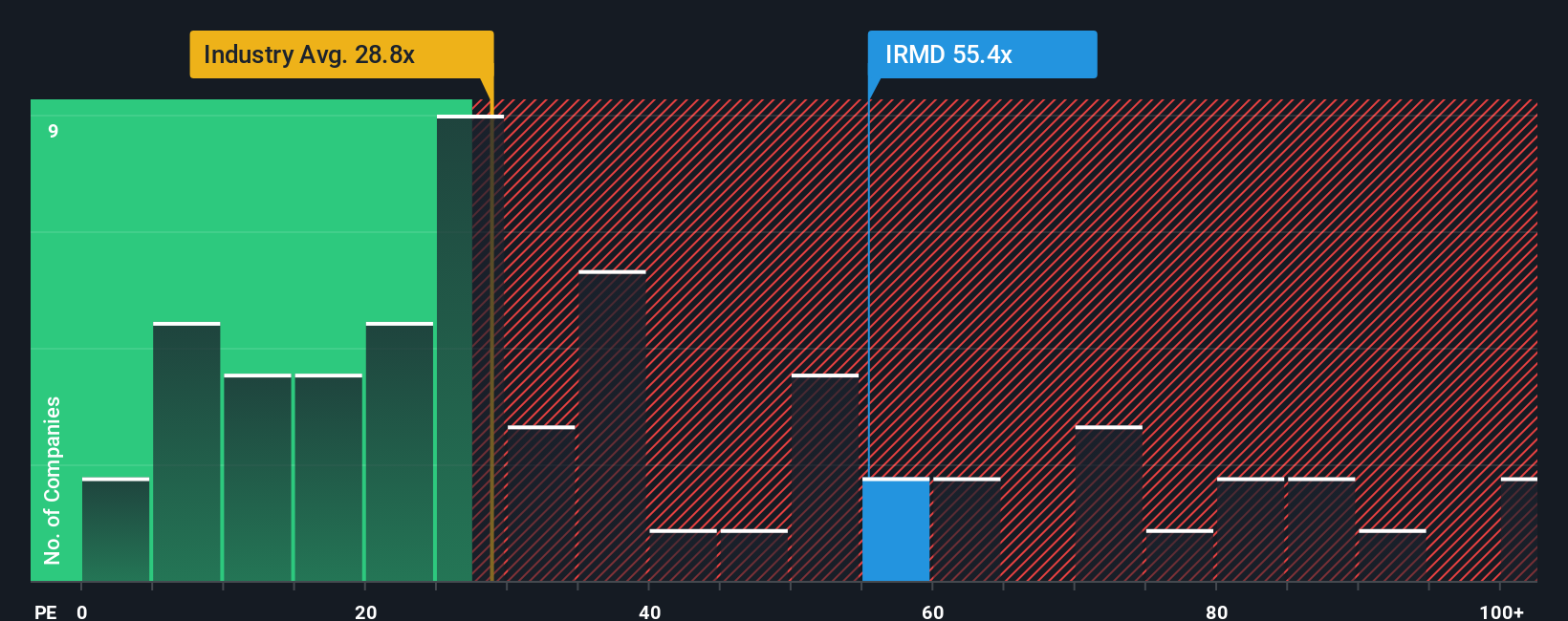

Our DCF view is not the only caution flag. On a simple P/E basis, IRADIMED trades at 56.5x, well above the US Medical Equipment industry on 30.4x and the 64x peer average, and far from its fair ratio of 19x. That gap leaves little room if growth or sentiment cools. How comfortable are you with that kind of valuation stretch?

Next Steps

If this mix of optimism and caution feels finely balanced, now is the time to look through the numbers yourself and pressure test the story. A good starting point is to weigh the company’s mix of risks and potential upside, highlighted in our breakdown of 2 key rewards and 1 important warning sign.

Ready to scout your next idea?

If IRADIMED is already on your watchlist, do not stop there. Broaden your opportunity set with a few focused screens that can surface fresh ideas fast.

- Target potential value opportunities by reviewing our list of 55 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience by checking companies in our 82 resilient stocks with low risk scores that score well on stability and balance sheet strength.

- Spot earlier stage opportunities by scanning our 29 elite penny stocks with strong financials that pass basic financial quality filters before many investors pay attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.