Assessing Jabil (JBL) Valuation After New Sivers Partnership Targets Greener AI Data Centers

Jabil Inc. JBL | 0.00 |

Jabil (JBL) recently drew attention after partnering with Sivers Semiconductors to develop a 1.6T linear receive optical transceiver, which is aimed at reducing energy use in next generation AI data centers.

The recent 1.6T optical transceiver partnership comes on top of strong momentum, with a 30 day share price return of 27.53% and a 90 day share price return of 40.81%, while the 1 year total shareholder return of 128.12% points to a very large gain over a longer period.

If you are interested in other companies tied to AI infrastructure and data center demand, this is a good moment to scan 37 AI infrastructure stocks

With Jabil now trading at US$342.47, showing strong recent returns and an 8% intrinsic discount estimate alongside a value score of 2, is this an overextended AI beneficiary or a genuine opportunity the market has not fully priced in yet?

Most Popular Narrative: 13.1% Overvalued

Jabil's most followed valuation narrative puts fair value at $302.78, below the last close of $342.47. This sets up a clear pricing debate for investors.

The analysts have a consensus price target of $302.78 for Jabil based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $354.0, and the most bearish reporting a price target of just $273.0.

Curious what earnings path and margin profile are needed to justify this valuation gap? The narrative leans on compound revenue growth, richer profitability and a premium future P/E multiple. The full story comes out when you see how those pieces fit together over time.

Result: Fair Value of $302.78 (OVERVALUED)

However, you also need to weigh softer demand in EV and renewable energy, as well as pressure in Connected Living, where revenue has fallen after divestitures and weaker consumer demand.

Another View: DCF Points to Upside

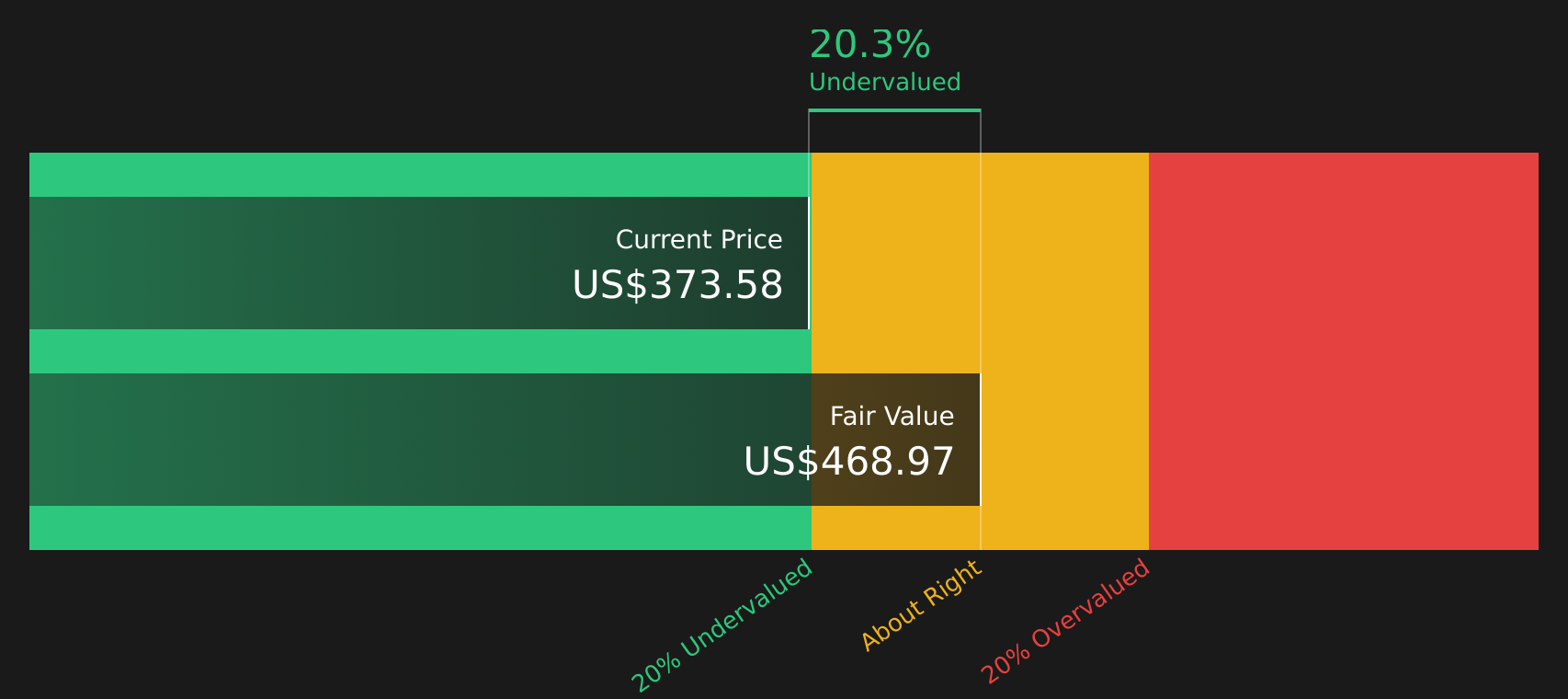

While the analyst narrative suggests Jabil is 13.1% overvalued using price targets, the SWS DCF model tells a different story. On that approach, fair value sits at $374.30 versus the current $342.47, implying Jabil trades at an 8.5% discount. Which set of assumptions appears more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Jabil for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing both risks and rewards in this story, it makes sense to move quickly, test the assumptions against the data, and then weigh 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Jabil has caught your attention, it is worth broadening your watchlist with other focused ideas that may suit different goals, risk levels, and income needs.

- Target potential mispriced opportunities by scanning 50 high quality undervalued stocks, which combines quality fundamentals with appealing pricing signals.

- Build a sturdier core to your portfolio by reviewing the solid balance sheet and fundamentals stocks screener (44 results) and focusing on companies with stronger financial footing.

- Strengthen your income stream by checking the 13 dividend fortresses, which focuses on higher yielding companies with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.