Assessing J.B. Hunt (JBHT) Valuation After Earnings Beat Dividend Hike And Faster Carrier Payments

J.B. Hunt Transport Services, Inc. JBHT | 226.03 | -1.56% |

J.B. Hunt Transport Services (JBHT) recently reported fourth quarter earnings per share of $1.90, along with a 2.3% dividend increase and a new payments partnership aimed at speeding up carrier payments.

The stock has been on a strong run, with a 90 day share price return of 31.76% and a 1 year total shareholder return of 35.08%, suggesting momentum has recently been building around its earnings, dividend increase, and new payments partnership, even after a 1 day share price decline of 1.30% to US$225.25.

If this kind of interest in logistics is on your radar, it could be a good moment to widen your search and check out 22 top founder-led companies as potential next ideas to research.

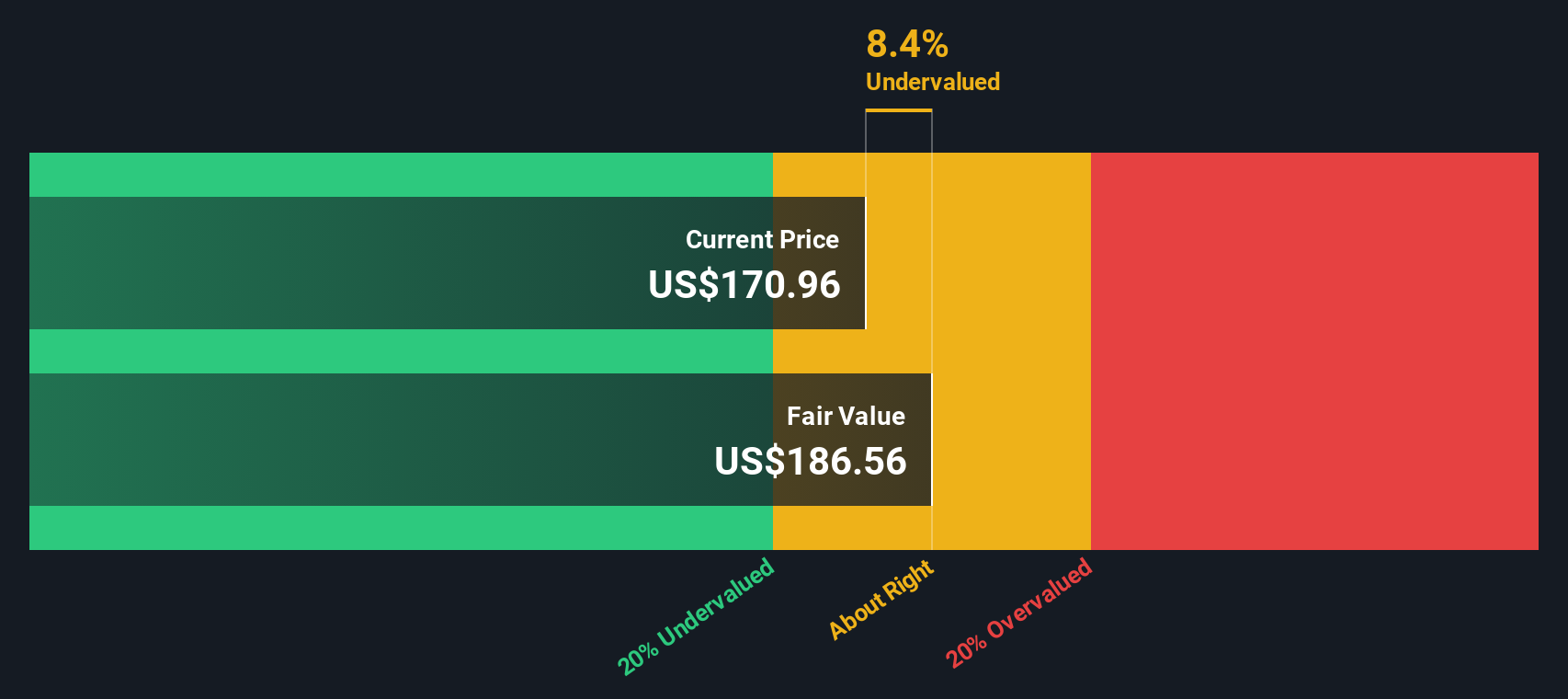

With the share price near its recent high and only a small implied discount to one intrinsic value estimate, the key question now is whether JBHT still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 7.1% Overvalued

At a last close of $225.25 against a widely followed fair value estimate of about $210.30, the current price sits slightly above that narrative anchor, which leans on steady earnings and cost discipline to justify its view.

The focus on reducing and optimizing costs, combined with a disciplined capital allocation strategy, suggests improvements in earnings as the company scales operations.

Strategic investments in technology and capacity expansion may provide a platform for long term revenue growth by better serving large addressable markets.

Want to understand why a modest growth profile still supports a premium setup here, including higher margins, rising earnings power and a richer future P/E multiple baked into that $210 fair value? The full narrative lays out the exact revenue path, profit step up and share count assumptions that make the numbers hold together.

Result: Fair Value of $210.30 (OVERVALUED)

However, you still need to weigh up softer freight demand and inflationary cost pressures, which could squeeze margins and challenge the earnings path behind that fair value.

Another View: Cash Flows Tell a Different Story

While the popular narrative pegs J.B. Hunt Transport Services at about 7.1% overvalued using earnings based assumptions, our DCF model points to a fair value of $226.63, a touch above the current $225.25 price. That tiny 0.6% gap raises a simple question for you: is this basically “fair enough” pricing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out J.B. Hunt Transport Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own J.B. Hunt Transport Services Narrative

If you are not fully aligned with these views or prefer to work from your own assumptions, you can quickly assemble your personal take on J.B. Hunt in just a few minutes, starting with Do it your way.

A great starting point for your J.B. Hunt Transport Services research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready to scout your next ideas?

If J.B. Hunt has caught your attention, do not stop here. Broadening your watchlist with other focused ideas can sharpen your overall approach.

- Target dependable income by checking out 15 dividend fortresses that might suit an investor who wants yield backed by solid business profiles.

- Hunt for quality at sensible prices through screener containing 25 high quality undiscovered gems that may not yet be crowded with attention.

- Prioritise resilience first and look at 81 resilient stocks with low risk scores if you want companies where risk indicators already look relatively contained.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.