Assessing JetBlue Airways (JBLU) Valuation After Mixed Price Momentum And Conflicting Fair Value Signals

JetBlue Airways Corporation JBLU | 0.00 |

What recent price moves suggest for JetBlue Airways (JBLU)

With JetBlue Airways (JBLU) shares up about 21% over the past month, but down roughly 6% over the past 3 months, investors may be reassessing what current pricing implies.

That recent 21% 30 day share price return, alongside a 10.68% year to date share price gain but a 74.63% five year total shareholder return loss, suggests short term momentum is building while longer term investors have faced considerable pressure.

If JetBlue’s swings have you thinking more broadly about the market, it can be useful to compare with other themes and sectors using tools designed for idea generation such as the 19 top founder-led companies

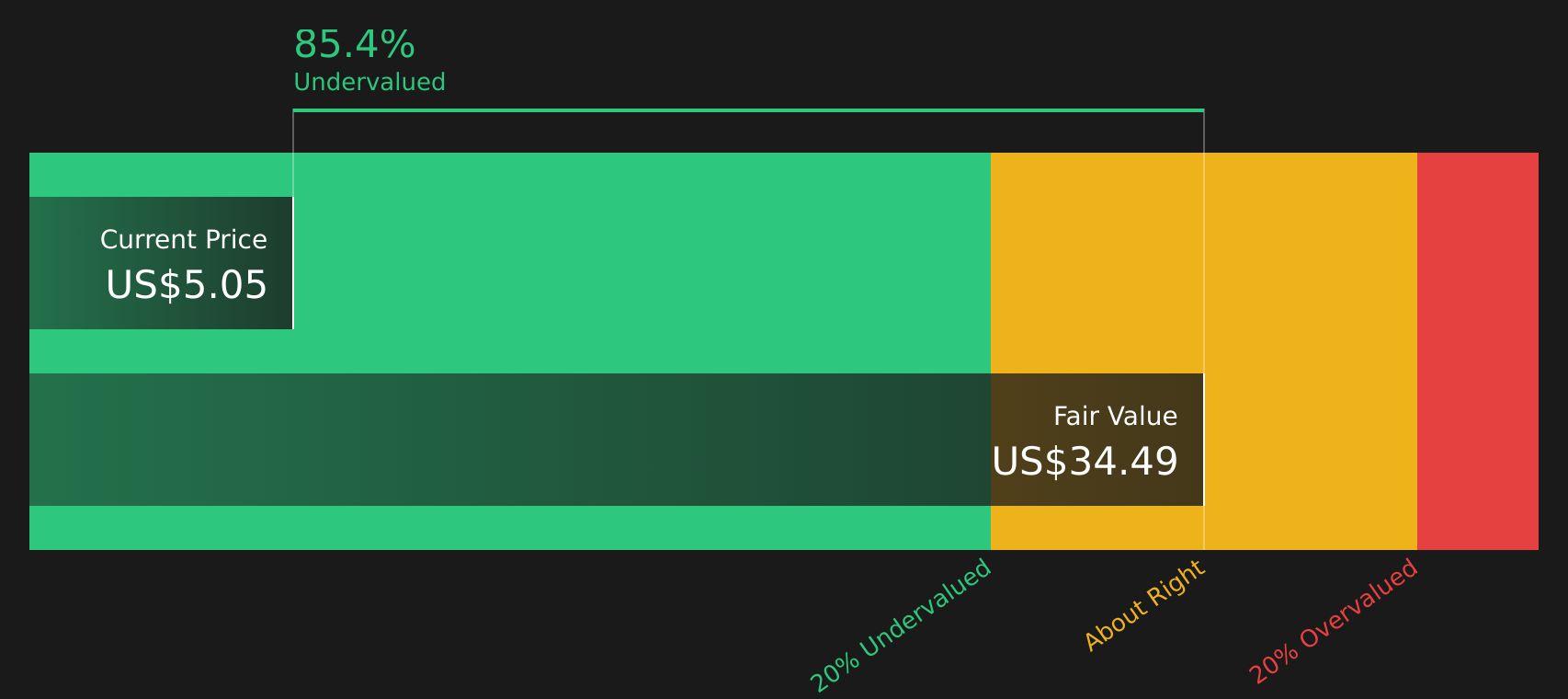

JetBlue’s recent 30% one-year total return, ongoing net loss of US$602 million and an estimated 48% gap to one intrinsic value estimate give mixed signals, raising the question: is this a fresh entry point, or has the market already priced in future recovery?

Most Popular Narrative: 5.2% Overvalued

JetBlue’s last close at $5.08 sits slightly above the narrative fair value of $4.83, pointing to a modest valuation premium built on specific earnings and margin assumptions.

The rebound in leisure travel and resilient demand, especially among Millennials and Gen Z prioritizing experiences, continues to drive close-in bookings and support premium cabin and loyalty revenue growth, which is likely to result in higher ticket revenues and topline expansion.

Curious what earnings path and margin repair story could support a higher valuation multiple than the wider US Airlines group? The full narrative spells out the revenue glide path, margin rebuild and earnings profile that sit behind this fair value call without leaving you to guess the core assumptions.

Result: Fair Value of $4.83 (OVERVALUED)

However, that story can quickly change if rising labor and fuel costs squeeze margins further, or if competitive pressure keeps load factors and unit revenues under strain.

Another View: Cash Flows Point To A Different Story

While the most popular narrative has JetBlue as about 5.2% overvalued at a fair value of $4.83, our DCF model presents a different perspective, with a future cash flow value of $9.69 per share that suggests the current $5.08 price is at a steep discount. Which set of assumptions do you think feels more realistic?

Next Steps

Mixed messages on value and risk so far? If you want a clearer picture, move quickly to weigh the upside and downside across the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If JetBlue has you thinking harder about risk, reward, and price, do not stop here, use targeted stock lists to pressure test your next move across sectors.

- Target higher potential returns in smaller companies and scan 26 elite penny stocks with strong financials that already show stronger financial underpinnings instead of just hype.

- Zero in on quality at a price that could work for you by checking 61 high quality undervalued stocks built around balance sheets and cash flows.

- Prioritise staying power and capital protection by reviewing 73 resilient stocks with low risk scores that score well on resilience and risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.