Assessing Kosmos Energy (KOS) Valuation After 2026 Growth Plan And Ghana License Extensions

Kosmos Energy Ltd. KOS | 2.92 | +8.55% |

Kosmos Energy (KOS) is back in focus after issuing 2026 guidance that targets a 15% production increase, a 20% cut in operating costs, and lower net debt, even as recent results showed sizeable losses.

The share price has reacted strongly to this guidance and the recent Ghana license extensions. It has delivered a 30 day share price return of 83.33% and a year to date share price return of 183.38%, even though the 3 year total shareholder return is a loss of 64.47%.

If this kind of turnaround story has your attention, it could be a good moment to see what else is moving in energy and resources, starting with 28 elite gold producer stocks.

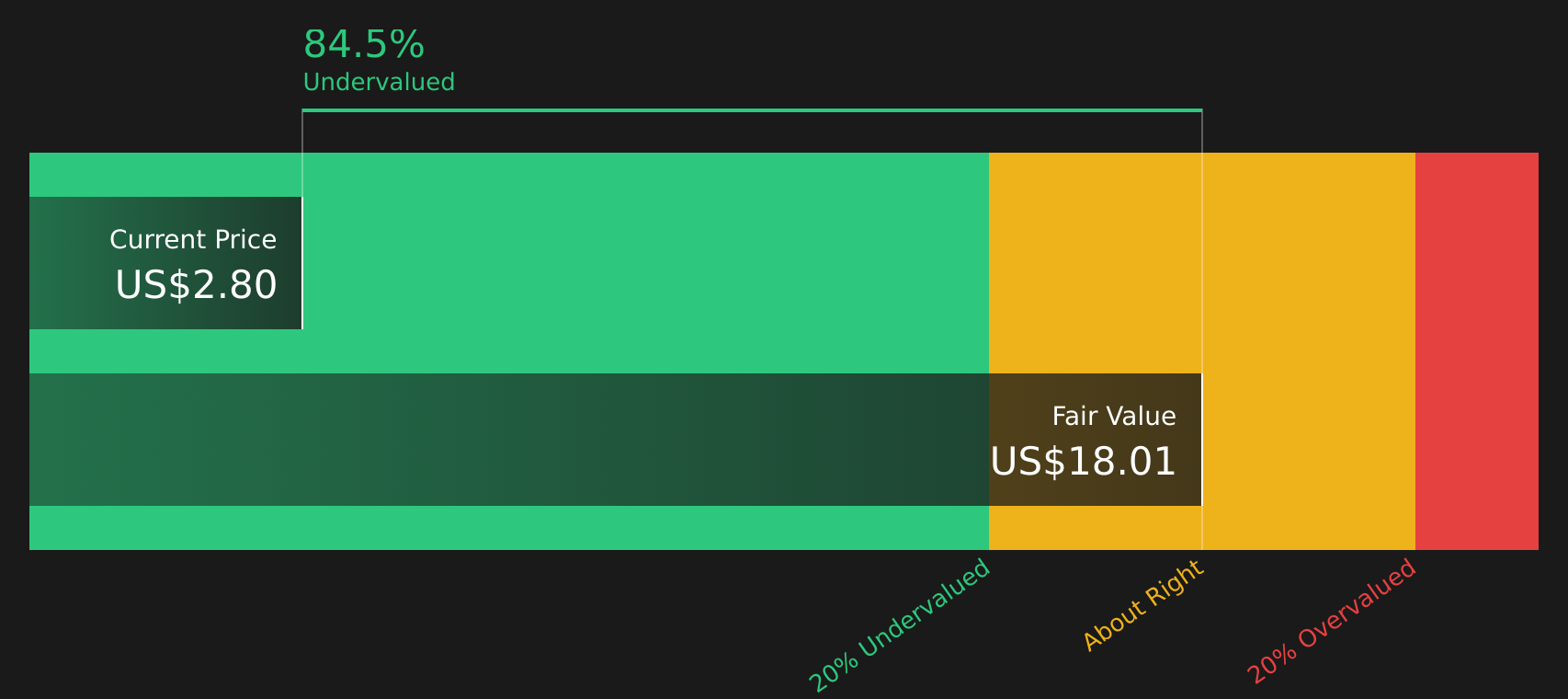

With the shares now at $2.53 and trading above the average analyst price target, recent losses and ambitious 2026 goals are pulling in opposite directions. Is there genuine value left here, or has the market already priced in the recovery story?

Most Popular Narrative: 12.8% Overvalued

The most followed narrative puts Kosmos Energy's fair value at $2.24 per share, which sits below the recent $2.53 close and creates an immediate tension between modeled value and market price.

Analysts have raised their price target for Kosmos Energy to $2.24 from $2.10, reflecting updated assumptions on fair value, a lower discount rate, and revised expectations for revenue growth, profit margins, and future P/E levels.

Want to know what is sitting behind that fair value lift? The narrative leans on a different growth glide path for revenue, margins and future earnings power than you might expect from a company that is still loss making today. The key is how those cash flows are stepped out over time and then pulled back using a discount rate that has already been nudged lower.

Result: Fair Value of $2.24 (OVERVALUED)

However, the heavy asset impairment and reliance on politically sensitive regions mean that project setbacks or fiscal surprises could still upend the current recovery narrative.

Another View: Market Pricing Versus Cash Flow

So far you have seen a fair value of $2.24 per share from the narrative model, which suggests Kosmos Energy is 12.8% overvalued at the current $2.53 price. Our SWS DCF model lands in a very different place, with a fair value of $2.98, implying the shares trade about 15.1% below that estimate.

That split between an overvalued narrative and an undervalued cash flow model leaves you with a simple question: which set of assumptions do you trust more, the story built into analyst targets or the cash flows embedded in our model?

Next Steps

Mixed signals like these often split opinions. If you think this story is moving fast, now is the time to check the full picture and weigh 2 key rewards and 3 important warning signs against your own view.

Ready to hunt for your next idea?

If Kosmos has sparked your interest, do not stop here; use this momentum to scan other opportunities that might fit even better with your goals.

- Target potential value opportunities by checking companies highlighted in our 47 high quality undervalued stocks and see which ones line up with your return expectations.

- Secure more dependable income by reviewing 14 dividend fortresses, focused on businesses offering 5%+ yields with an emphasis on durability.

- Prioritize resilience by scanning 73 resilient stocks with low risk scores and see which names match your comfort level on volatility and risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.