Assessing L3Harris Technologies (LHX) Valuation After Strong Recent Share Price Momentum

L3Harris Technologies Inc LHX | 0.00 |

Event driven context for L3Harris Technologies (LHX)

L3Harris Technologies (LHX) has been drawing attention after recent share price moves, including a 13% return over the past month and 19% over the past 3 months, prompting investors to reassess its current valuation.

While the recent 1 month share price return of 12.6% and 3 month share price return of 18.8% point to building momentum, the 1 year total shareholder return of 64.8% and 5 year total shareholder return of 107.6% show that the stock has also rewarded longer term holders.

If L3Harris has put defense contractors on your radar, it could be a good moment to scan aerospace and defense stocks for other ideas in the space.

With L3Harris shares around $342.85 and metrics like value score, intrinsic value estimates and analyst targets in focus, the key question now is simple: is there still an opportunity here or is the market already pricing in potential future developments?

Most Popular Narrative: 5.8% Undervalued

With L3Harris shares at $342.85 and the most followed narrative pointing to a fair value of $364, the gap raises questions about what is baked into those assumptions.

The U.S. defense budget is expected to grow, with new defense initiatives and a potential increase in funding that could benefit L3Harris, supporting revenue growth. L3Harris is well-positioned in several key growth areas, such as missile warning and tracking, due to recent investments and capability alignment, likely increasing future revenue.

Curious what revenue path, margin uplift and future earnings multiple are needed to justify that higher fair value, especially with a discount rate under 8% guiding the model and an earnings profile that leans on both defense spending and the missile spinout story? The full narrative lays out those building blocks in detail, including how future profits and valuation assumptions interact over time.

Result: Fair Value of $364 (UNDERVALUED)

However, those assumptions can be tested if fixed price contracts squeeze margins, or if U.S. and European political tensions weigh on international communications demand.

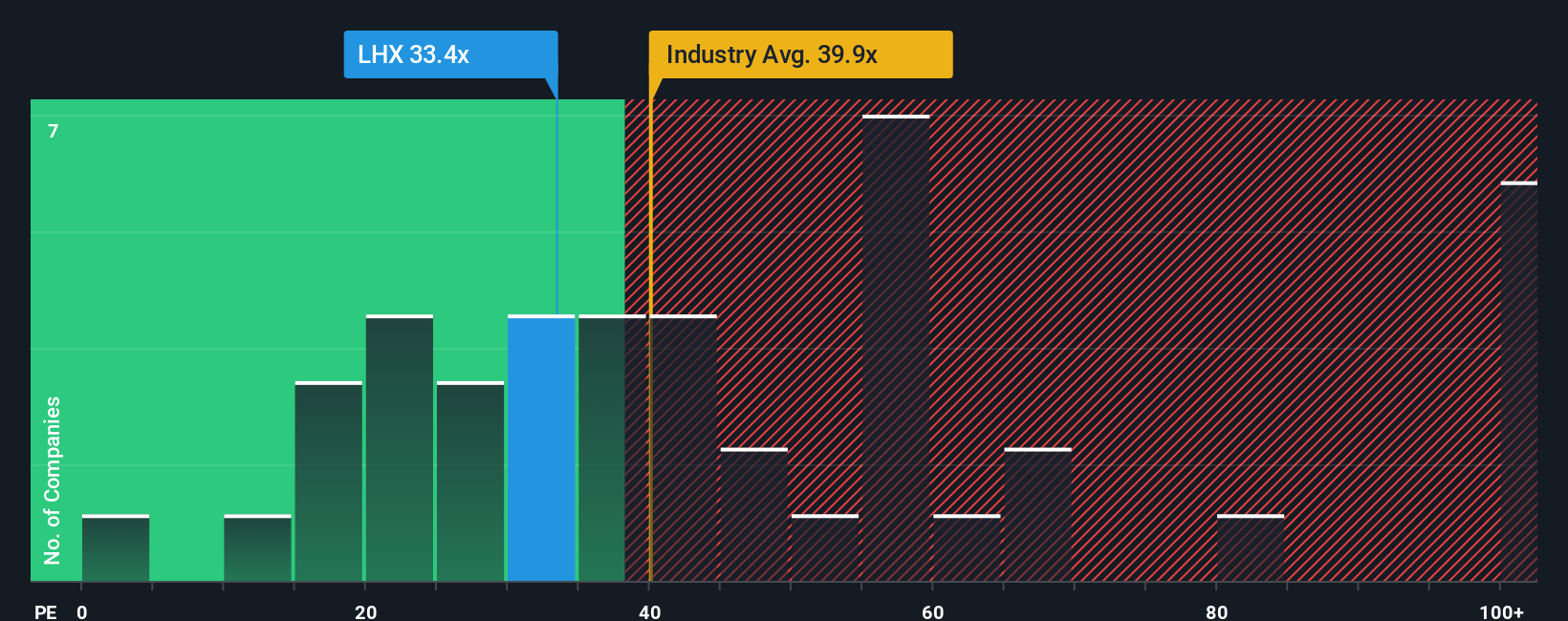

Another View: What The P/E Ratio Is Saying

While our model points to L3Harris trading about 5.7% below an estimated fair value of $363.46, the current P/E of 39.9x paints a different picture. That is higher than both the 36.7x peer average and the 33.7x fair ratio our work suggests the market could move toward over time.

In practice, that means a lot of optimism is already embedded in the share price. Outcomes that fall short of expectations could therefore matter more for investors than they might in a cheaper name. The question is whether you think L3Harris can keep justifying this richer multiple.

Build Your Own L3Harris Technologies Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way.

A great starting point for your L3Harris Technologies research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If L3Harris has sharpened your interest in defense and related themes, do not stop here. Use the screener to quickly surface other focused opportunities.

- Target potential value by reviewing these 875 undervalued stocks based on cash flows, where cash flow based filters highlight companies that may offer pricing that lines up more tightly with fundamentals.

- Explore technology themes by scanning these 24 AI penny stocks for businesses tied to artificial intelligence that might align with the themes on your watchlist.

- Strengthen your income focus by checking these 12 dividend stocks with yields > 3% for companies that currently offer dividend yields above 3% and that may complement your return objectives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.