Assessing La-Z-Boy (LZB) Valuation After Recent Share Price Momentum And Mixed Long Term Returns

La-Z-Boy Incorporated LZB | 31.60 | -0.91% |

La-Z-Boy (LZB) has been drawing attention after recent share price moves, with the stock closing at $39.58 and showing mixed returns over the past year, month, and past three months.

The recent 1-day share price return of 1.44% and 7-day share price return of 6.11% come on top of a 23.19% 90-day share price return. At the same time, the 1-year total shareholder return is 6.79% lower and the 3-year total shareholder return is 58.90% higher. This suggests that near term momentum has picked up while the longer term record remains mixed.

If La-Z-Boy’s recent move has you thinking about what else is working in consumer names, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With La-Z-Boy trading at $39.58, alongside an estimated intrinsic discount of around 30% and only a small gap to the average analyst price target, the key question is whether this represents a genuine value opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 3.5% Undervalued

Using a fair value of US$41 against the last close at US$39.58, the most followed narrative sees a modest gap in La-Z-Boy’s pricing and builds a detailed case around future earnings and margins.

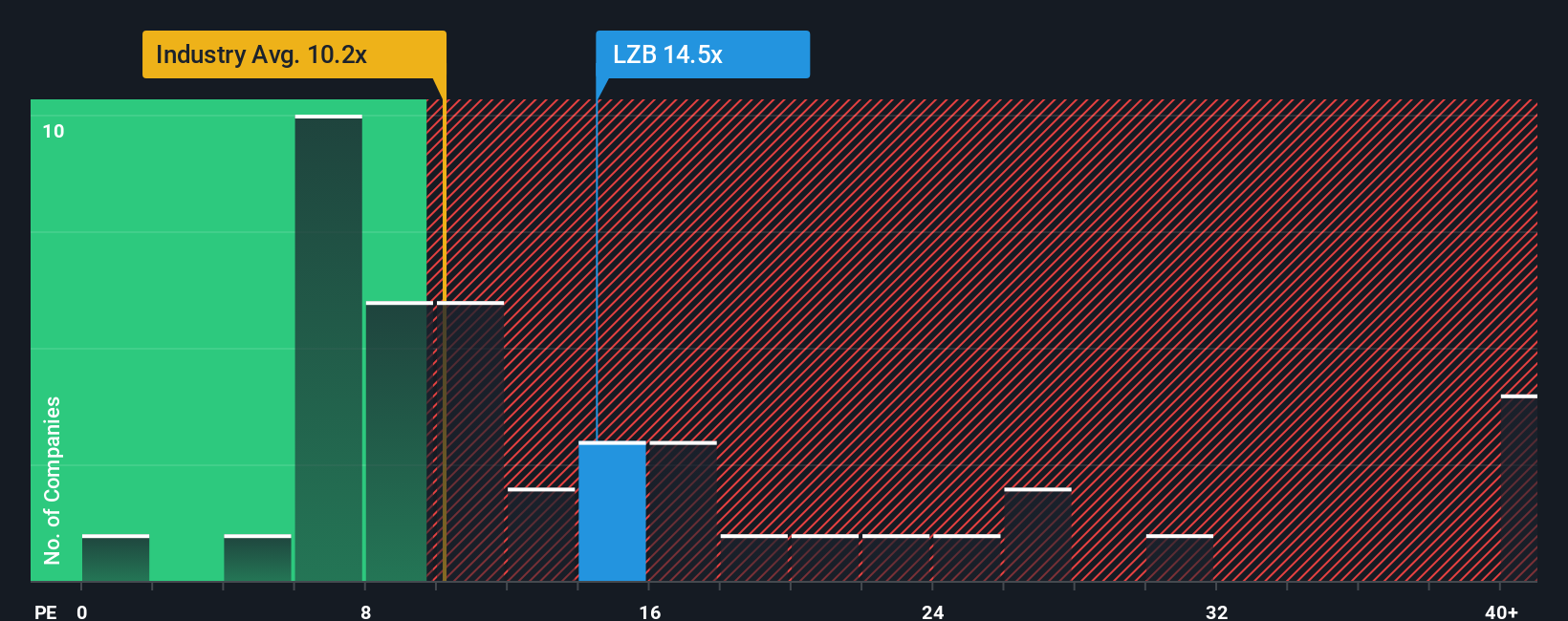

In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.5x on those 2028 earnings, up from 15.9x today. This future PE is greater than the current PE for the US Consumer Durables industry at 11.5x.

Want to see what is behind that richer earnings multiple and higher profit base, plus how steady revenue growth feeds into the valuation story? The key assumptions are more specific than you might expect, and they rest on a mix of margin rebuilding and measured top line expansion. Curious how those threads are combined into today’s fair value?

Result: Fair Value of $41 (UNDERVALUED)

However, that fair value story can be challenged if softer store traffic persists, or if heavier discounting in key product lines keeps squeezing margins and cash flow.

Another View: What P/E Is Telling You

While our fair value estimate points to La-Z-Boy as undervalued overall, the P/E picture is less forgiving. At 18.1x earnings, the shares sit well above the estimated fair ratio of 14.9x and ahead of both the Consumer Durables industry at 11.7x and peer average at 11.8x.

That gap means you are paying a richer price than the sector and similar companies, which could limit upside if expectations cool or earnings fall short. The key question is whether you see enough quality and earnings growth ahead to justify paying above that fair ratio.

Build Your Own La-Z-Boy Narrative

If you look at the numbers and come to a different conclusion, or just prefer to test the inputs yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your La-Z-Boy research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about tightening up your watchlist, now is the moment to scan for fresh ideas before the next round of opportunities passes you by.

- Spot potential value candidates early by running your own search through these 882 undervalued stocks based on cash flows, built around discounted cash flow and pricing signals.

- Position yourself in the next wave of technology by checking out these 28 AI penny stocks, which are tied to real revenue and business models, not just headlines.

- Target higher income potential upfront by screening for these 12 dividend stocks with yields > 3%, which already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.