Assessing Legence (LGN) Valuation After A Sharp 3 Month Share Price Surge

Legence Corp. Class A LGN | 0.00 |

Why Legence Stock Is on Investors’ Radar

Legence (LGN) has drawn fresh attention after a strong recent share performance, with the stock up 53% over the past month and more than doubling over the past 3 months.

The recent 52.95% 1-month share price return and 107.64% 3-month share price return suggest strong momentum building on earlier gains, even though the 7-day share price return of 2.22% is slightly weaker.

If this kind of move has you looking for other potential opportunities, it could be a good moment to scan the market using our screener for 37 power grid technology and infrastructure stocks

With Legence now at US$100 and trading above both its analyst price target and intrinsic value estimate, investors have to ask: is this surge overdone, or is the market correctly factoring in stronger growth ahead?

Price-to-Sales of 3x: Is It Justified?

With a P/S of 3x, Legence trades above the US Construction industry average of 1.9x but below the peer average of 4.3x and an estimated fair P/S of 4.1x.

The P/S multiple compares the company’s market value to its revenue, which can be useful for loss-making businesses where earnings are not yet a reliable guide. For Legence, forecast revenue growth of 18.9% a year and expectations that earnings could grow 49.61% a year and move into profitability within 3 years help explain why the market may be willing to pay a higher P/S than the sector average.

Compared with the Construction industry, Legence’s higher 3x P/S suggests investors are pricing in stronger growth and a faster path to profitability than the broader group. At the same time, trading below the 4.1x fair P/S estimate and the 4.3x peer average implies the market is still applying a discount to what the regression based fair ratio suggests the multiple could move toward if those forecasts play out.

Result: Price-to-Sales of 3x (ABOUT RIGHT)

However, the stock trading above its US$78.78 analyst price target and the company still reporting a loss of US$33.80m could challenge this positive momentum.

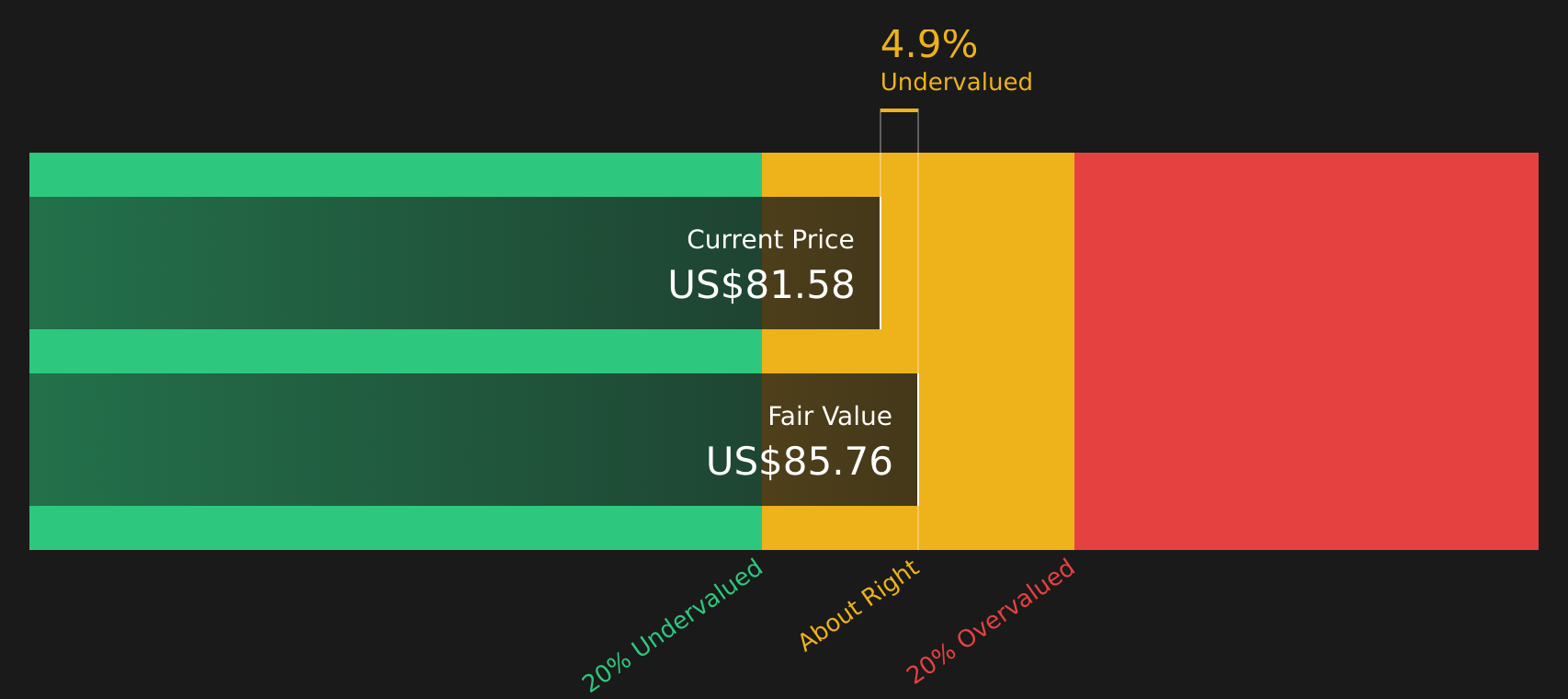

Another View: DCF Points to a Richer Price

While the current 3x P/S ratio looks reasonable against the fair ratio of 4.1x, the SWS DCF model tells a different story. With the stock at $100 and the model indicating a future cash flow value of $89.74, Legence screens as overvalued on this method. That gap raises a simple question: is the market getting ahead of itself, or is the model too cautious?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Legence for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With the mixed signals in this article, it makes sense to look through the numbers yourself and decide how compelling the story really feels. To understand what investors are optimistic about, take a closer look at the 2 key rewards

Looking for more investment ideas?

If you are serious about putting your capital to work, do not stop at one stock. Use targeted stock ideas to spot opportunities others might overlook.

- Target value opportunities that combine quality with attractive pricing by checking out 47 high quality undervalued stocks.

- Prioritise resilience and sleep easier at night by reviewing companies in the 68 resilient stocks with low risk scores.

- Spot potential future standouts before they are widely followed by scanning the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.