Assessing Lemonade (LMND) Valuation As AI Growth Optimism Builds Ahead Of Earnings

Lemonade LMND | 65.17 | +4.32% |

Recent commentary around Lemonade (LMND) has focused on upbeat projections for premiums, revenue and customer growth, as the insurer leans on AI driven expansion ahead of an earnings report that is drawing investor attention.

The upbeat expectations around premiums and customer growth are playing out against a mixed price backdrop. A recent 2.91% 1 day share price gain to $63.76 follows a 30 day share price return of negative 19.71% and a much stronger 1 year total shareholder return of 65.65%, which hints at longer term optimism but fading short term momentum.

If Lemonade’s AI fueled insurance push has your attention, you might also want to see what else is happening in the space by checking out 58 profitable AI stocks that aren't just burning cash as another set of ideas to review.

With Lemonade still loss making but showing revenue growth of 25.96% and a 1 year total return of 65.65%, investors may be considering whether the recent pullback represents a fresh entry point or whether the stock is already pricing in future growth.

Most Popular Narrative: 17.3% Undervalued

According to the most followed narrative, Lemonade’s fair value sits at $77.14 per share versus the last close at $63.76, which points to a valuation gap that some investors are watching closely.

Lemonade reported in-force premiums of $889 million, up 24% year over year and higher by nearly 50% since mid-2022. The company now has 2.31 million customers, up 17% from year-ago levels, and gross profit climbed 71%.

The narrative, according to VincentE, focuses on compounding premium growth, improving unit economics and a future profit margin that assumes a meaningful shift in the business model. Readers may be interested in which revenue trajectory and margin profile sit behind that $77.14 figure, and how a future earnings multiple is used in that framework.

Result: Fair Value of $77.14 (UNDERVALUED)

However, there are still clear risks, including sustained losses, with net income at a loss of US$173.8 million, and any slowdown in customer or premium growth.

Another View on Valuation

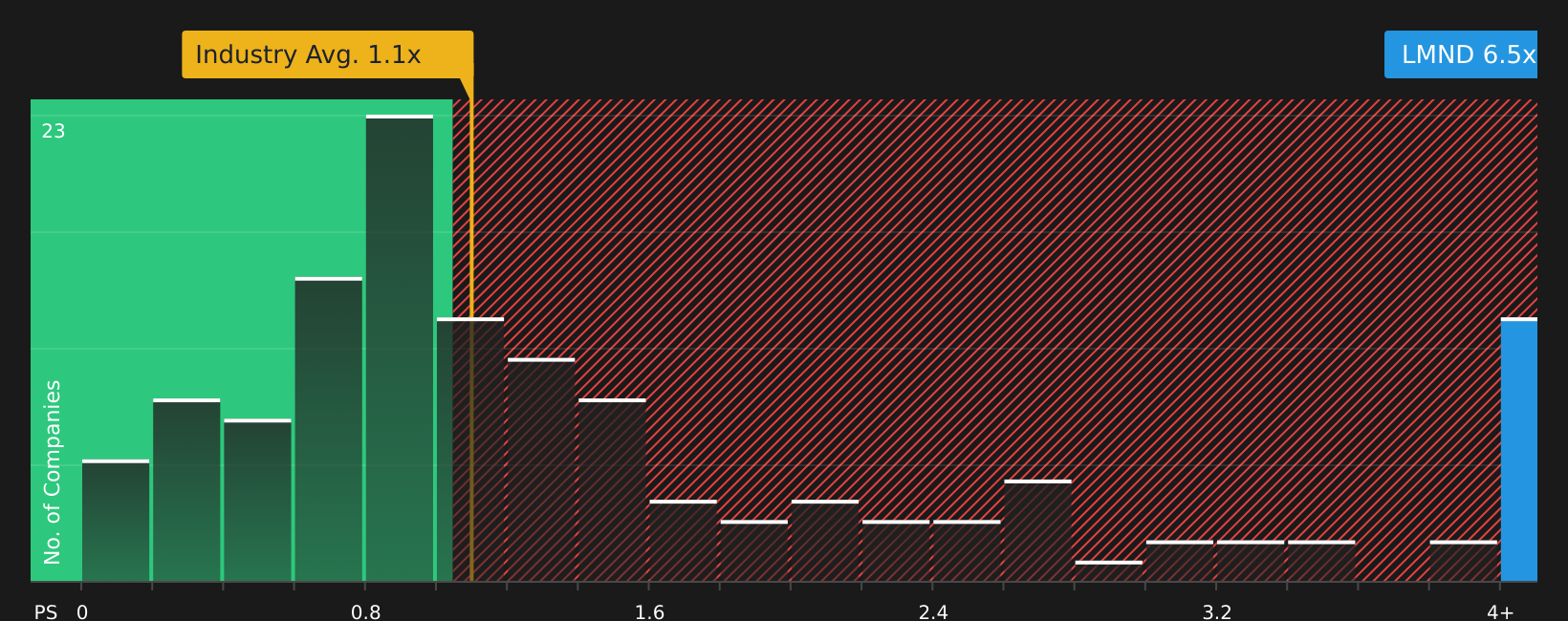

That $77.14 fair value hinges on long term growth, but the current P/S of 7.2x tells a different story. It sits well above the US insurance industry at 1.1x, the peer average at 2x, and even the 1.4x fair ratio. This points to meaningful valuation risk if sentiment cools.

Next Steps

If this mix of optimism and concern around Lemonade feels finely balanced, take a moment to review the numbers yourself and move quickly to shape your own view, starting with 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If you are weighing Lemonade but do not want all your eggs in one basket, it makes sense to line up a few other ideas side by side.

- Scan for quality at a discount by reviewing 55 high quality undervalued stocks, and see which companies pair solid fundamentals with prices that may not fully reflect them yet.

- Strengthen your income stream by checking 13 dividend fortresses, focusing on companies with higher yields that some investors use when they want cash returns from their holdings.

- Reduce portfolio stress by considering 81 resilient stocks with low risk scores, where the focus is on companies with lower risk scores that some investors prefer when they want fewer surprises.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.