Assessing Linde (LIN) Valuation After Strong Q4 Beat Backlog Growth And M&A Push

Linde plc LIN | 497.94 | -0.34% |

What Linde’s Acquisition Push Means for Investors Now

The latest catalyst for Linde (LIN) is not a single deal, but management’s clear message that acquisitions remain central to its playbook, coming alongside detailed fourth quarter 2025 results.

On the earnings call, CEO Sanjiv Lamba highlighted what he described as a robust pipeline of tuck in M&A focused on adding to Linde’s existing supply density rather than pushing into new areas. That framing matters if you are looking at how future deals might fit with the current industrial gas network and existing projects.

Linde’s shares have eased back in the very short term, with a 1 day share price return of a 2.49% decline and a 7 day share price return of a 1.91% decline. However, the 90 day share price return of 6.55% and 5 year total shareholder return of 90.08% suggest longer term momentum has been strong, even if the 1 year total shareholder return of a 0.17% decline looks more muted.

If the recent M&A push has you thinking more broadly about where industrial growth could come from next, it might be worth scanning our list of 24 power grid technology and infrastructure stocks to see which other companies are tied into major infrastructure themes.

With Linde trading around US$448 after a strong multi year run, recent earnings, active M&A plans and a modest analyst price target gap all matter. Is there still an entry point here, or is future growth already priced in?

Most Popular Narrative: 11% Undervalued

The most followed narrative pegs Linde’s fair value at about $503 per share, comfortably above the last close of $448.24, and builds that view around long term project economics, earnings power and capital allocation.

Linde's project backlog has doubled over the last 4 years, anchored by long-term, fixed-fee contracts supporting U.S. clean energy and electronics infrastructure, and management expects this robust pipeline to remain at record levels, positioning the company for steady multi-year revenue and earnings growth.

Want to see what is baked into that backlog story? The narrative hinges on measured revenue growth, rising margins and a premium earnings multiple. Curious how those ingredients add up to that fair value call? The full narrative spells out the assumptions line by line.

Result: Fair Value of $503.52 (UNDERVALUED)

However, that fair value story could crack if industrial demand in Europe stays weak, or if clean energy projects are delayed and the backlog takes longer to convert.

Another Take: Valuation Gaps On Earnings

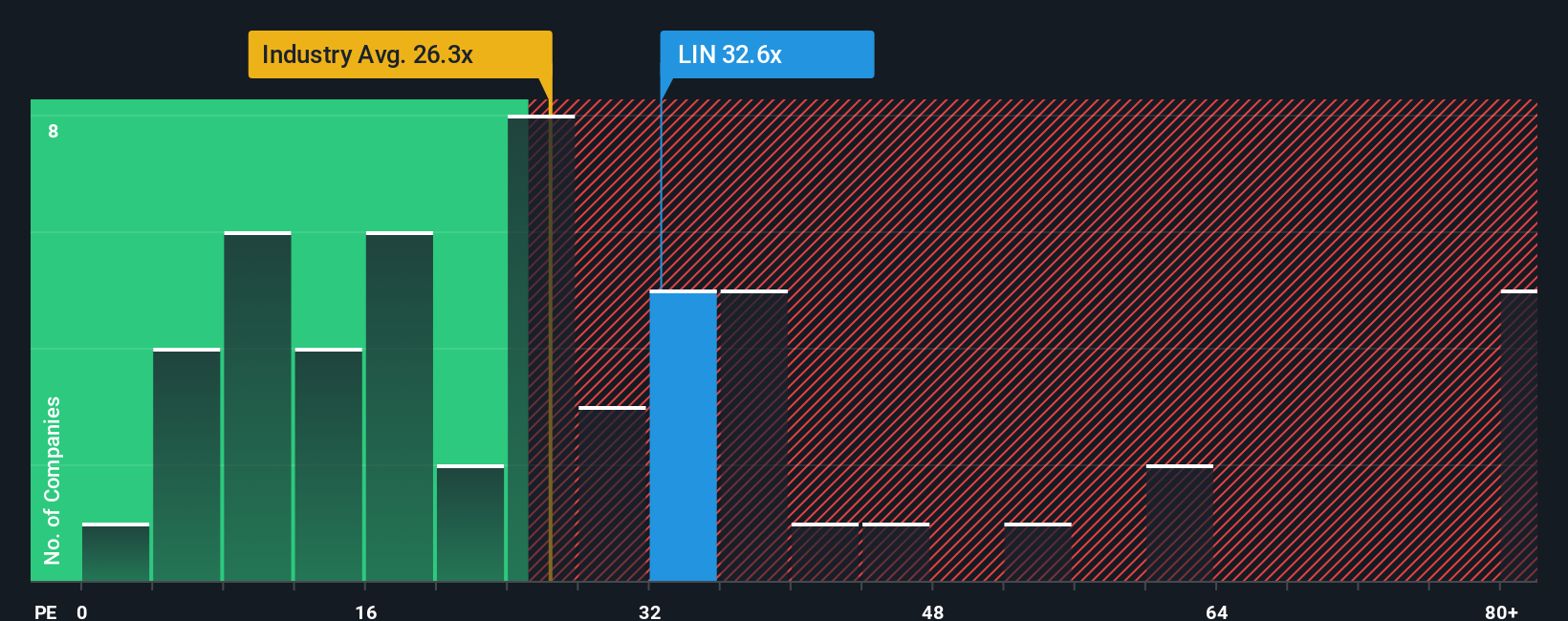

Our first narrative leans on fair value around $503 per share, but the earnings multiples tell a more cautious story. Linde trades on a P/E of 30.3x, above the US Chemicals industry at 25.4x and above its own fair ratio of 28.7x. This points to some valuation risk if sentiment cools.

Build Your Own Linde Narrative

If you look at these numbers and come to a different conclusion, or simply prefer to run your own checks, you can build a fresh view in just a few minutes starting with Do it your way

A great starting point for your Linde research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Linde has sharpened your appetite for quality research, do not stop here. The right mix of ideas can make a real difference over time.

- Target value with confidence by scanning our list of 52 high quality undervalued stocks that pair stronger fundamentals with prices that may not fully reflect their metrics.

- Prioritize resilience by reviewing the 82 resilient stocks with low risk scores that score well on our risk checks if you prefer a steadier ride.

- Get ahead of the crowd by filtering for our screener containing 24 high quality undiscovered gems before they sit firmly on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.