Assessing Lockheed Martin (LMT) Valuation After Strong Recent Share Price Momentum

Lockheed Martin Corporation LMT | 622.79 | +0.83% |

Lockheed Martin stock snapshot after recent performance

Lockheed Martin (LMT) has drawn investor attention after a recent run that includes a 21.50% move over the past month and an 18.25% gain over the past 3 months, alongside steady profitability figures.

That strong 30 day share price return of 21.50% and 18.25% over 90 days comes on top of a 15.89% year to date share price gain and a 5 year total shareholder return of 99.85%. Together, these figures point to solid momentum supported by longer term compounding.

If Lockheed Martin has you looking closer at defense contractors, this is also a useful moment to scan other aerospace and defense stocks that might fit your portfolio goals.

With the stock up strongly over multiple time frames, trading around $576.06 and only a small discount to one intrinsic estimate, the key question now is whether there is still a buying opportunity here or if markets are already pricing in future growth.

Most Popular Narrative: 9.1% Overvalued

Against a last close of $576.06, the most followed narrative pegs Lockheed Martin’s fair value at about $528, suggesting the recent share price runs ahead of that estimate.

The analysts have a consensus price target of $476.667 for Lockheed Martin based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $544.0, and the most bearish reporting a price target of just $398.0.

Curious how relatively modest revenue growth, a higher profit margin profile and a lower future P/E can still support this valuation gap? The full narrative lays out the earnings path, cash flow assumptions and discount rate choice that have to hold together for that fair value to make sense.

Result: Fair Value of $528 (OVERVALUED)

However, that story can change quickly if issues with fixed price contracts deepen or if U.S. and allied defense budgets shift away from key Lockheed Martin programs.

Another View: Multiples Point To A Different Story

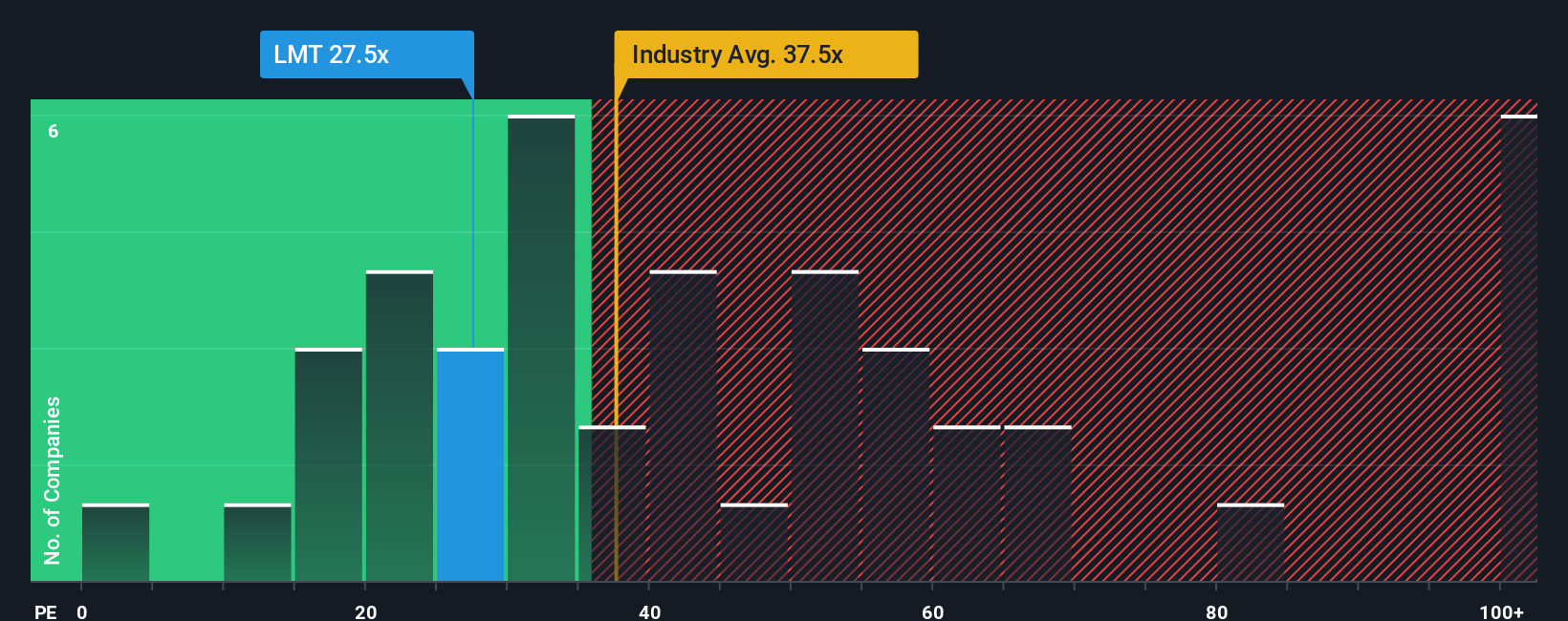

While the most popular narrative sees Lockheed Martin as about 9.1% overvalued against a fair value of roughly $528, the market’s own pricing signals are less one sided. At a P/E of 31.7x, the shares sit below peers at 37.8x and below an estimated fair ratio of 35.8x. This suggests investors are not paying a premium for this stock right now and may even be applying a safety cushion. The real question is whether that cushion reflects genuine risk or a potential opening for patient investors.

Build Your Own Lockheed Martin Narrative

If you see the numbers differently or simply prefer to weigh the data yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your Lockheed Martin research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Lockheed Martin has sharpened your focus, do not stop here. Widen your watchlist now so you are not the one hearing about the opportunities after they move.

- Scan for value focused setups by checking out these 872 undervalued stocks based on cash flows that align with cash flow based opportunities.

- Spot early trends in technology by tracking these 24 AI penny stocks that are shaping how automation and data are used across sectors.

- Strengthen your income angle by reviewing these 13 dividend stocks with yields > 3% that could complement more growth oriented positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.