Assessing Luckin Coffee (OTCPK:LKNC.Y) Valuation After Opening Its 30,000th Origin Flagship Store

Luckin Coffee (OTCPK:LKNC.Y) just marked a major milestone by inaugurating its 30,000th store in Shenzhen, the first Origin Flagship, which puts its expanded format, supply chain story and premium positioning in clearer focus for investors.

Investors have seen mixed momentum in Luckin Coffee this year, with a 6.73% 1 month share price return and a 20.7% 1 year total shareholder return. This suggests the Shenzhen Origin Flagship and upcoming 2025 results are feeding into shifting expectations.

If this expansion has you thinking about where else growth stories might emerge around consumer brands and retail formats, it could be worth scanning our 23 top founder-led companies as a fresh source of ideas.

With shares up 21% over the past year, a value score of 4, and the last close at US$36.45 versus an analyst target of about US$48.76, you have to ask: Is there still upside here, or is future growth already priced in?

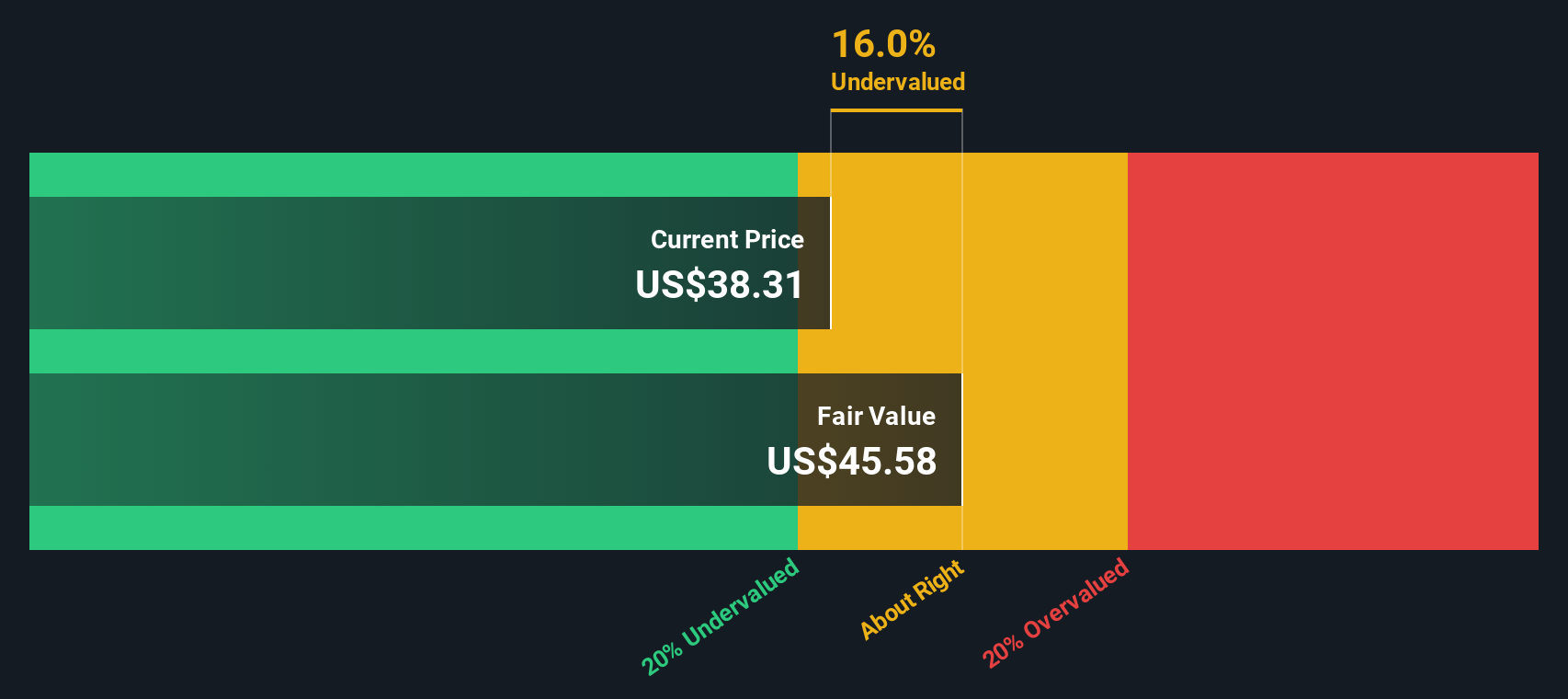

Most Popular Narrative: 25% Undervalued

With the most followed fair value sitting at about $48.60 versus the last close of $36.45, the current market price sits well below that narrative line.

Ongoing investments in proprietary supply chain infrastructure such as the commissioning of the new Xiamen roasting facility and integration of existing plants are expected to enhance vertical integration, lower cost of materials as a percent of revenues, and drive expansion of gross and net margins over the long term.

Want to see what earnings path and margin profile sit behind that fair value and discount rate? The full narrative lays out the revenue climb, profitability arc and valuation multiple that need to come together for the story to hold.

Result: Fair Value of $48.60 (UNDERVALUED)

However, you still need to weigh the risk that rapid store expansion and rising delivery related costs could pressure margins and challenge the current upside narrative.

Another View: Cash Flows Paint A Different Picture

While the fair value narrative points to about $48.60 per share as undervalued, our DCF model tells a different story. On that view, Luckin Coffee's current price of $36.45 sits above an estimated future cash flow value of $24.69, which screens as overvalued and raises a simple question: which set of assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Luckin Coffee for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Luckin Coffee Narrative

If you see the numbers differently or simply prefer to test your own assumptions against the data, you can build a tailored view in minutes: Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Luckin Coffee.

Ready to hunt for your next idea?

If this Luckin Coffee story has you thinking bigger, do not stop here. The next strong opportunity you size up early could make a real difference.

- Start with value by checking companies that screen as attractively priced relative to quality using our 53 high quality undervalued stocks curated from the Simply Wall St screener.

- Prioritise resilience by scanning businesses with stronger balance sheets and fundamentals through our solid balance sheet and fundamentals stocks screener (44 results) so you are not only focused on headlines.

- Broaden your watchlist by reviewing our screener containing 23 high quality undiscovered gems, a screener built to surface quality ideas you might not see in the usual stock picks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.