Assessing Lumen Technologies (LUMN) Valuation After CEO Share Purchase And AI Infrastructure Pivot

Lumen LUMN | 0.00 |

CEO share purchase and AI focus shift investor attention

Lumen Technologies (LUMN) has been back on radar after CEO Kate Johnson bought about US$500,000 of stock following a 21% drop, with the move followed by a 29% rebound the next day.

The purchase came shortly after mixed fourth quarter results and alongside Lumen’s push to position its network as core infrastructure for AI. This is supported by more than US$13b in contracts with large technology customers and recent divestitures to concentrate on enterprise, cloud, and AI services.

Beyond the immediate swing around the CEO’s purchase, Lumen’s 1-year total shareholder return of 82.39% and 3-year total shareholder return of 113.49% contrast with a more moderate 9.10% year-to-date share price return. This suggests that momentum has cooled after a period of strong recovery.

If the AI infrastructure angle at Lumen has caught your attention, it may be worth seeing what else is out there through our screener of 34 AI infrastructure stocks.

With Lumen’s shares up strongly over 1 year but closer to flat in the past month, and with recent losses and AI contracts now in focus, the key question is whether today’s price offers a genuine entry point or if markets are already pricing in future growth.

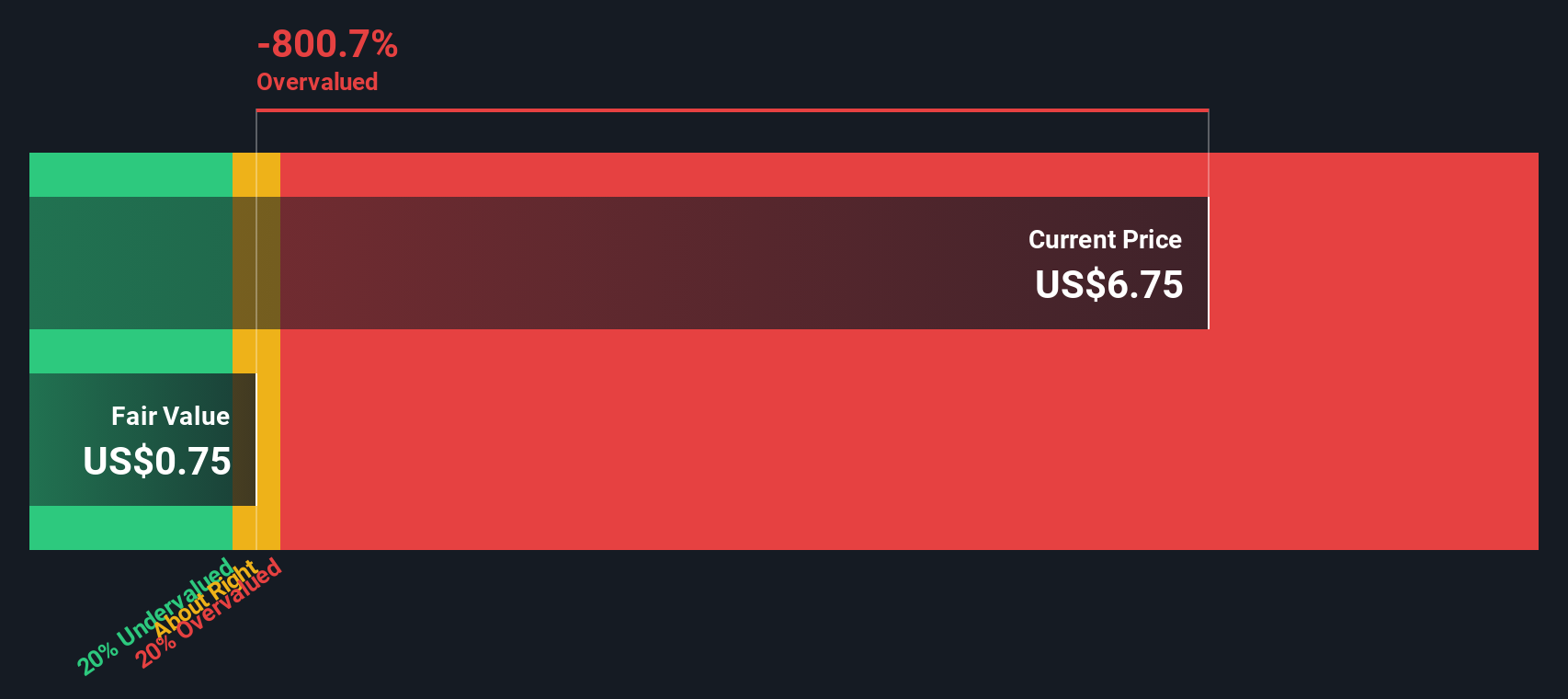

Most Popular Narrative: 16% Overvalued

The most followed valuation view currently puts Lumen Technologies’ fair value at about $7.23 per share, compared with the latest close of $8.39, which sets up a cautious tone for the story that follows.

Lumen's large pipeline of AI-driven network infrastructure and Platform Connectivity Fiber (PCF) contracts, particularly with hyperscalers and data center providers, positions the company to capture long-duration, higher-margin recurring revenues from explosive data growth, benefiting long-term revenue and margin expansion.

Curious how a turnaround story with shrinking revenue, rising loss, and high expected returns can still support that price tag. The fair value hinges on a specific mix of margin rebuild, earnings power and valuation multiple. Want to see exactly how those moving parts are stitched together and what has to go right for it all to line up.

Result: Fair Value of $7.23 (OVERVALUED)

However, there is still the risk that double digit declines in legacy products and a heavy debt load could limit how much value the AI story can support.

Another View: Market Pricing Versus Cash Flows

While the most popular narrative suggests Lumen is about 16% overvalued on earnings assumptions, our DCF model is even more cautious, putting fair value at $1.31 per share compared to the current $8.39. That is a wide gap, so which story do you think is closer to reality?

Build Your Own Lumen Technologies Narrative

If you are not on board with these views or simply prefer to test the numbers yourself, you can build a custom Lumen story in just a few minutes: Do it your way.

A great starting point for your Lumen Technologies research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one stock, you might miss opportunities that suit your goals better, so use the screener to see what else lines up with your approach.

- Target potential value opportunities by checking companies on our list of 53 high quality undervalued stocks that combine quality fundamentals with prices some investors may find appealing.

- Prioritize stability and capital protection by reviewing 84 resilient stocks with low risk scores that score well on our risk checks and may suit more cautious portfolios.

- Hunt for overlooked stories by scanning our screener containing 23 high quality undiscovered gems where strong fundamentals have not yet drawn broad attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.