Assessing LyondellBasell (LYB) Valuation After Quarterly Loss And Portfolio Reshaping Plans

LyondellBasell Industries NV LYB | 79.60 | +3.77% |

LyondellBasell Industries (LYB) is back in focus after reporting a fourth quarter loss of US$142 million, with revenue above forecasts, alongside continued portfolio reshaping and asset divestment plans.

The latest update comes after a strong short term rebound, with a 1 day share price return of 6.37% and a 30 day share price return of 20.41%, while the 1 year total shareholder return is a 24.96% loss. Together with the portfolio reshaping and asset sales, this mix of sharp recent gains and weaker long term total shareholder returns suggests that investors may be reassessing both the risks and the potential payoff as the turnaround progresses.

If you are comparing LyondellBasell with other industrial names, this could be a useful moment to scan fast growing stocks with high insider ownership for ideas that pair strong fundamentals with committed insiders.

With the shares rebounding strongly in the short term yet still sitting on a weak multi-year total return, and with an intrinsic value estimate suggesting a large discount, is this a genuine opportunity or is the market already pricing in any recovery?

Most Popular Narrative: 4% Overvalued

At a last close of $53.45 versus a narrative fair value of $51.61, LyondellBasell is framed as slightly expensive, with that view resting heavily on how its recycling and technology bets reshape future earnings power under a 9.20% discount rate.

LyondellBasell's strategic investments in circular and advanced recycling (MoReTec-1 and plans for MoReTec-2, plus expanding renewable feedstock capacity in Europe) position the company to benefit from rising regulatory and consumer demand for recycled and sustainable plastics, improving product mix and supporting higher net margins and long-term revenue growth.

Curious how a company with shrinking forecast revenues still lands a premium to fair value? The narrative leans on margin rebuild, earnings compounding and a reset profit multiple that contrasts sharply with today. The full story connects these ingredients into one valuation case.

Result: Fair Value of $51.61 (OVERVALUED)

However, this depends on avoiding a prolonged petrochemical downturn and on planned recycling and capacity projects not being delayed. Both factors could undermine the upbeat narrative.

Another Take On Valuation

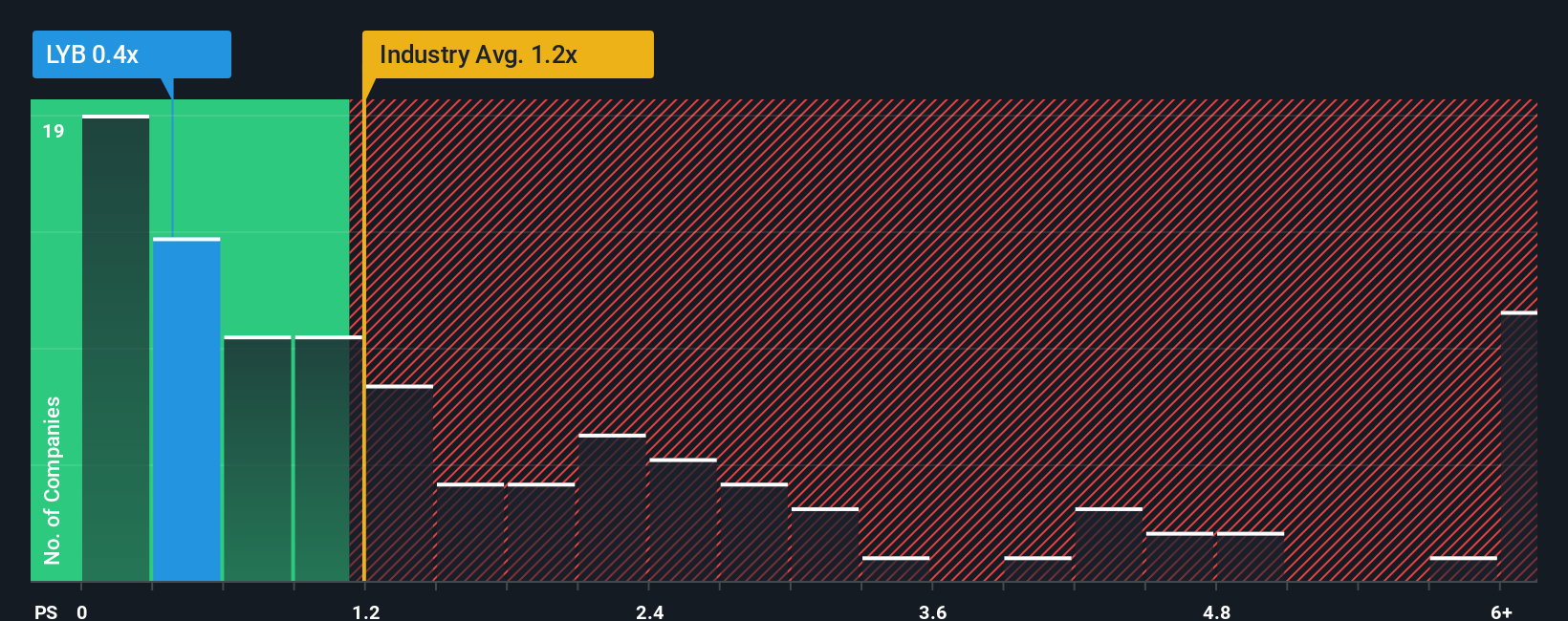

That fair value of $51.61 points to a small premium at today’s $53.45, yet the simple sales based lens tells a different story. LyondellBasell trades on a P/S of 0.5x versus 0.7x for similar peers, 1.2x for the US Chemicals industry, and a fair ratio of 0.7x. If the market drifted closer to that fair ratio, the gap could matter a lot more than a 4% narrative premium. Which signal do you trust more right now?

Build Your Own LyondellBasell Industries Narrative

If this take does not quite fit your view, or you would rather lean on your own work, you can pull the same data, test your assumptions and build a personalised thesis in just a few minutes with Do it your way.

A great starting point for your LyondellBasell Industries research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If you stop with just one company, you could miss opportunities that fit your style even better, so take a few minutes to scan fresh ideas now.

- Spot potential bargains early by reviewing these 867 undervalued stocks based on cash flows that may be pricing in more pessimism than their cash flow profiles suggest.

- Tap into AI driven trends by checking out these 25 AI penny stocks that are tying their growth plans to machine learning and automation.

- Boost your income focus by shortlisting these 13 dividend stocks with yields > 3% that combine higher yields with underlying business fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.