Assessing Maase (MAAS) Valuation After A Sharp Multi‑Month Share Price Surge

Maase Inc MAAS | 0.00 |

Recent price action and business snapshot

Maase (MAAS) has drawn investor attention after a 63% share price move over the past month and 58% over the past 3 months, prompting a closer look at its current fundamentals.

The company provides technological intelligence and capital investment services in China through a technology-driven independent financial service platform and independent wealth management services. It reports revenue of CN¥3.483 and a net loss of CN¥1.775.

After a strong 65.49% year to date share price return and a sharp 63.39% 30 day move, Maase’s recent momentum contrasts with the small 0.62% 1 day pullback at the latest US$9.64 close. This hints at shifting sentiment around its risks and potential.

If Maase’s surge has you thinking about what else is moving, this could be a good moment to scan the market for other fast evolving platforms via the 17 top founder-led companies

With Maase posting strong recent returns but still carrying an intrinsic discount and reporting a net loss, the key question for you is simple: is the stock undervalued or is the market already pricing in future growth?

Preferred price to book multiple of 15x: Is it justified?

Maase trades on a P/B of 15x, which is high relative to both the US Insurance industry and its closest peers, raising questions about what the market is paying up for at the current $9.64 share price.

P/B compares a company’s market value to its net assets, so a higher multiple usually reflects expectations of stronger profitability, superior business quality, or valuable intangibles that do not sit cleanly on the balance sheet.

Here, the picture is mixed for readers to weigh. Maase is currently loss making, reports a return on equity of 0.092% in the red, has less than three years of financial history and makes under $1 million in revenue, yet carries a P/B that is 10 times the US Insurance sector average and a little over 3 times the peer average.

The gap is stark. The US Insurance industry average P/B sits at 1.5x and Maase’s peer average at 4.7x, compared with Maase at 15x, which means the stock is priced at a much richer level than both its broader sector and closer comparables based on book value alone.

Result: Price to book of 15x (OVERVALUED)

However, there are clear risks here, including the current net loss of CN¥1.775 and the reliance on a small CN¥3.483 revenue base from a single market.

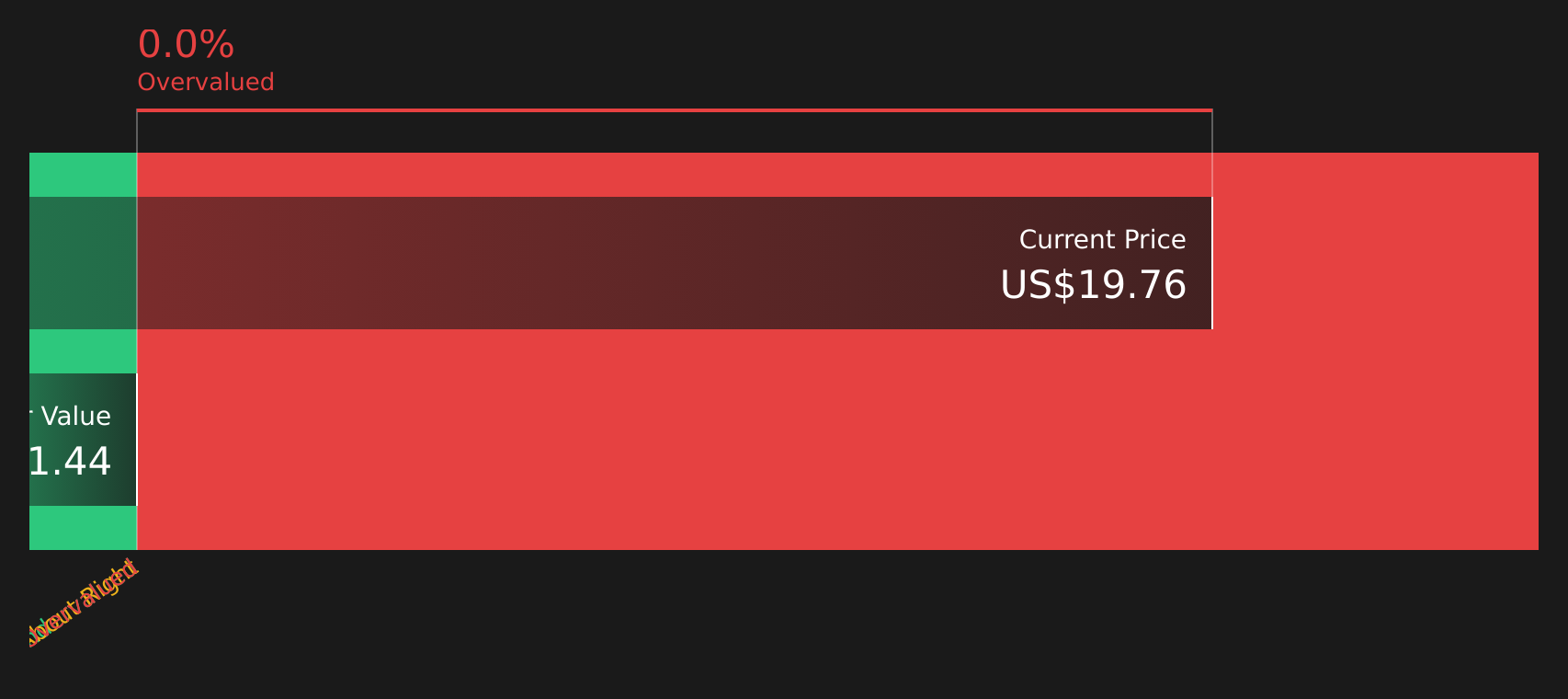

Another view on Maase’s valuation

The DCF model tells a very different story from the 15x P/B ratio. Our DCF workup suggests Maase’s $9.64 share price sits well above an estimated future cash flow value of $1.51, which points to an overvalued stock rather than a bargain on cash flow terms.

That gap leaves you with a clear tension to consider: is the market correctly pricing in potential that cash flow models do not capture, or is it stretching too far beyond what current fundamentals support?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Maase for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of strong price moves and valuation tension leaves you unsure, review the details closely and decide quickly where you stand by starting with the 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If Maase has sharpened your focus, do not stop here. Widen your net and line up a few fresh ideas before the next move catches you off guard.

- Target dependable cash generators by scanning for companies with resilient payouts and strong balance sheets via the 13 dividend fortresses.

- Hunt for quality at a discount by using the 49 high quality undervalued stocks to spot stocks where fundamentals and price are still out of sync.

- Unearth under-the-radar opportunities early by filtering through the screener containing 25 high quality undiscovered gems before the crowd starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.