Assessing MACOM (MTSI) Valuation After Strong Q1 Results And Data Center Demand Surge

MACOM Technology Solutions MTSI | 0.00 |

Why MACOM’s latest results caught the market’s attention

MACOM Technology Solutions Holdings (MTSI) kicked off fiscal 2026 with first quarter results that turned a prior year loss into profit, alongside firm demand in data center products and a higher revenue outlook.

The earnings beat and higher revenue guidance arrived alongside strong momentum in the shares, with a 10.64% 1 month share price return and a 52.76% 3 month share price return. The 1 year total shareholder return of 98.31% suggests the recent move is part of a longer upswing.

If MACOM’s data center story has your attention, this could be a good moment to look across the sector using our screener of 34 AI infrastructure stocks as potential next research ideas.

With the shares up sharply and MACOM now trading only about 5% below the average analyst price target, the key question is whether the current valuation still leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 4.5% Undervalued

The most followed narrative sees fair value at about $255.73, slightly above the last close of $244.16, which puts recent gains into sharper context.

Analysts have lifted their fair value estimate for MACOM Technology Solutions Holdings by about $48.60 per share, reflecting revised assumptions for revenue, profit margins and future P/E multiples supported by a series of recent price target increases across the Street.

Want to see what justifies that higher fair value? Revenue growth assumptions, margin expectations and a richer future earnings multiple are all doing serious heavy lifting.

Result: Fair Value of $255.73 (UNDERVALUED)

However, you still need to weigh risks such as volatile data center and telecom demand, as well as the execution challenges tied to ramping the RTP fab.

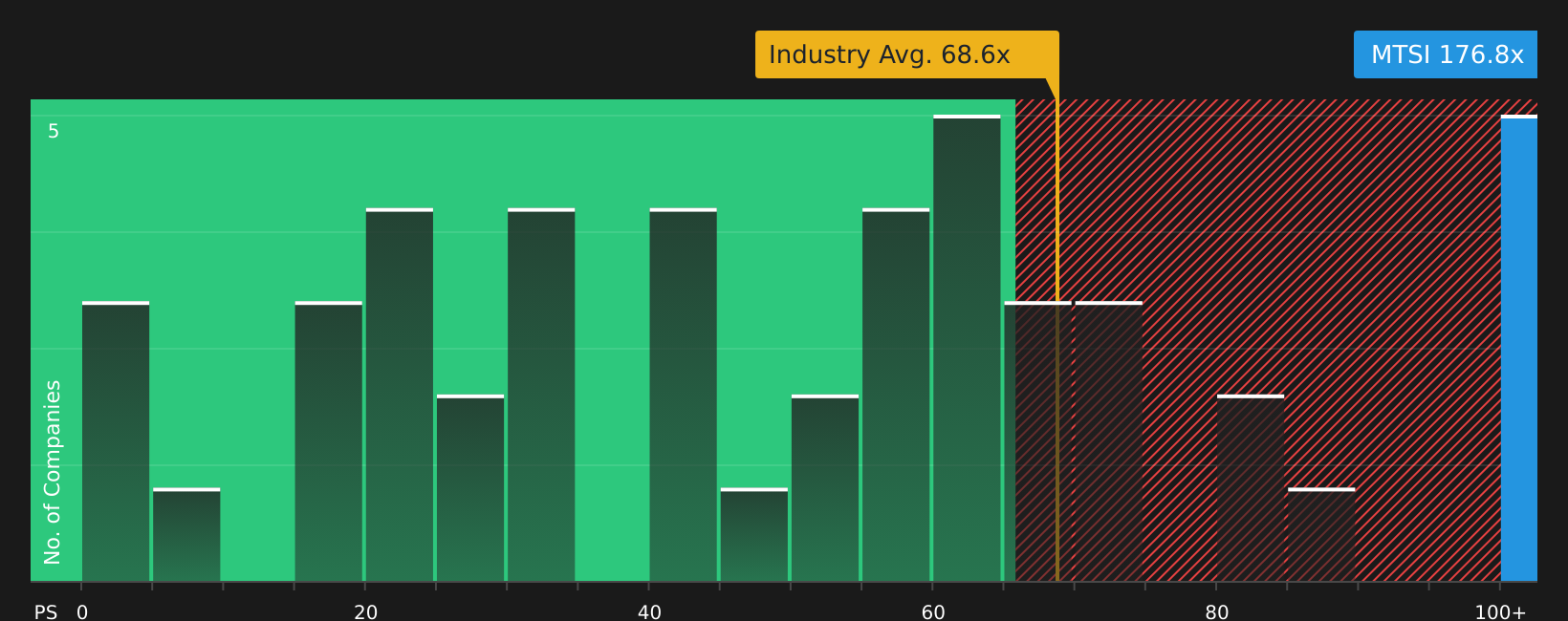

Another way to look at MACOM’s valuation

The fair value narrative points to a modest 4.5% undervaluation, but the current P/E of 113x tells a different story. That is far above the US Semiconductor industry at 43.4x, the peer average at 40.3x, and the fair ratio of 38.4x. This suggests meaningful valuation risk if sentiment cools.

Build Your Own MACOM Technology Solutions Holdings Narrative

If you see the numbers differently or simply want to test your own view, you can build a custom MACOM story yourself in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding MACOM Technology Solutions Holdings.

Looking for more investment ideas?

If MACOM has sharpened your focus, do not stop here. A broader watchlist can help you spot opportunities that match your goals before others react.

- Target strong fundamentals and staying power by scanning our solid balance sheet and fundamentals stocks screener (45 results) that highlights companies with robust financial footing.

- Hunt for potential value by checking our screener containing 23 high quality undiscovered gems where less-followed businesses with solid numbers might be hiding in plain sight.

- Prioritize resilience with our 84 resilient stocks with low risk scores to see companies that score well on overall risk and may suit a more cautious approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.