Assessing Martin Marietta Materials (MLM) Valuation After Strong Long Term Returns And Recent Share Pullback

Martin Marietta Materials, Inc. MLM | 616.94 616.94 | -2.20% 0.00% Pre |

What Martin Marietta Materials’ Recent Performance Tells Investors

Martin Marietta Materials (MLM) has drawn attention after a period of mixed share performance, with a small 1 day decline and a modest pullback over the past week, as well as a stronger total return over the past year.

While the 1 day and 7 day share price returns have slipped, the 90 day share price return of 10.67% and 1 year total shareholder return of 24.87% suggest momentum has been building over a longer stretch.

If this has you thinking about other construction and infrastructure related themes, it could be worth scanning our list of 25 power grid technology and infrastructure stocks as a starting point for fresh ideas.

With the shares recently easing back despite a 1 year total return of 24.87% and analysts’ price targets sitting only slightly higher than the last close, you have to ask: is there real value left here or is the market already pricing in future growth?

Most Popular Narrative: 3.1% Undervalued

Martin Marietta Materials’ most followed narrative puts fair value at about $680.88, a little above the recent $660.07 close, which sets up a relatively tight valuation debate.

The exchange of cement and ready-mix assets for high-quality aggregate operations in Virginia, Missouri, Kansas, and Vancouver, BC, strategically increases Martin Marietta's exposure to advantaged geographies with strong barriers to entry and pricing power, expected to enhance margins and support stable earnings growth over time.

If you want to see what is really driving that fair value, look at how the narrative connects multi year revenue growth, margin expansion, and a richer earnings multiple.

Result: Fair Value of $680.88 (UNDERVALUED)

However, this hinges on infrastructure funding staying on track and construction demand holding up, so any pullback there could quickly challenge the current underpriced story.

Another Angle On Valuation

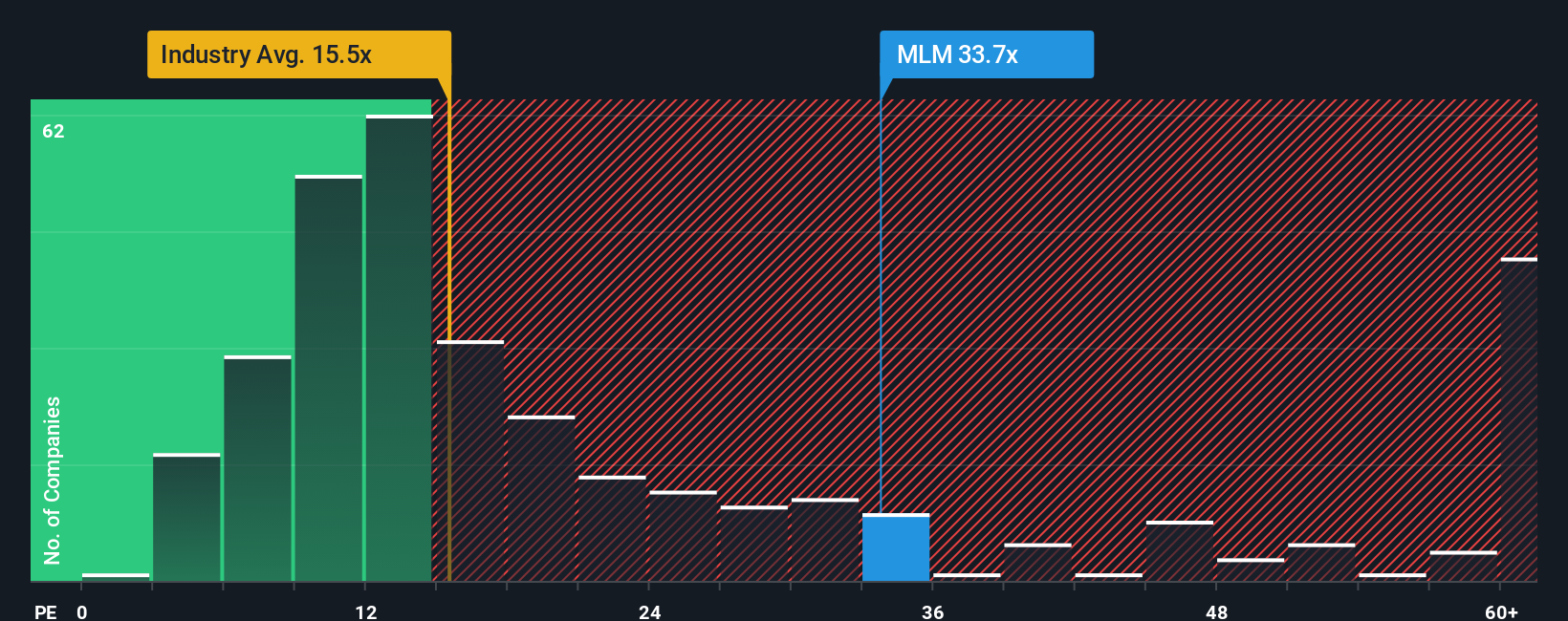

The popular narrative calls Martin Marietta Materials about 3.1% undervalued at a fair value of $680.88, but the current P/E of 40.2x tells a different story. That is well above the estimated fair ratio of 25.5x, the global Basic Materials average of 15.6x, and the peer average of 27.5x.

In plain terms, the market is asking you to pay a premium price for each dollar of earnings, compared with both the wider industry and closer peers. That kind of gap can work out if everything goes right, but it also leaves less room for disappointment, so which set of assumptions do you trust more?

Build Your Own Martin Marietta Materials Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a full narrative in just a few minutes, starting with Do it your way.

A great starting point for your Martin Marietta Materials research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If you stop with just one company, you could miss other opportunities that fit your goals even better, so broaden your search with a few focused stock lists.

- Target quality at a discount by scanning our 55 high quality undervalued stocks and see which companies combine solid fundamentals with prices that may not fully reflect them.

- Strengthen your income stream by reviewing 16 dividend fortresses that pair higher yields with an emphasis on stability.

- Prioritise resilience by checking out 85 resilient stocks with low risk scores that stand out for lower risk scores and sturdier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.