Assessing Medpace Holdings (MEDP) Valuation After Robust Quarterly Results And Share Repurchases

Medpace MEDP | 498.34 | +1.81% |

Recent investor letters spotlighted Medpace Holdings (MEDP) after quarterly results exceeded expectations, with accelerated growth, a strong balance sheet, solid free cash flow, and sizable share repurchases at what investors viewed as attractive valuation levels.

The share price has consolidated around US$602.06 after a 2.38% 1 day share price return and a 6.08% 30 day share price return, while the 1 year total shareholder return of 71.84% and 5 year total shareholder return of 337.61% indicate strong long term momentum. Recent earnings and buybacks appear to have reinforced this trend rather than reversed it.

If Medpace’s run has you thinking about what else is working in healthcare, it could be a good moment to scan healthcare stocks for other ideas with potential.

With the shares around US$602.06, Medpace now trades close to investor estimates of intrinsic value and above the average analyst price target, so should you see this as a fresh opportunity or a market that is already pricing in future growth?

Most Popular Narrative: 10.3% Overvalued

With Medpace at $602.06 versus a narrative fair value of about $545.75, the current price sits above what this widely followed framework suggests. This puts the focus squarely on the growth assumptions behind that gap.

The analysts have a consensus price target of $423.636 for Medpace Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $510.0, and the most bearish reporting a price target of just $305.0.

Want to see what has to happen for that fair value to hold up? Revenue, earnings and margins are all carefully wired into this model. The key point is how future profitability and the chosen earnings multiple work together. Curious which assumptions really carry the weight here?

Result: Fair Value of $545.75 (OVERVALUED)

However, if trial funding softens or backlog and bookings fall further, earnings visibility could tighten and challenge the optimistic assumptions built into current valuation models.

Another View: Cash Flows Point a Different Way

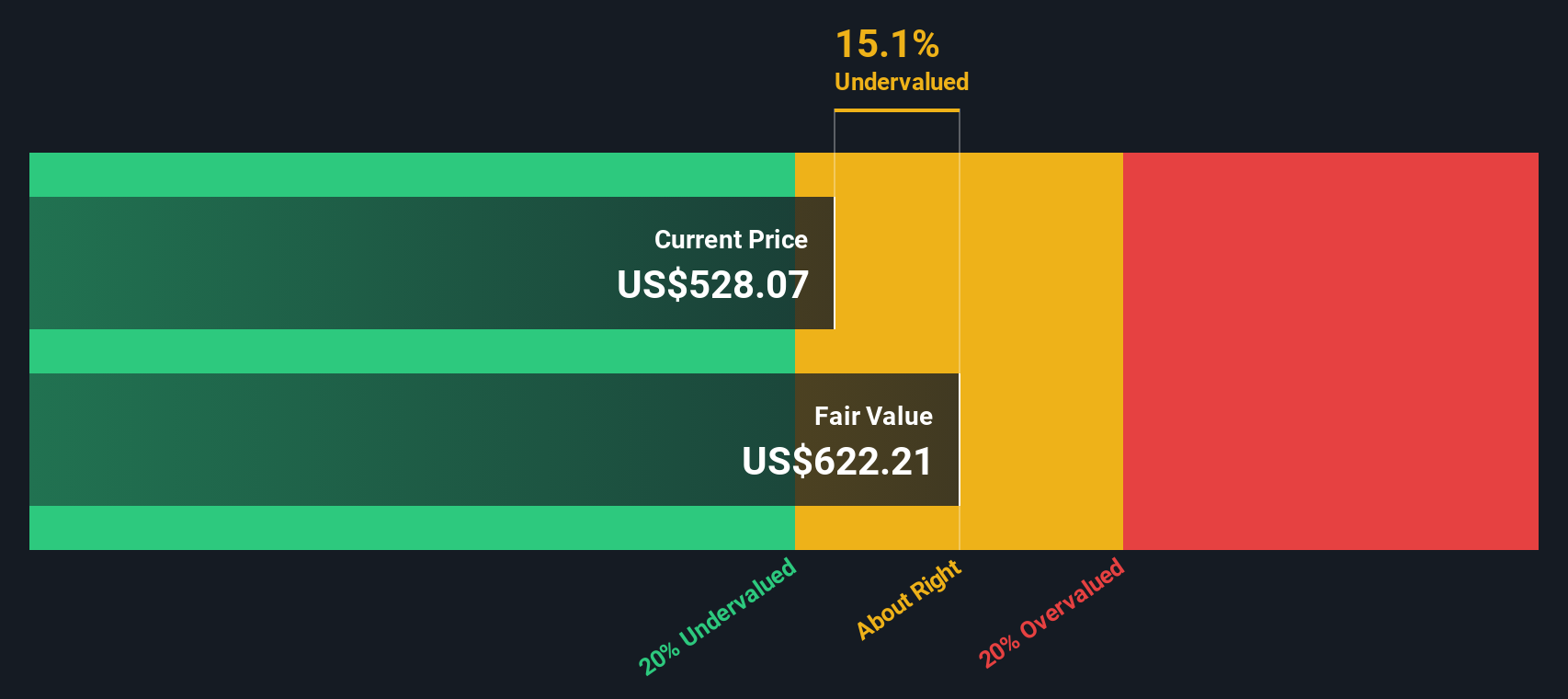

While the narrative fair value of about $545.75 frames Medpace as roughly 10% overvalued at $602.06, our DCF model points in the opposite direction. On that approach, the shares sit about 17.9% below an estimated future cash flow value of roughly $733, which raises a very different question about upside and risk.

Build Your Own Medpace Holdings Narrative

If you see the numbers differently or prefer to lean on your own work, you can test the data, challenge the assumptions, and Do it your way in just a few minutes.

A great starting point for your Medpace Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Medpace has your attention, do not stop there. Use the Simply Wall Street Screener to quickly surface fresh ideas that fit the way you like to invest.

- Hunt for potential value opportunities by scanning these 885 undervalued stocks based on cash flows that screen on cash flow based metrics rather than short term headlines.

- Tap into long term themes in automation and machine learning with these 23 AI penny stocks that focus on companies tied to real business adoption of AI.

- Position your portfolio for income potential using these 13 dividend stocks with yields > 3% to spot companies offering dividend yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.