Assessing Merck (MRK) Valuation After Mixed Short Term Performance And Conflicting Fair Value Signals

Merck MRK | 0.00 |

Merck stock triggered by recent performance metrics

Merck (MRK) is back on investors’ radar after a recent stretch of mixed share performance, including a gain of about 6% over the past month alongside modest declines over the past week.

Short term momentum has softened, with the share price down 3.0% over the past week after a 5.9% gain over 30 days. However, the year to date share price return of 11.5% and 1 year total shareholder return of 60.1% point to a much stronger longer term trend.

If Merck’s recent moves have you thinking about what else is changing in healthcare, it could be a good time to scan for other opportunities in rapidly growing medical AI, including 38 healthcare AI stocks

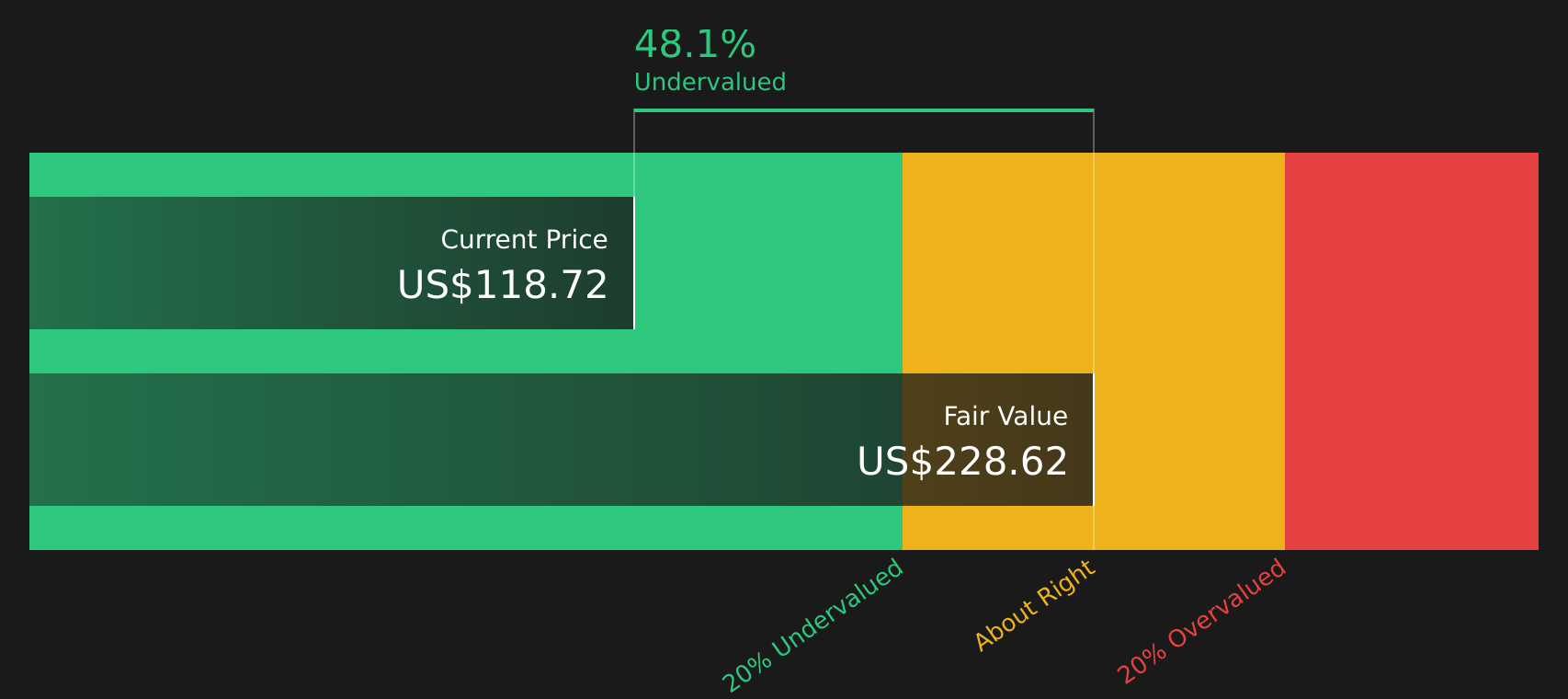

With Merck trading around $118.72, showing an estimated 48% intrinsic discount and about a 9% gap to analyst targets, the central question is whether this represents genuine value or whether the stock already reflects future growth.

Most Popular Narrative: 5.5% Overvalued

According to the most followed narrative, Merck’s fair value sits at $112.55, a touch below the last close at $118.72, which tilts the story slightly to the expensive side.

Merck & Co. presents a compelling long-term investment case, underpinned by its innovative capacity and strong market position. The current valuation, considering both quantitative metrics and qualitative factors, suggests an attractive entry point for investors willing to weather near-term volatility.

Want to see what justifies paying above that fair value line? The narrative leans heavily on future earnings power and a profit profile most pharma peers do not match. The key assumptions sit in how long those margins hold up and how rich the future earnings multiple runs. Curious which pieces of the story carry the most weight in that $112.55 figure?

Result: Fair Value of $112.55 (OVERVALUED)

However, this story can shift quickly if Keytruda faces faster than expected competitive pressure, or if new pipeline drugs encounter regulatory or clinical setbacks.

Another View: DCF Points to Deep Undervaluation

While the popular narrative suggests Merck is about 5.5% overpriced at $118.72 versus a $112.55 fair value, the SWS DCF model lands in a very different place. It puts fair value at $228.62, which implies Merck trades roughly 48% below that estimate. Which perspective aligns best with the level of risk you are willing to take?

To see how that cash flow based view is built, and what would need to change for it to shift, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Merck for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across fair value estimates, are you leaning bullish or cautious? Act quickly by reviewing the full picture, including 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Merck has sharpened your focus, do not stop here. Use Simply Wall Street's tools to spot other stocks that could fit your goals before others do.

- Target opportunities where market pessimism might be overdone by scanning 46 high quality undervalued stocks and seeing which stocks still look out of favour.

- Strengthen your income toolkit by checking out 10 dividend fortresses that could complement Merck in a yield focused portfolio.

- Prioritise resilience by reviewing 63 resilient stocks with low risk scores that aim to pair steadier risk profiles with solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.