Assessing Mercury Systems (MRCY) Valuation After Earnings Beat And Ongoing Losses

Mercury Systems, Inc. MRCY | 85.51 | +1.69% |

Mercury Systems (MRCY) just released quarterly results that beat analyst expectations on both earnings and revenue, driven by accelerated customer deliveries and a strong backlog, yet the company remains loss making with cautious commentary.

The earnings beat and record backlog helped the share price gain 3.96% on the day. That follows a 12.44% 7 day share price return decline and a softer 30 day move, while the 1 year total shareholder return of 81.26% and 3 year total shareholder return of 51.91% still point to strong longer term momentum.

If Mercury Systems has put defense electronics on your radar, you may want to broaden your search with our screener of 33 AI infrastructure stocks as another way to spot potential opportunities tied to advanced computing demand.

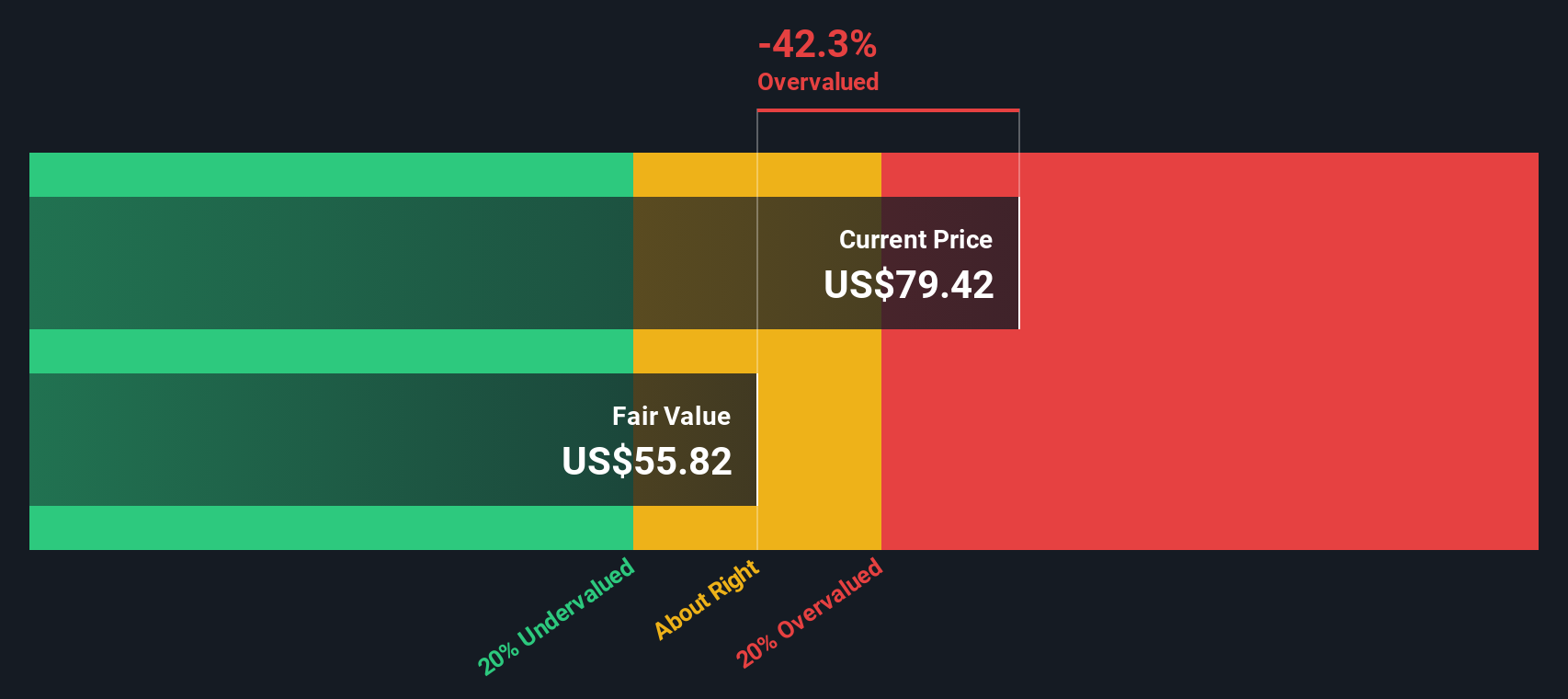

With Mercury Systems still loss making but backed by a record backlog and trading about 20% below the average analyst price target, the key question is whether there is still an investment opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 4.4% Undervalued

Mercury Systems last closed at $82.20 against a widely followed fair value estimate of $86, which presents an interesting gap for investors to consider.

Investments in R&D and expanded product offerings (including acquisition integration and common processing architectures) are enabling wins in next-generation programs and recurring business, supporting a long-term transition toward a higher-margin, more predictable earnings model.

Want to see what is incorporated into that fair value? The narrative focuses on future margin rebuild, steadier revenue growth and a richer earnings profile. The exact balance of those elements is where it gets interesting.

Result: Fair Value of $86 (UNDERVALUED)

However, there are still questions around low margin legacy contracts running through FY26 and the risk that earlier delivery pull forwards may leave future revenue looking thinner.

Another Angle: Cash Flows Point to a Richer Price

While the fair value narrative suggests Mercury Systems is about 4.4% undervalued at $82.20 versus $86, our DCF model tells a different story. On future cash flows, the shares screen as expensive, with the current price above an estimated value of $69.08. Which lens do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mercury Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Mercury Systems Narrative

If you are not fully on board with this view or simply prefer to dig into the numbers yourself, you can build and stress test your own Mercury Systems story in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Mercury Systems.

Looking for more investment ideas?

If Mercury Systems has sparked your interest, do not stop here. Expanding your idea set can help you spot opportunities you might otherwise miss.

- Target potential value opportunities by running our screener of 53 high quality undervalued stocks that stand out on both quality and price.

- Prioritize resilience first and check out 86 resilient stocks with low risk scores that score well on our risk metrics and may offer a steadier ride.

- Hunt for under followed stories with the screener containing 24 high quality undiscovered gems that combine solid fundamentals with limited market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.