Assessing Mettler-Toledo (MTD) Valuation After Recent Share Price Weakness And Mixed Returns

Mettler-Toledo International Inc. MTD | 1259.94 | -1.11% |

Mettler-Toledo International (MTD) has drawn investor interest after recent trading left the shares around $1,392.65, with a value score of 1 and mixed total returns over the past year and past 3 months.

With the share price at US$1,392.65, Mettler-Toledo’s recent 30 day share price return of a 6.66% decline and relatively flat 90 day move contrast with a 6.10% gain in 1 year total shareholder return and a 19.39% total shareholder return over 5 years, which hints that near term momentum has faded even though longer term holders have still seen gains.

If this price action has you thinking about where else capital could work, it might be a good time to widen your search with our 22 top founder-led companies as potential long term compounders.

With the share price near US$1,392 and a low value score of 1 despite steady revenue and net income growth, you have to ask: is Mettler-Toledo quietly undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 7.2% Undervalued

Compared with the current share price of $1,392.65, the most followed narrative points to a fair value of about $1,501, built on detailed long term forecasts and a 7.71% discount rate.

Accelerating trends in automation and digitalization of manufacturing and laboratory environments are creating strong, recurring demand for Mettler-Toledo's data-driven solutions and process analytics, enabling greater share of wallet, increased adoption of its automation products, and supporting revenue growth as well as higher-margin recurring software and services.

Curious what kind of revenue path and margin profile need to hold for that valuation to stack up, and how much earnings power the narrative builds in by 2028? The full story connects steady top line growth, firmer profitability and a future earnings multiple that has to tighten from today’s level yet still support a premium price. Want to see exactly how those moving parts combine to reach a fair value around $1,501? The detailed narrative lays out the numbers behind that view.

Result: Fair Value of $1,501 (UNDERVALUED)

However, you still need to weigh risks like unpredictable global tariffs and ongoing softness in China and Europe, which could pressure margins and restrain revenue.

Another Angle On Mettler-Toledo's Valuation

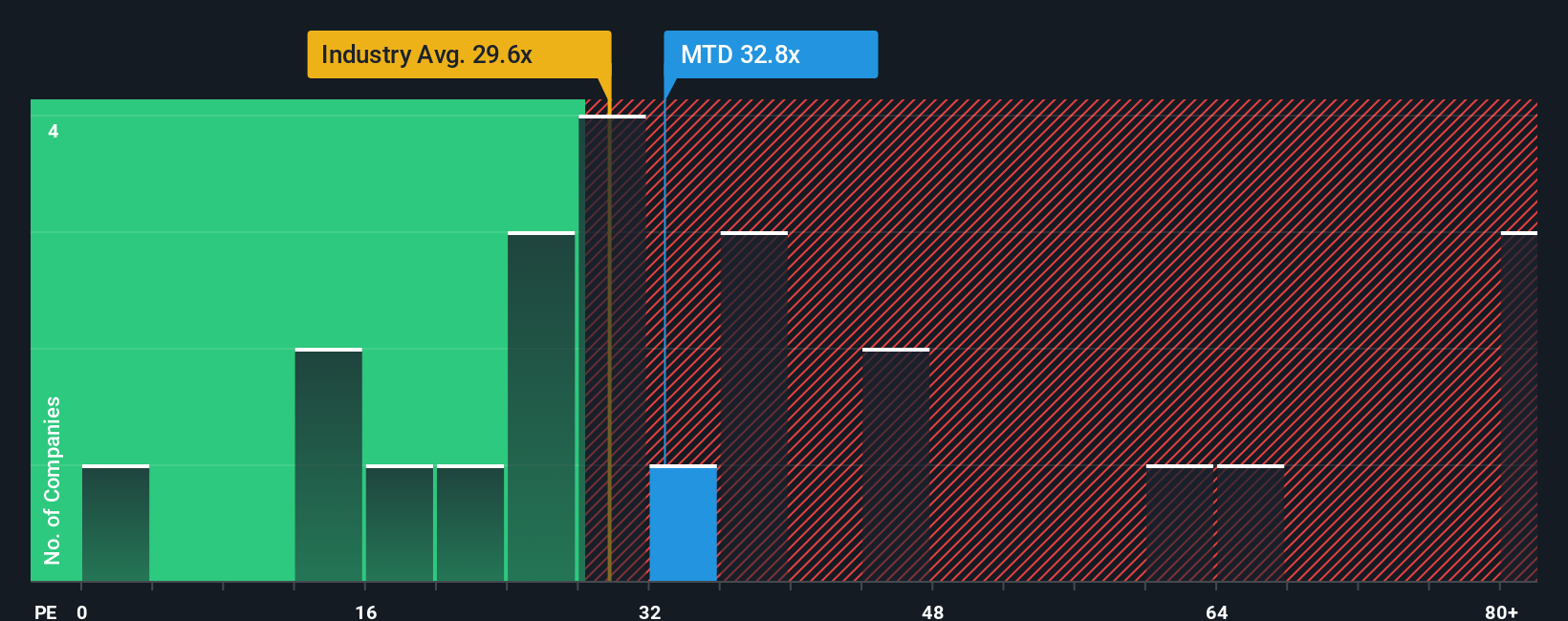

The earlier narrative focuses on long term growth forecasts and a target fair value of about $1,501, but the current P/E of 32.6x tells a different story. It sits just below the North American Life Sciences average of 34x, yet clearly above the fair ratio of 22.8x that our model suggests.

That gap implies the market is already paying a premium that could shrink if expectations cool, even though the stock does not look stretched versus peers. The question for you is whether that premium feels like justified quality or valuation risk waiting for a reset.

Build Your Own Mettler-Toledo International Narrative

If this framework does not quite fit how you see Mettler-Toledo, or you prefer to lean on your own research, you can create a tailored view of the forecasts, risks and valuation in just a few minutes with Do it your way.

A great starting point for your Mettler-Toledo International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are weighing your next move after looking at Mettler-Toledo, do not leave your cash sitting idle when there are other ideas worth your attention.

- Spot potential turnarounds early by checking out 28 elite penny stocks with strong financials that already show stronger financial footing than many expect from this corner of the market.

- Hunt for quality at a price that still looks reasonable by reviewing our 51 high quality undervalued stocks, built from companies with solid fundamentals that may not be fully appreciated.

- Simplify your search for reliability by focusing on 85 resilient stocks with low risk scores, where the emphasis is on businesses with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.