Assessing Modine Manufacturing (MOD) Valuation After Powerful Recent Share Price Momentum

Modine Manufacturing Company MOD | 253.66 | -1.30% |

Modine Manufacturing shares in focus

Modine Manufacturing (MOD) has moved sharply in recent months, with the stock showing an 80.25% return over the past month and 37.94% over the past 3 months. This recent performance has put the company firmly on investors’ radar.

At a share price of $215.72, Modine Manufacturing has seen strong momentum, with a 16.82% 7 day share price return and a very large 5 year total shareholder return, which may indicate that sentiment has shifted sharply in its favor recently.

If Modine’s surge has you thinking about what else might be gaining traction, you may consider running a broader search through our screener of 24 power grid technology and infrastructure stocks to see other potential ideas.

With Modine’s value score of 1 and the shares trading at a roughly 12% discount to the average analyst price target and around a 14% discount to one intrinsic estimate, you have to ask: is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 17.9% Overvalued

Compared with the current share price of $215.72, the most followed narrative pins Modine Manufacturing’s fair value at $183.00, creating a clear valuation gap that hinges on aggressive growth in higher tech cooling markets.

The accelerating build-out of data centers and the need for next-generation cooling solutions are driving extraordinary demand for Modine's products, with management forecasting the potential to double data center revenues from ~$1 billion in fiscal '26 to $2 billion by fiscal '28; this structural demand from digital infrastructure is set to materially boost revenue growth and deliver significant operating leverage over time.

Curious what earnings power has to look like to justify that kind of price tag? The narrative leans on rapid top line expansion, fatter margins and a future earnings multiple that assumes Modine keeps winning in data center cooling. The full story is in how those three levers work together, and what has to go right for the numbers to hold.

Result: Fair Value of $183 (OVERVALUED)

However, that story can break if data center orders slow, or if Modine’s acquisitions and exits prove harder to integrate and reshape than current models assume.

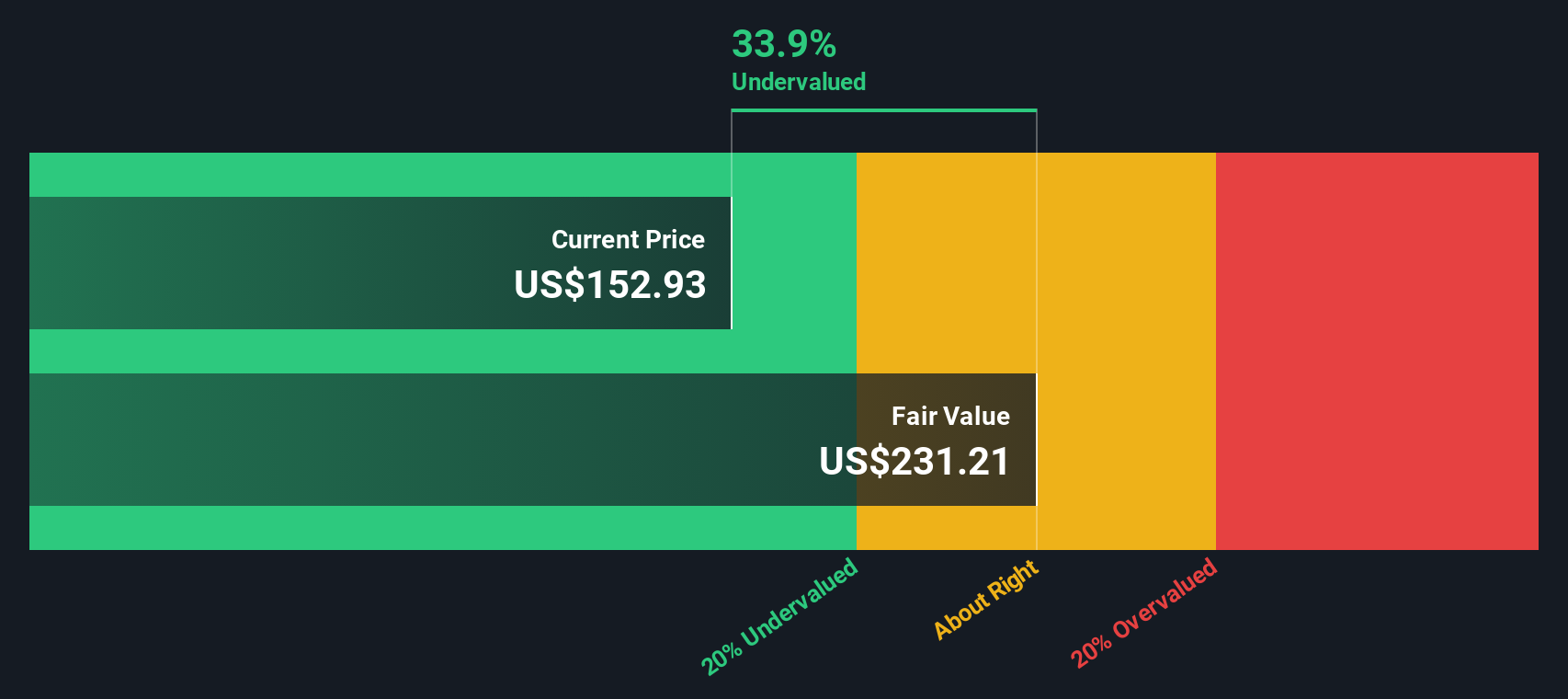

Another View: Cash Flows Paint a Different Picture

While the popular narrative tags Modine Manufacturing as 17.9% overvalued at a fair value of $183, our DCF model points the other way. It indicates a fair value estimate of $252.13 compared with the current $215.72 share price, raising the question of which story you trust more: sentiment or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Modine Manufacturing for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Modine Manufacturing Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can build a personalized Modine thesis in minutes: Do it your way.

A great starting point for your Modine Manufacturing research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Modine has caught your attention, do not stop here. Casting a wider net with focused screeners can reveal opportunities you might regret missing later.

- Spot potential value opportunities early by running our list of 53 high quality undervalued stocks built to highlight companies with appealing pricing signals.

- Prioritize resilience by checking out 86 resilient stocks with low risk scores that concentrates on businesses with lower risk scores and steadier profiles.

- Hunt for lesser known opportunities with our screener containing 25 high quality undiscovered gems designed to surface quality companies that are not yet widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.