Assessing Morgan Stanley (MS) Valuation After Record Dealmaking Revenues And New AI Wealth Tools

Morgan Stanley MS | 165.81 | -0.22% |

Morgan Stanley (MS) has been back in focus after reporting record annual revenues from trading and dealmaking, paired with fresh AI tools in wealth management and reinforced by analyst upgrades and rising earnings estimates.

Those record trading and dealmaking revenues, along with new AI tools and preferred dividend declarations, come after a mixed price patch, with a 9.49% 1 month share price decline, a 7.08% 3 month share price return, and a 26.48% 1 year total shareholder return that reflects longer term momentum.

If you are looking beyond big banks and want to see where technology and disruption are meeting finance, our screener of 16 cryptocurrency and blockchain stocks is a useful place to start your search.

With record trading and dealmaking revenues, a growing AI push in wealth management, and a share price that has recently pulled back, the key question is whether Morgan Stanley is still mispriced or if the market already reflects its future growth.

Most Popular Narrative: 1% Overvalued

At a last close of $171.15 against a narrative fair value of about $169.52, Morgan Stanley is priced slightly above that widely followed view, which leans on steady earnings growth, modestly higher margins, and an updated future earnings multiple.

The ongoing increase in global wealth, combined with the accelerating intergenerational transfer of assets, is boosting demand for comprehensive advisory and wealth management solutions, evidenced by record net new assets and a growing client base, which should drive higher recurring fee-based revenue and long-term earnings growth.

Want to see what kind of revenue climb and margin profile underpin that fair value? The narrative leans on measured growth, richer profitability, and a tighter share count. The full story connects those moving parts to today’s price tag.

Result: Fair Value of $169.52 (OVERVALUED)

However, this hinges on active advisory remaining attractive as low fee ETFs gain ground, and on acquisitions like E*TRADE and Eaton Vance avoiding costly integration setbacks.

Another Take: Market Ratios Send A Different Signal

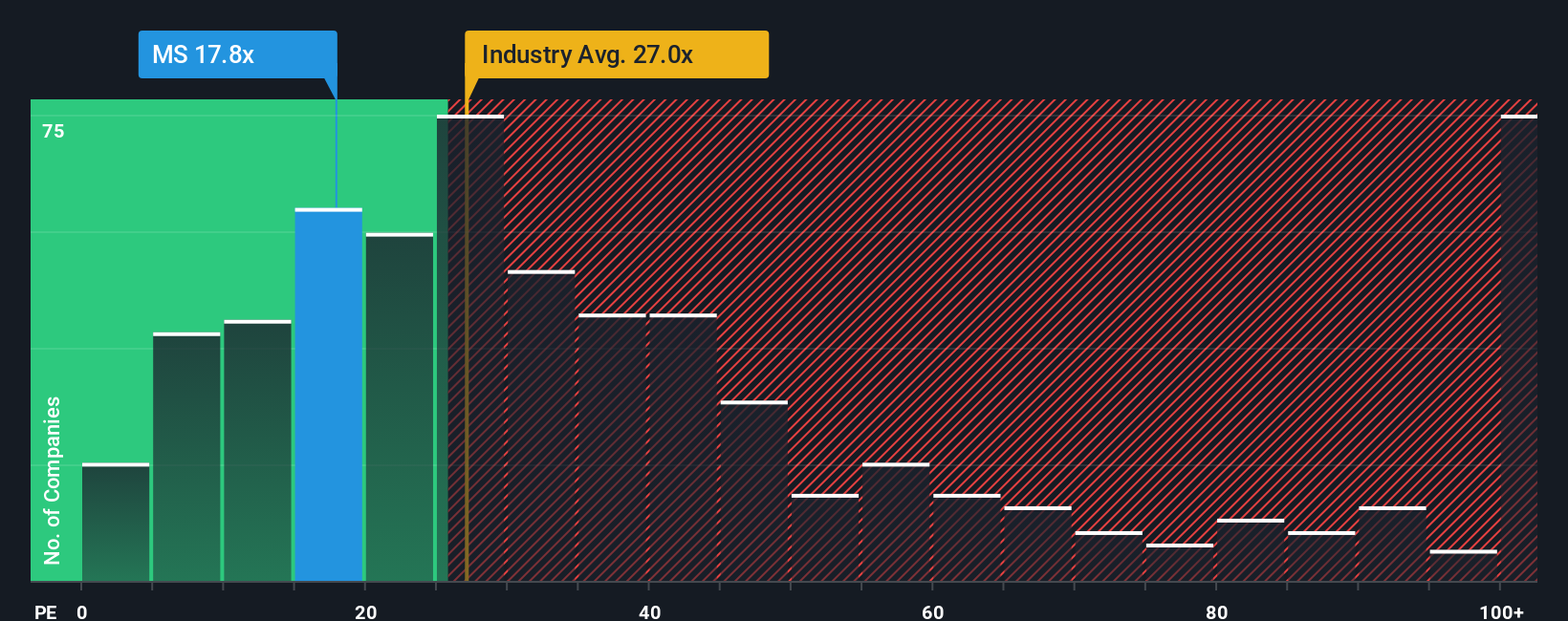

While the narrative fair value pegs Morgan Stanley as slightly overvalued at $171.15 versus about $169.52, the current P/E of 16.7x tells a different story. It sits well below the US Capital Markets industry at 23.1x, the peer average at 26.9x, and the fair ratio of 19.6x, which suggests the market could move closer to that level over time.

That gap points to a trade off for you as an investor, with less optimism priced in than peers, but also less room for error if earnings or sentiment shift. Which signal do you rely on more right now: the slightly rich cash flow model or the comparatively low earnings multiple?

Build Your Own Morgan Stanley Narrative

If you are not fully on board with this view or simply want to stress test it against your own assumptions, you can easily build a custom Morgan Stanley thesis in just a few minutes, starting with Do it your way.

A great starting point for your Morgan Stanley research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Morgan Stanley has sharpened your appetite for quality opportunities, do not stop here. Use focused stock lists to spot ideas that match your goals before others do.

- Target resilience by scanning companies with strong finances using our solid balance sheet and fundamentals stocks screener (44 results), which can help you focus on businesses with healthier balance sheets and fundamentals.

- Hunt for potential bargains by checking our 54 high quality undervalued stocks, which highlights companies that our models flag as high quality with prices that may not fully reflect their fundamentals.

- Strengthen your income ideas by reviewing our 13 dividend fortresses, which spotlights companies combining higher yields with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.