Assessing Mueller Water Products (MWA) Valuation After Recent Share Price Strength

Mueller Water Products, Inc. Class A MWA | 27.65 | -1.46% |

Mueller Water Products (MWA) has attracted attention after a recent move in its share price, with the stock closing at $29.44. That puts recent performance and current valuation back in focus for investors.

The recent 30-day share price return of 16.50%, alongside a 27.45% gain over 90 days and a 22.97% year to date share price return, contrasts with a 13.57% 1-year total shareholder return and much stronger 3-year and 5-year total shareholder returns of 118.24% and 152.91%. This suggests momentum has picked up again after a longer period of compounding gains for investors.

If Mueller Water Products has you thinking about long-term infrastructure themes, you might also want to see what stands out in our 24 power grid technology and infrastructure stocks as another way to find potential ideas.

With Mueller Water Products trading at $29.44 and only a small gap to a US$30.33 analyst target and a modest estimated intrinsic discount, you have to ask: is there real value left here, or is the market already pricing in future growth?

Most Popular Narrative: 0.9% Overvalued

With Mueller Water Products at $29.44 against a narrative fair value of about $29.17, the gap is small. This puts the assumptions behind that fair value in the spotlight.

Investments in smart water and leak detection technologies position the company to benefit from heightened emphasis by utilities and municipalities on water conservation and operational efficiency, likely bolstering higher-margin sales, recurring revenue streams, and future earnings growth.

Curious what kind of revenue run rate, margin lift and future earnings multiple are baked into that fair value work? The full narrative spells it out.

Result: Fair Value of $29.17 (ABOUT RIGHT)

However, you still need to weigh the chance that delayed infrastructure funding or softer construction activity could cut into the growth assumptions behind that fair value work.

Another View: Earnings Multiple Paints a Different Picture

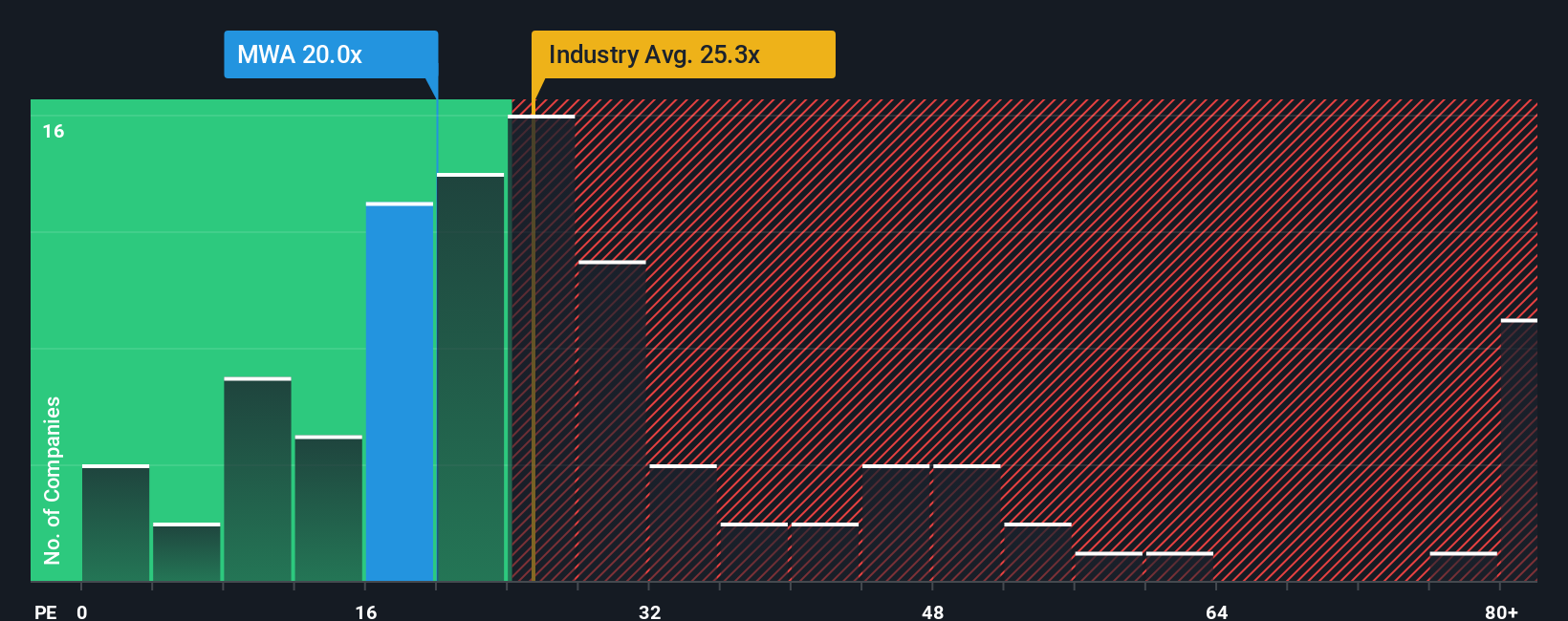

If you step away from fair value models and just look at the price tag on earnings, Mueller Water Products trades on a P/E of 23.1x. That sits below the US Machinery industry at 29.7x, below peers at 45.3x, and below a fair ratio estimate of 26.2x.

Put simply, the market is asking you to pay less for each dollar of Mueller Water Products' earnings than it pays for comparable names and less than where the fair ratio suggests the P/E could migrate to over time. Is that a cushion against disappointment, or a hint that investors are already baking in execution and funding risks?

Build Your Own Mueller Water Products Narrative

If you see the numbers differently or just want to stress test these assumptions yourself, you can build your own view in minutes with Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Mueller Water Products.

Looking for more investment ideas?

If Mueller Water Products is already on your radar, do not stop there. A broader watchlist can help you spot opportunities you might otherwise miss.

- Target quality at a reasonable price and scan our 51 high quality undervalued stocks to see which names currently stand out on both fundamentals and valuation filters.

- Prioritise resilience and capital protection by checking the 85 resilient stocks with low risk scores that focuses on businesses with lower risk scores and sturdier profiles.

- Hunt for promising names before the crowd by reviewing the screener containing 24 high quality undiscovered gems that highlights companies with strong fundamentals that receive less attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.