Assessing MYR Group (MYRG) Valuation After A Powerful Run In Power Infrastructure And Grid Services

MYR Group Inc. MYRG | 0.00 |

Event context and recent performance snapshot

MYR Group (MYRG) has drawn investor attention after a strong run in recent months, with the share price last closing at $337.76 and total return over the past year reported at 176.13%.

The recent 26.45% 1 month share price return and 32.63% 3 month share price return suggest momentum is building, reinforcing a 5 year total shareholder return of 302.00% and a 1 year total shareholder return of 176.13%.

If you are looking beyond MYR Group and want to see what else is moving in power infrastructure and grid plays, take a look at 33 power grid technology and infrastructure stocks

With MYR Group now trading at $337.76 and an intrinsic discount flagged at 22.02%, the key question is simple: is the current price still leaving upside on the table, or is the market already baking in future growth?

Most Popular Narrative: 10% Overvalued

At a last close of $337.76 versus the most followed fair value estimate of $307, the current price sits above what that narrative considers reasonable, which puts the underlying growth and margin story under the spotlight.

Sustained momentum in electrification spanning grid upgrades, data center buildouts, and transportation, coupled with robust private/public sector investment, is expected to drive strong demand for MYR Group's infrastructure services, elevating the overall addressable market and supporting top-line growth.

Curious what kind of revenue trajectory and margin uplift could justify that fair value, even with a lower future earnings multiple baked in? The most popular narrative leans heavily on steady top line expansion, firmer profitability, and a specific reset in the valuation multiple to tie the numbers back to $307.

Result: Fair Value of $307 (OVERVALUED)

However, you also need to keep an eye on risks such as rising labor costs and a lumpy C&I backlog, which could pressure margins and unsettle earnings visibility.

Another view on valuation

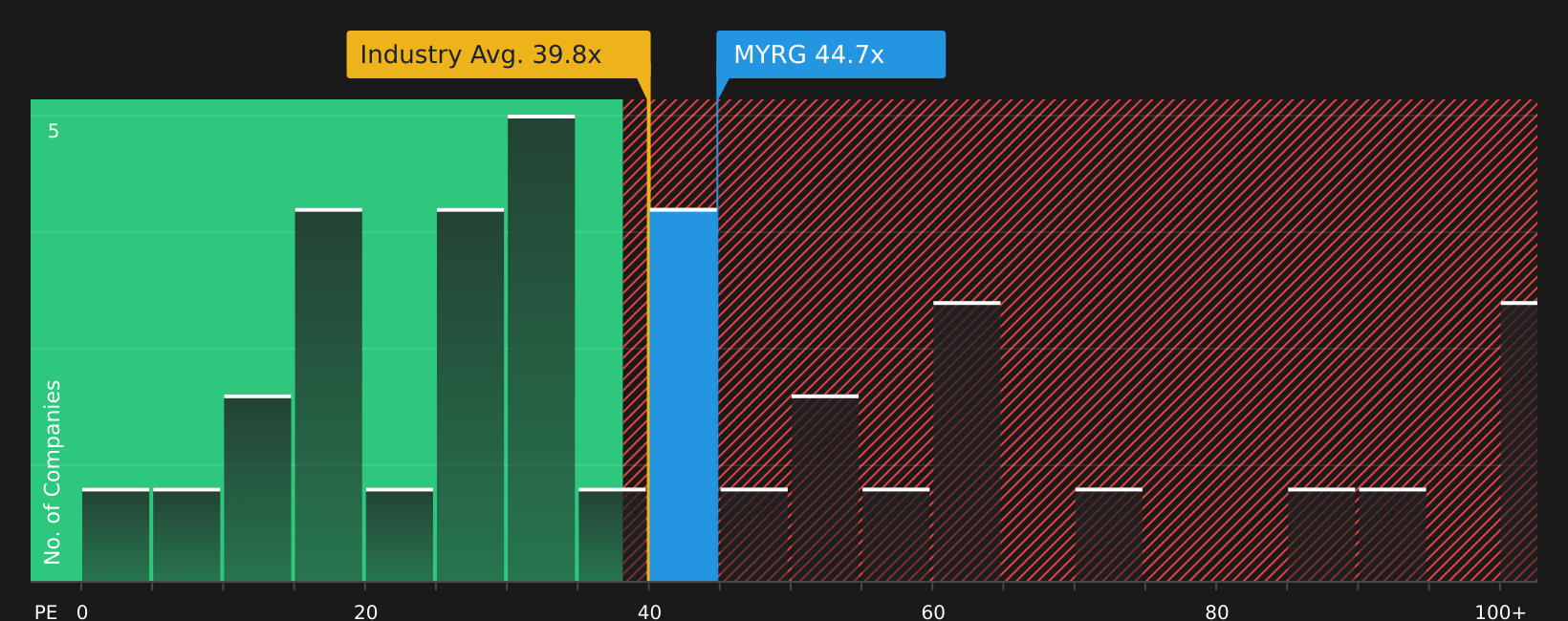

Analysts using earnings based multiples see MYR Group as expensive, with a P/E of 44.3x versus 43.1x for the US Construction industry and 35.1x for peers, and above a fair ratio of 26.9x. That gap raises a simple question: is the premium justified by your own expectations for the business?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out MYR Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of strong past returns and questions on valuation can pull you in different directions, so check the numbers yourself and decide how comfortable you are with the current setup. To understand what investors see as the positives worth paying attention to, take a look at the 3 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that fit your style. Broaden your watchlist using targeted screens built for different goals.

- Target value opportunities by checking companies that currently screen as 52 high quality undervalued stocks.

- Strengthen your potential income stream with companies highlighted in the 12 dividend fortresses.

- Prioritize resilience and capital preservation by reviewing the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.