Assessing Navigator Holdings (NVGS) Valuation After Record Q1 2026 Earnings And Portfolio Reshaping

Navigator Holdings Ltd. NVGS | 0.00 |

Navigator Holdings (NVGS) has drawn fresh attention after reporting record net income for Q1 2026, alongside a quarterly dividend declaration, an increased capital return target of 35% of net income, and plans to sell eight gas carrier vessels.

The recent Q1 2026 earnings, dividend declaration and planned vessel sales appear to have coincided with stronger momentum, with a 30 day share price return of 16.57% and a 1 year total shareholder return of 71.26% highlighting how sentiment has shifted.

If you are looking for more ideas beyond gas shipping, this could be a useful moment to broaden your research and check out 19 top founder-led companies

With the stock up 71.26% over the past year and recently within about 8% of its consensus price target, you now have to ask: Is Navigator still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 1% Undervalued

The most followed narrative places Navigator Holdings' fair value at $23.25, almost exactly in line with the last close of $23.01, which makes the underlying assumptions worth a closer look.

The continued structural shift toward cleaner fuels (like LPG and ammonia), together with industrial growth and higher living standards in emerging markets, is driving rising demand for liquefied gas and petrochemical transport. Navigator is already seeing restored trade volumes post-Q2 disruption, supporting higher utilization and revenue growth.

Want to understand why this almost fully valued stock still earns a premium narrative? The key is how falling margins, shrinking revenues and a richer future earnings multiple are stitched together into one tight valuation story.

Result: Fair Value of $23.25 (ABOUT RIGHT)

However, this narrative could be challenged if geopolitical disruption again hits volumes or if higher operating and environmental compliance costs squeeze already lower margin assumptions.

Another View: DCF Flags a Bigger Gap

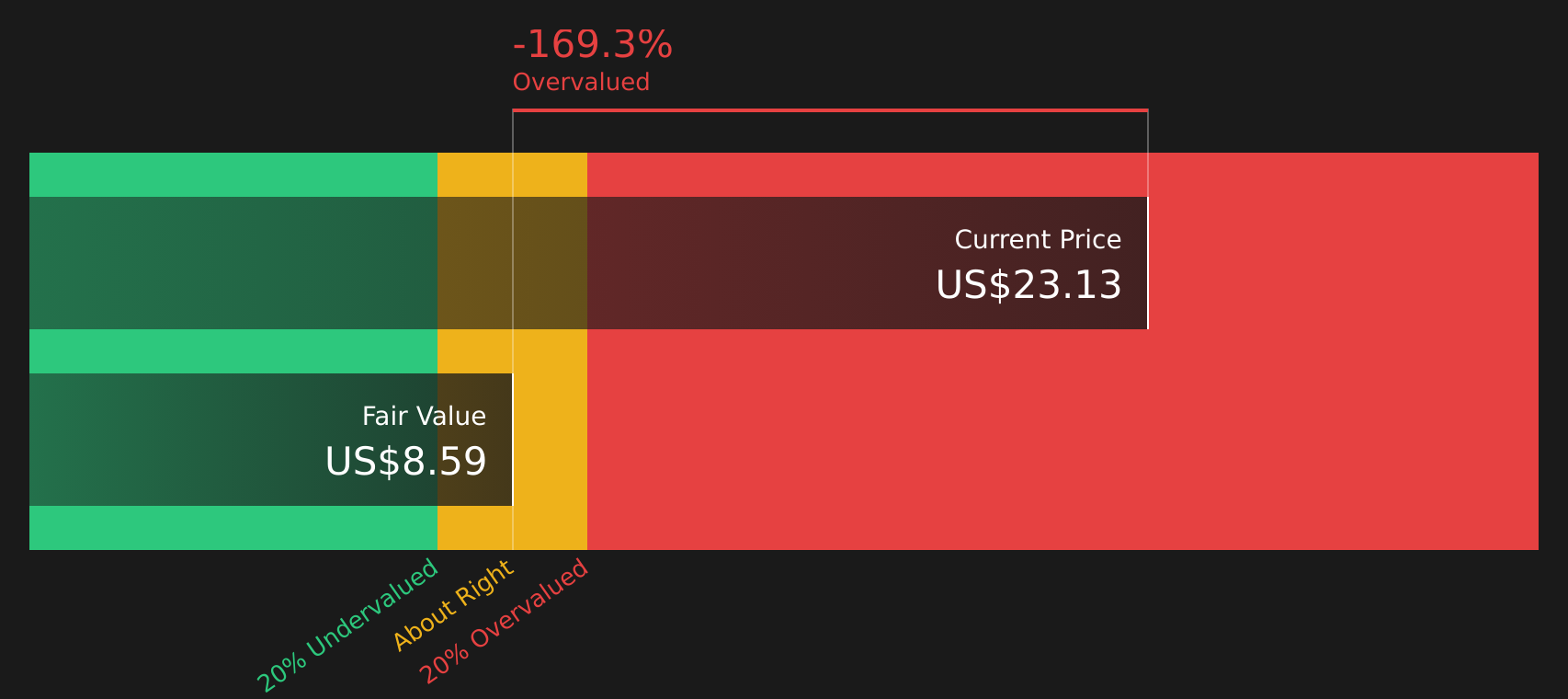

While analysts see fair value around $23.25, the Simply Wall St DCF model points to a future cash flow value of $12.43 per share, which is well below the current $23.01 price. That leaves you weighing up a strong narrative against a much more cautious cash flow view. Which side feels more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Navigator Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern has you on the fence, do not wait for consensus to form. Review the data, weigh both sides and see how the current 2 key rewards and 3 important warning signs

Looking for more investment ideas?

Do not stop your research with one stock. Broaden your watchlist now and give yourself more options before the next round of quarterly updates lands.

- Spot potential bargains early by scanning 50 high quality undervalued stocks and see which companies currently line up with solid fundamentals and lower implied expectations.

- Strengthen your downside protection by reviewing 71 resilient stocks with low risk scores so you are not caught out when market sentiment cools.

- Get ahead of the crowd by researching screener containing 21 high quality undiscovered gems before these quieter opportunities attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.