Assessing New Oriental Education & Technology Group’s Valuation After Recent Share Price Momentum

New Oriental Education & Technology Group, Inc. Sponsored ADR EDU | 58.33 | +5.16% |

New Oriental Education & Technology Group (NYSE:EDU) has been drawing investor attention after recent share price moves, with returns over the past year and past 3 months prompting fresh interest in its fundamentals.

At a share price of US$62.17, New Oriental’s 30 day share price return of 9.61% and 90 day gain of 14.18% sit alongside a 1 year total shareholder return of 30.15%. This suggests momentum has been building rather than fading recently.

If this has you thinking more broadly about where growth could come from next, it might be worth scanning 22 top founder-led companies as a way to surface other potential ideas beyond education stocks.

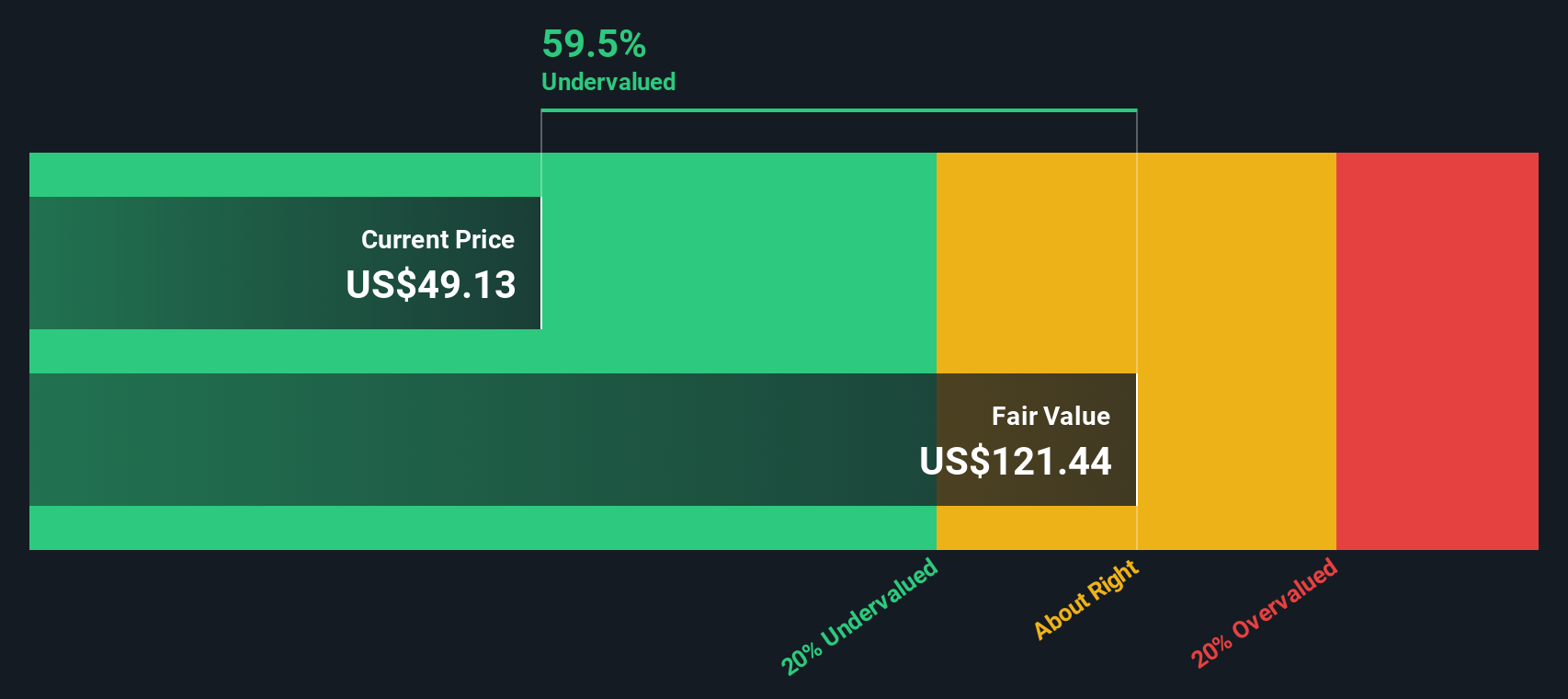

With New Oriental trading at US$62.17 and data pointing to an estimated intrinsic value and analyst targets that sit a little higher, the key question is whether the current price still leaves upside or if the market is already baking in future growth.

Most Popular Narrative: 3.6% Undervalued

With New Oriental closing at $62.17 against a widely followed fair value estimate of $64.49, the current price sits modestly below that narrative view, which leans on detailed earnings and cash flow forecasts.

Deferred revenue and customer prepayments are up nearly 10% year-over-year, signaling resilient demand and forward visibility in education business lines. This increases predictability of future revenue recognition and cash flow.

Aggressive share repurchases and the introduction of a three-year capital return plan committing at least 50% of net income to buybacks and dividends provide a direct and ongoing catalyst for EPS growth and shareholder value creation, especially when combined with rising profitability.

For readers interested in the earnings trajectory, margin profile behind that fair value, and how buybacks and growth expectations interact with the discount rate and future multiples, the full narrative lays out the complete set of assumptions that drive the $64.49 figure.

Result: Fair Value of $64.49 (UNDERVALUED)

However, this earnings story could change quickly if competition squeezes margins in core education segments, or if regulatory shifts and weaker overseas study demand hit revenue visibility.

Another View: Higher P/E Puts Market Optimism To The Test

Our DCF model points to New Oriental trading about 10.5% below its estimated future cash flow value of $69.49, which supports the undervalued story. The tension is that this view depends heavily on long term cash flow assumptions. How confident are you that those inputs will hold up?

Build Your Own New Oriental Education & Technology Group Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to weigh the inputs yourself, you can build a tailored view in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding New Oriental Education & Technology Group.

Looking for more investment ideas?

If New Oriental has you thinking about your next move, do not stop here. Use the Simply Wall St Screener to spot other opportunities that fit your style.

- Target potential mispricings by scanning 55 high quality undervalued stocks, which combines solid fundamentals with prices the market has not fully chased yet.

- Focus on resilience first by checking out solid balance sheet and fundamentals stocks screener (46 results), highlighting companies with stronger financial footing that can support their operations through tougher periods.

- Hunt for under the radar opportunities by reviewing screener containing 25 high quality undiscovered gems, where smaller names with quality metrics might not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.