Assessing Nexa Resources (NEXA) Valuation After A Strong Multi Month Share Price Surge

Nexa Resources S.A. NEXA | 11.07 | +0.73% |

Recent performance snapshot for Nexa Resources

Nexa Resources (NEXA) has quietly put up a mixed return profile, with a small gain over the past month, a decline over the past week, and a strong rise over the past 3 months.

With the share price at US$11.93, Nexa Resources is coming off a sharp 1 day share price return of 6.04% and a 90 day share price return of 93.98%, while its 1 year total shareholder return of 119.85% suggests momentum has been strong over a longer stretch despite some recent pullback.

If this kind of move has you looking beyond a single name, it could be a moment to scan other metal producers through our 8 top copper producer stocks as a starting list of potential ideas.

So with Nexa trading at US$11.93, sitting above the US$9.78 analyst target yet showing a 17% intrinsic discount and reporting improvements in revenue and net income, is there still a buying opportunity here or is the market already pricing in future growth?

Most Popular Narrative: 69.8% Overvalued

According to the most followed narrative, Nexa Resources has a fair value estimate of $7.03 compared with the current $11.93 share price. This indicates a clear gap between narrative expectations and where the market is trading today.

The plan to reach Aripuana’s nameplate capacity only in the second half of 2026, with the fourth tailings filter still in installation and commissioning, concentrates a lot of future zinc volume and cash flow in a single asset. Any delay or underperformance could weigh on revenue growth and EBITDA.

Want the full story behind that gap between price and fair value? The narrative leans heavily on a specific profit turnaround, modest revenue assumptions and a tighter earnings multiple. The key details sit in how those three pieces fit together over the next few years.

Result: Fair Value of $7.03 (OVERVALUED)

However, a sustained ramp up at Aripuana and smoother Cerro Pasco integration could support stronger volumes and cash generation than this 69.8% overvalued narrative assumes.

Another view on Nexa’s value

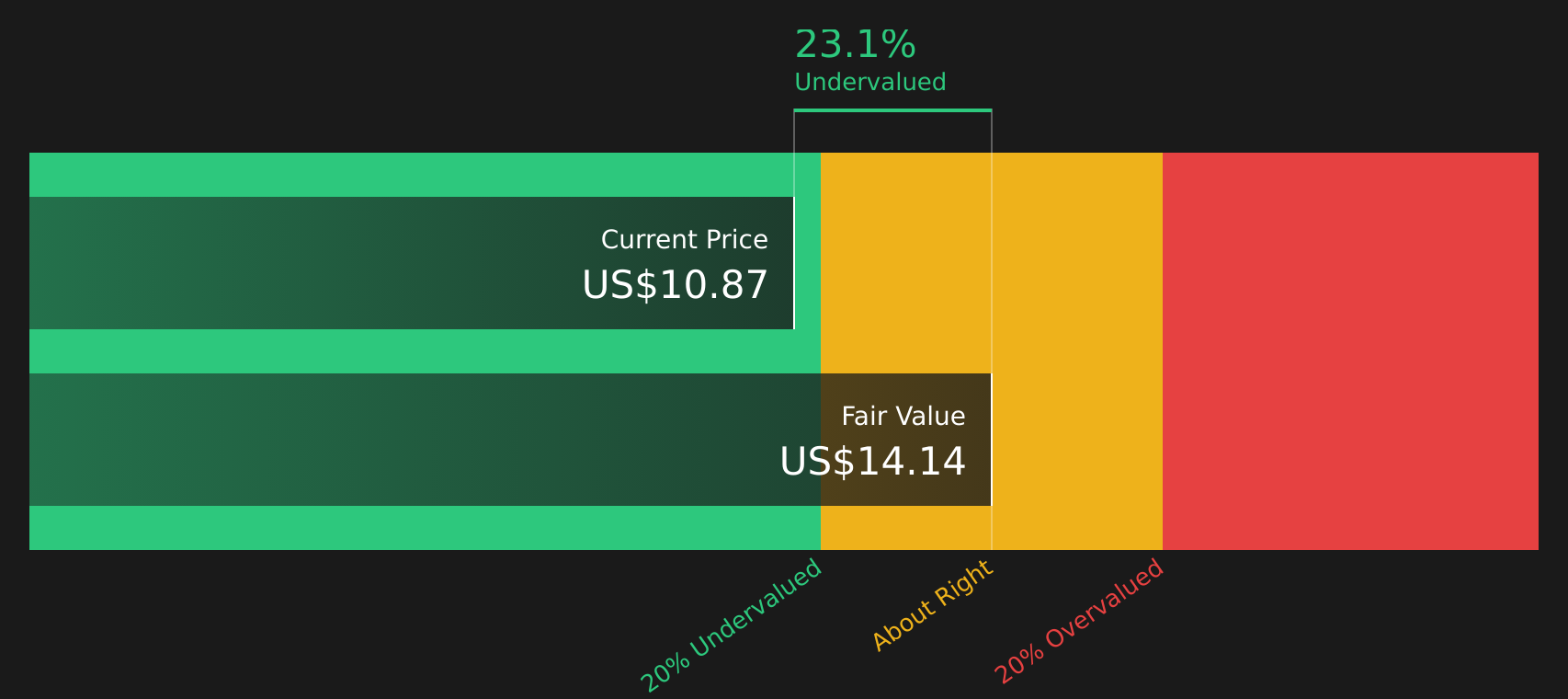

The narrative says Nexa Resources looks 69.8% overvalued at $11.93 versus a $7.03 fair value, but our DCF model points the other way, with a fair value of $14.36 and the shares trading at a 16.9% discount. When two methods disagree this much, which one do you trust more, and why?

Build Your Own Nexa Resources Narrative

If you are not fully aligned with these views or simply prefer to rely on your own work, you can develop a complete Nexa thesis yourself in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nexa Resources.

Looking for more investment ideas?

If Nexa has sparked your curiosity, do not stop here. Use the Simply Wall St stock screener to uncover a broader set of opportunities that fit your style.

- Target potential value opportunities by scanning our 54 high quality undervalued stocks, which pairs quality fundamentals with prices that may look appealing.

- Strengthen your income focus with our 13 dividend fortresses and quickly spot companies offering higher yields with an eye on stability.

- Prioritise resilience by checking the solid balance sheet and fundamentals stocks screener (45 results), where you can narrow in on businesses with financial structures that may handle bumps in the road better.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.