Assessing Nexa Resources (NEXA) Valuation After New Multi Year Production And Sales Guidance

Nexa Resources S.A. NEXA | 11.07 | +0.73% |

Nexa Resources (NEXA) shares reacted after the company released its fourth quarter and full year 2025 update, pairing softer reported metal sales with fresh multi year production and sales guidance through 2028.

The latest guidance is landing against a backdrop of sharp share price swings, with Nexa Resources closing at $11.80 after a 1‑day share price return of a 7.67% decline and a 7‑day share price return of a 14.86% decline, but a 90‑day share price return of 124.76% and a 1‑year total shareholder return of 97.49%. Taken together, these figures suggest that recent momentum has cooled in the very short term following a strong run.

If Nexa's update has you thinking more broadly about metals exposure, this could be a good moment to look at our list of 7 top copper producer stocks as another way to research the space.

With Nexa trading at US$11.80, sitting at a large intrinsic discount but above the average analyst target, the key question is whether the market is still underestimating the business or already pricing in future growth.

Most Popular Narrative: 68% Overvalued

Compared with the $11.80 share price, the most followed narrative points to a fair value near $7.03, using a consistent discount rate of 11.5%.

The plan to reach Aripuana’s nameplate capacity only in the second half of 2026, with the fourth tailings filter still in installation and commissioning, concentrates a lot of future zinc volume and cash flow in a single asset. Any delay or underperformance could weigh on revenue growth and EBITDA.

Want to understand why this narrative lands well below today’s price? It leans heavily on a specific earnings path, tighter margins and a disciplined profit multiple. The core issue is the tension between flat revenues and a swing to profitability. For a full view of how those elements connect to that $7 range, the complete narrative provides the details.

Result: Fair Value of $7.03 (OVERVALUED)

However, there are still real swing factors here, including a smoother Aripuana ramp and successful Cerro Pasco integration, that could shift cash generation meaningfully.

Another View: Multiples Tell a Very Different Story

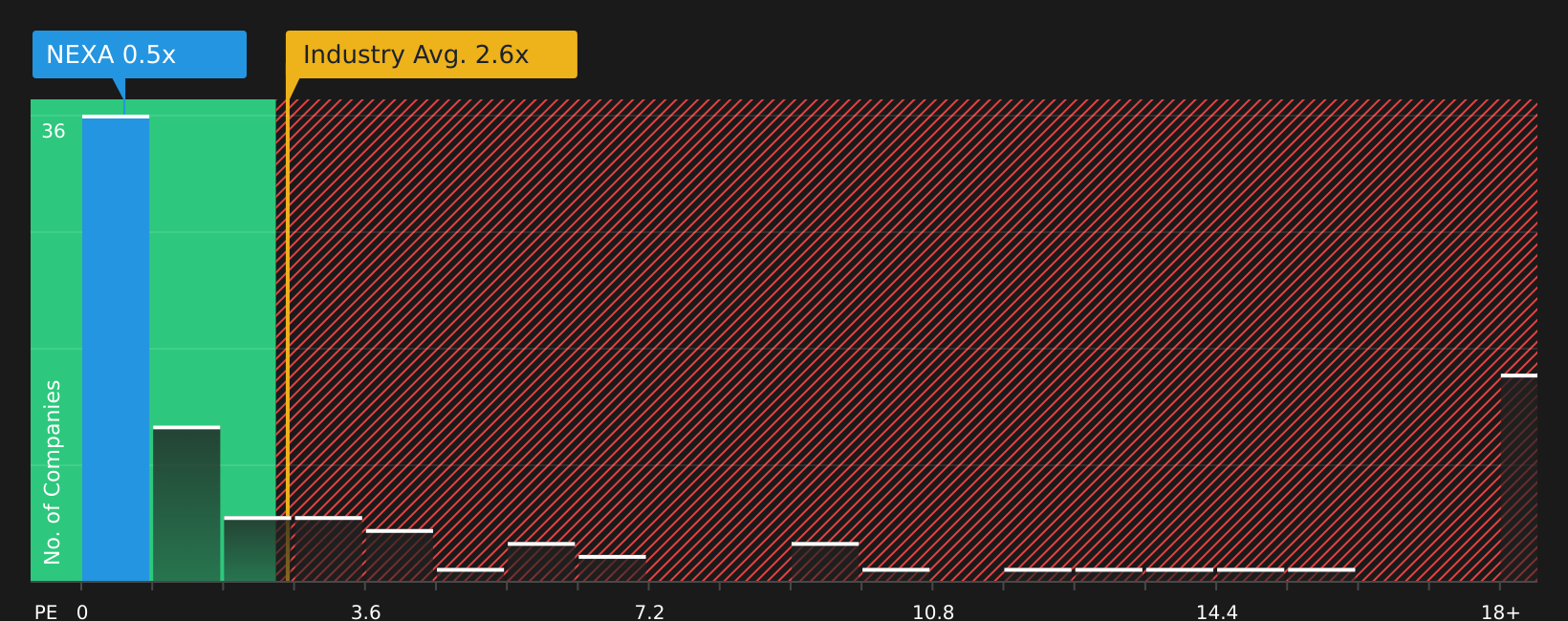

That $7.03 fair value from the narrative sits awkwardly next to how the market is actually pricing Nexa today. On a P/S of 0.6x, the shares sit far below the US Metals and Mining industry at 2.7x and a peer average of 9x, and even below a 0.9x fair ratio our work points to. That gap suggests the bigger risk may be underestimating what the market could pay if sentiment shifts.

To see what the numbers say about this price, and how that P/S gap might close over time, See what the numbers say about this price — find out in our valuation breakdown..

Build Your Own Nexa Resources Narrative

If your view on Nexa is different or you simply prefer to rely on your own work, you can build a custom thesis in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nexa Resources.

Looking for more investment ideas?

If Nexa has sharpened your thinking, do not stop here; use this as a springboard to line up your next few investment candidates with purpose.

- Hunt for quality on sale by checking our list of 55 high quality undervalued stocks that combine strong fundamentals with appealing prices.

- Prioritise staying power by scanning solid balance sheet and fundamentals stocks screener (46 results) to spot companies with financial structures that can support long term plans.

- Get ahead of the crowd by reviewing our screener containing 25 high quality undiscovered gems before others start paying attention to these ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.