Assessing NextEra Energy (NEE) Valuation After Recent Short Term Share Price Weakness

NextEra Energy, Inc. NEE | 0.00 |

Why NextEra Energy Is Drawing Attention Now

NextEra Energy (NEE) is back on many investors’ watchlists after a period of mixed short term returns, with a 1 day decline of 2.17% and a total return of 40.65% over the past year.

The recent 1 day share price return of -2.17% and 7 day share price return of -4.66% sit against a year to date share price return of 15.31% and a 1 year total shareholder return of 40.65%. Together, these figures point to momentum that has cooled in the very short term while remaining strong over a longer horizon.

If you are looking beyond utilities and want to see what else is moving with the energy transition theme, it is worth scanning 36 power grid technology and infrastructure stocks

With the stock sitting close to analyst targets and a low value score, along with solid recent revenue and net income growth, you have to ask: is NEE still underappreciated, or is the market already pricing in future growth?

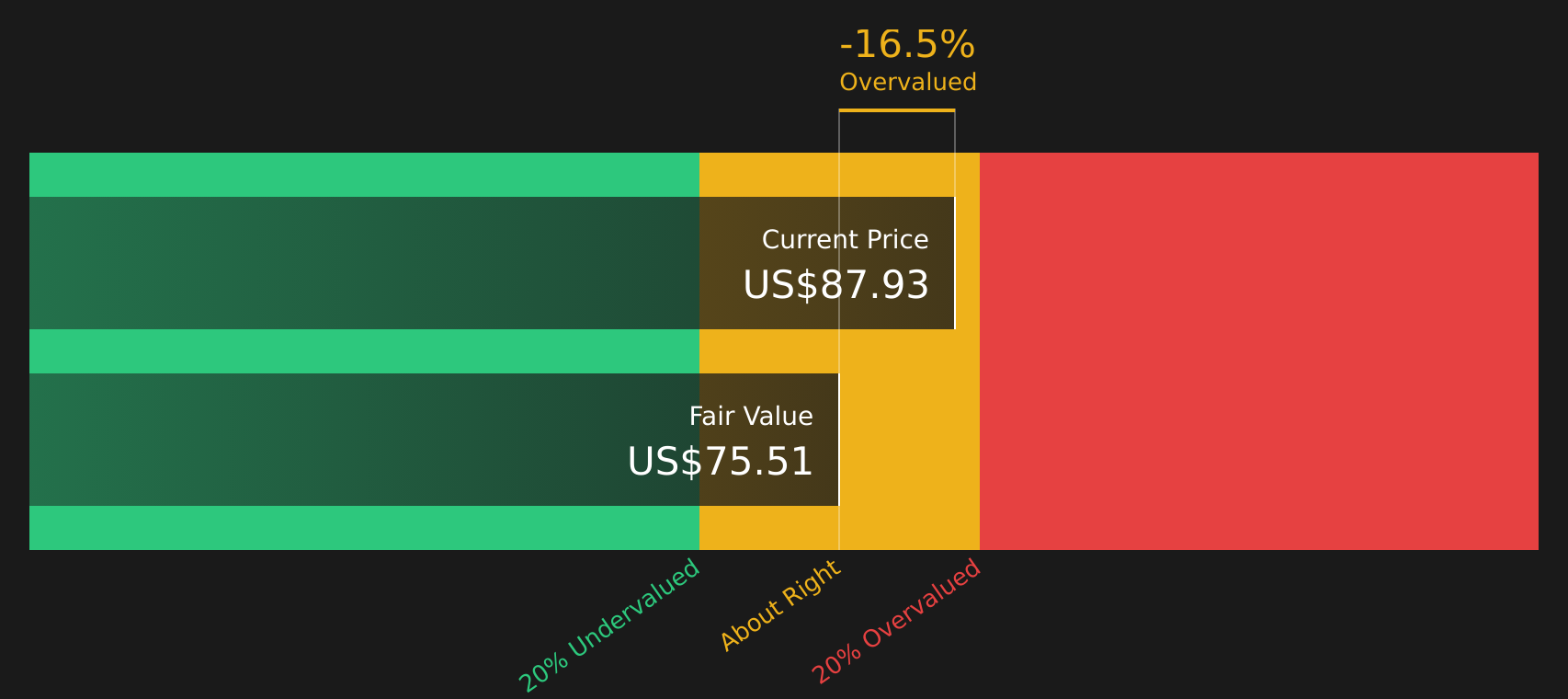

Most Popular Narrative: 1.1% Undervalued

NextEra Energy's last close at $93.32 sits just below a fair value estimate of $94.33 according to the most followed narrative, leaving only a slim valuation gap to interrogate.

On a blended basis, this SOTP model yields a Fair Value Estimate of approximately $94.33. While the current $96 price reflects peak market optimism and "momentum buying" following the earnings surprise, it leaves a razor-thin margin for error.

For a disciplined investor, $90 (approx. 22x blended P/E) remains the ideal entry point. It represents a price where the AI growth is a "bonus" rather than a requirement for holding. At $96, the stock is ''Fairly Valued'' in a perfect-growth scenario, but potentially vulnerable to any shifts in interest rate policy or regulatory pushback. Read the complete narrative.

Want to see how a regulated utility and an AI focused renewables platform get blended into one fair value math? The key driver here is a split between a steady earnings anchor and a higher growth engine, plus assumptions about how long that earnings mix can hold. The full narrative lays out exactly which profit trajectory and valuation multiple are doing the heavy lifting in that $94.33 figure.

Result: Fair Value of $94.33 (ABOUT RIGHT)

However, the story could quickly change if interest rate policy tightens again or if regulators slow project approvals across Florida Power & Light and NextEra Energy Resources.

Another View: Our DCF Model Paints A Different Picture

While the SOTP narrative points to a fair value of $94.33, our DCF model tells a different story. Using that method, NEE at $93.32 sits above an estimated future cash flow value of $75.97, which suggests less upside and more need for discipline around entry price.

For readers who want to see how cash flow assumptions compare with the market price, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NextEra Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment, do you feel the risk reward trade off is still compelling here, or already stretched? Act while the data is fresh and weigh the potential upside against the concerns using our breakdown of 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If NEE feels finely balanced, broaden your watchlist now. Fresh opportunities often appear first in focused screens rather than front page headlines.

- Spot potential quality at a discount by scanning 51 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their financial profile.

- Secure income focused opportunities by reviewing 12 dividend fortresses that pair higher yields with an emphasis on stability and consistency.

- Dial down portfolio risk by checking 72 resilient stocks with low risk scores built around companies with more resilient balance sheet and risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.