Assessing Norfolk Southern (NSC) Valuation As Shares Show Mixed Short And Long Term Returns

Norfolk Southern Corporation NSC | 0.00 |

Stock performance snapshot and recent context

Norfolk Southern (NSC) has drawn investor attention after recent trading, with the stock last closing at US$305.16. Short term returns have been mixed. This may prompt you to reassess how NSC fits in a rail-focused portfolio.

Recent trading has been choppy, with a 7 day share price return of down 2.98% and a 30 day share price return of down 3.40%. The 1 year total shareholder return of 26.73% points to stronger longer term momentum, which contrasts with the softer 90 day share price return of down 3.81%.

If you are weighing NSC against other transport exposed ideas, it can be useful to see how rail linked infrastructure compares with broader power and grid themes through the 33 power grid technology and infrastructure stocks

With Norfolk Southern trading at US$305.16 and sitting at a discount to analyst targets but at a premium to one intrinsic estimate, the real question is whether you are looking at a genuine opportunity or a stock already pricing in future growth?

Most Popular Narrative: 8.1% Undervalued

Norfolk Southern's most followed narrative points to a fair value of $332.22 per share, compared with the last close at $305.16. This frames a modest valuation gap that hinges on execution of its operating and network plans.

The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could bolster future revenue growth. Strategic plans to capitalize on industrial development activity, particularly in sectors like steel and food production, along with the potential for highway to rail conversions, are expected to provide new demand drivers for volume growth, supporting long term revenue enhancement.

Want to see what kind of revenue path, margin profile and future P/E this narrative needs to support that fair value? The full story connects service gains, productivity targets and long term infrastructure demand into one tight valuation case that is not obvious from the headline numbers alone.

Result: Fair Value of $332.22 (UNDERVALUED)

However, investors also need to keep an eye on weather related restoration costs and pressure from lower export coal pricing, both of which could strain margins and earnings assumptions.

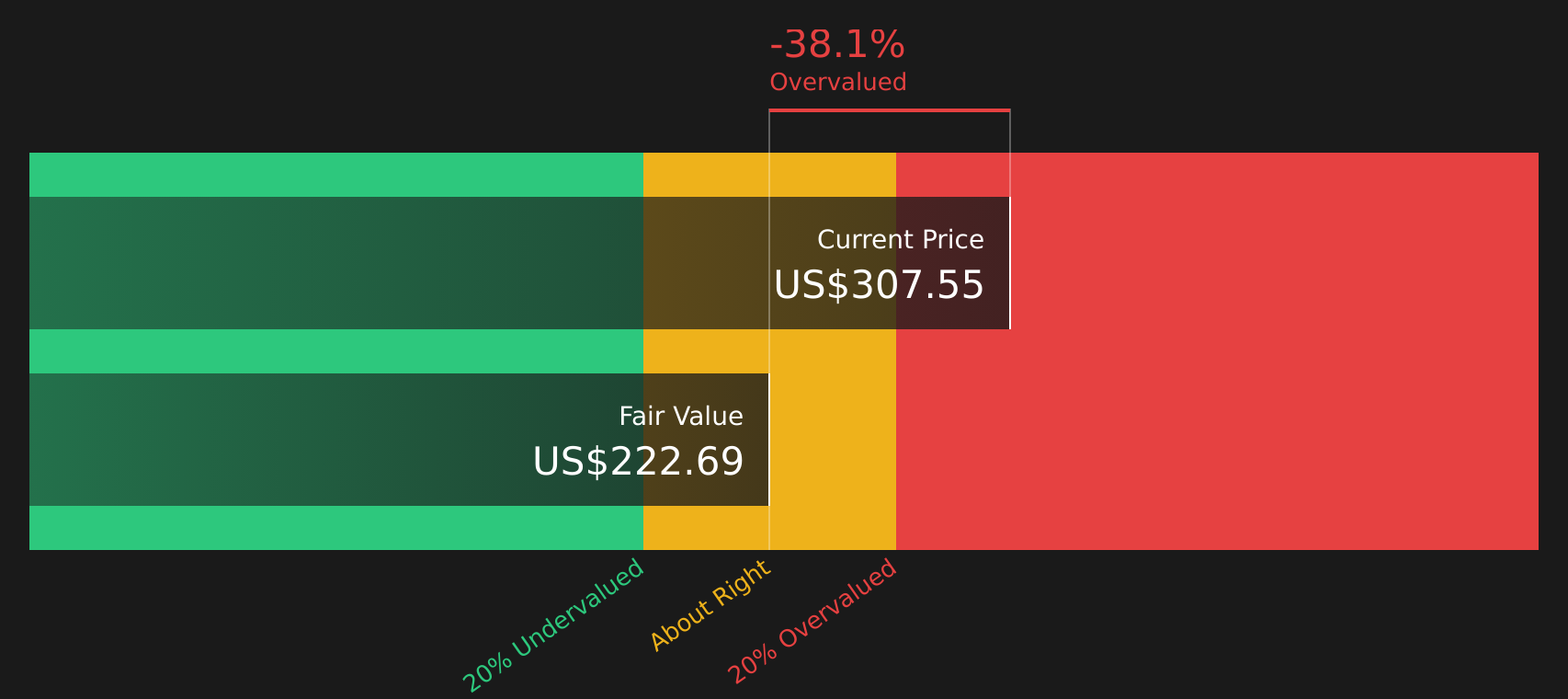

Another angle on valuation

The popular narrative frames Norfolk Southern as about 8.1% undervalued at $305.16, using forward earnings assumptions and a P/E of 27.5x. Yet our DCF model, based on future cash flows, points to a fair value of $223.09, which would make the stock look expensive instead. Which story do you trust more: earnings or cash flows?

Next Steps

With mixed signals across valuation methods and sentiment, it makes sense to move quickly and test the data against your own expectations for the stock. To get a balanced view of both the concerns and the upside that other investors are focused on, take a close look at the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

NSC may be on your radar, but broadening your watchlist with other focused stock ideas can help you spot opportunities you would otherwise miss.

- Target income potential with companies that currently offer stronger yields by scanning the 10 dividend fortresses.

- Hunt for quality at a possible discount by filtering stocks that look attractively priced through the 47 high quality undervalued stocks.

- Prioritise sleep at night holdings by concentrating on companies screened in the 62 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.